The State Pension Funding Gap: 2016

Investment shortfalls, insufficient contributions reduced funded levels for public worker retirement plans

Overview

Many state retirement systems are on an unsustainable course, coming up short on their investment targets and having failed to set aside enough money to fund the pension promises made to public employees. Even as contributions from taxpayers over the past decade doubled as a share of state revenue, the total still fell short of what is needed to improve the funding situation.

There is no one-size-fits-all solution to the pension funding shortfall and the budgetary challenges facing individual states, but without new policies that commit states to fully funding retirement systems, the impact on other essential services—and the potential for unpaid pension promises—will increase.

The Pew Charitable Trusts analyzed the state pension funding gap for fiscal year 2016, the most recent year for which comprehensive data were available for all 50 states. This brief outlines the primary factors that caused the widening divide in most states between assets and liabilities, and identifies tools that can help legislators strengthen policies and better manage risk for their state’s retirement plans.

In 2016, the state pension funds in this study cumulatively reported a $1.4 trillion deficit—representing a $295 billion jump from 2015 and the 15th annual increase in pension debt since 2000. Overall, state plans disclosed assets of just $2.6 trillion to cover total pension liabilities of $4 trillion.

Investment returns that fell short of state assumptions caused a major part of the increase in the funding gap. The median public pension plan’s investments returned about 1 percent in 2016, well below the median assumption of 7.5 percent—a disparity that added about $146 billion to the debt.1 Assumption changes—primarily states lowering the assumed rate of return used to calculate pension costs—accounted for another $138 billion in increased liabilities.

Even if plan assumptions had been met in 2016, the funding gap would have increased by $13 billion because states did not allocate enough to their systems. As a whole, they would have needed to contribute $109 billion to pay for both the cost of new benefits and interest on pension debt; the actual amount contributed, $96 billion, fell short.

Preliminary information for 2017 indicates that the year’s strong investment performance will decrease reported unfunded liabilities, as public pension funds—which continue to allocate an ever greater share of assets to complex investments such as equities, hedge funds, real estate, and commodities that can produce higher returns than other assets but may also expose plans to increased risk—experienced gains from the upswing in financial markets. However, that same market volatility could have an adverse impact in the long term, especially if lawmakers also fail to make adequate annual contributions to state plans.

Even small changes to projected returns can significantly increase liabilities. Pew applied a 6.5 percent return assumption, instead of the median assumption of 7.5 percent, to estimate the total liability for state pension plans and found that it would increase to $4.4 trillion—$382 billion more than the current amount. The funding gap would then jump to $1.7 trillion.

Similarly, public pension disclosures are now required to estimate funding levels using investment assumptions at 1 percentage point above and below the plan’s assumed rate of return.

Ultimately, differences in state pension funding levels are driven by policy choices, with well-funded states having records of making actuarial contributions, managing risk, and avoiding unfunded benefit increases. Measures of plan assets as a percentage of liabilities in 2016 ranged from 31 percent in New Jersey to 99 percent in Wisconsin. Colorado, Connecticut, Illinois, Kentucky, and New Jersey were less than 50 percent funded, and another 17 states had less than two-thirds of the assets needed to pay promised benefits. Only New York, South Dakota, Tennessee, and Wisconsin were at least 90 percent funded. (See Figure 1.)

Other metrics of pension plans’ financial health can indicate whether contribution policies are sufficient to make progress in paying down pension debt and keeping assets from being depleted. For example, net amortization measures whether expected contributions would have been enough to reduce unfunded liabilities—if return assumptions are accurate—while a new indicator, the operating cash flow ratio, can give a better sense of annual changes. These tools can help policymakers better track the financial health of state pension plans and act when warranted.

Key Terms

- Operating cash flow: The difference, before investments, between expenses (including benefit payments) and employer and employee contributions. When divided by assets, it is a benchmark for the rate of return required to ensure that asset balances do not decline.

- Funded ratio: The level of a plan’s assets, at market value, in proportion to accrued pension liability. This is an annual point-in-time measure, as of the valuation date.

- Net amortization: Measures whether total contributions to a public retirement system would have been sufficient to reduce unfunded liabilities if all actuarial assumptions—primarily investment expectations—had been met for the year. The calculation uses the plan’s reported numbers and assumptions about investment returns. Plans that consistently fall short of this benchmark can expect to see the gap between the liability for promised benefits and available funds grow over time.

- Net pension liability: Current-year pension debt calculated as the difference between the total value of pension benefits owed to current and retired employees or dependents and the plan assets on hand. Pension plans with assets greater than accrued liabilities show a surplus.2

- Sensitivity analysis: A method for measuring the impact of differing assumptions, particularly around investments, on key pension funding measures. Sensitivity analyses showing an investment return assumption 1 percentage point higher or lower than the base assumption are included in Governmental Accounting Standards Board (GASB) disclosures.

Debt drivers

Investment returns that fell short of plan assumptions accounted for a significant portion of the $295 billion growth in net pension liability from 2015 to 2016. (See Figure 2.) Data collected by the Wilshire Trust Universe Comparison Service show median state pension plan returns of about 1 percent for 2016, the worst performance since the end of the Great Recession in 2009. That year the median investment return assumption used to calculate expected pension costs was 7.5 percent—a difference of 6.5 percentage points. Because of investment market volatility, public pension plans in the aggregate missed their return targets in five of the preceding 10 years.3 Investment underperformance in 2016 added about $146 billion to the overall funding gap—on top of the $125 billion increase from investment shortfalls in 2015.

Changes to assumptions about investment performance also were a major driver of increased pension debt in 2016. Several state pension plans made more conservative projections about performance—or were forced to do so because of new standards set by GASB in 2014. The lower assumed rates of return, along with other changes to actuarial assumptions, increased the reported liability by $138 billion.

Two other factors contributed to the increase in net pension liability. Even if the assumptions of every plan had been met in 2016, the aggregate funding gap would have increased because contribution policies did not bring in sufficient resources to meet the growing costs. States in the aggregate would have needed to contribute $109 billion for both the cost of new benefits and interest on pension debt; actual employer contributions fell short by a total of about $13 billion. Finally, benefit changes and demographic experience reduced liabilities by about $3 billion. The latter could include factors such as salaries growing more slowly than expected or retirees’ life spans not increasing as quickly as projected.

Recent changes to accounting rules also play a role in the fluctuations in reported net pension liability. Under the new GASB standards, pension assets are reported using actual market values rather than the traditional calculations that smoothed gains and losses over time. As a result, continued volatility in reported annual funding levels is likely.

Investment volatility contributes to funding volatility

While state pension plans have been lowering their assumed rates of return—from a median of more than 8 percent in 1992 to 7.5 percent in 2016—the level of risk that states take on to meet investment targets has never been higher. Twenty years ago, states needed only to exceed the yield on a 30-year Treasury bond by 1 percentage point to meet their investment targets. Currently, the typical state would need to outperform a 30-year Treasury bond by 5.2 percentage points to meet its now-lower investment assumption. That reality has forced plans to take on higher levels of investment risk. (See Figure 3.)

The share of public funds’ investments in stocks, private equity, and other risky assets has increased by over 30 percentage points since 1990—to over 70 percent of the portfolio of state pension plans. As a result, pension plan investment performance now closely follows equity returns.4 (See Figure 4.)

Since 2009, overall median returns for public pension plans have ranged from 0.7 percent in 2016 to 19.2 percent in 2011, volatility attributable in part to increased investment portfolio risk.5 While one or two years of weak returns may not indicate fiscal danger for a pension plan, such volatility presents long-term policy challenges.

Assuming 6.5% return provides useful perspective

To better understand the risk exposure of public funds, policymakers need access to stress testing or sensitivity analyses, which simulate scenarios that can measure the fiscal impact of lower investment performance or other missed assumptions. The most basic approach is to evaluate pension liabilities at alternative assumed rates of return. The median return assumption used by state pension plans to calculate liabilities in 2016 was 7.5 percent, according to data collected by Pew. However, state plans generated just 6 percent returns over the past decade, and various projections suggest that returns will be around 6.5 percent a year for the next 10 years or longer.6

To illustrate the impact of lower-than-expected returns, Pew estimated the total and net pension liabilities at a 6.5 percent assumed rate of return. The return assumptions were not changed if already below 6.5 percent. (See Figure 5.)

As shown in Figure 5, states’ pension liabilities would grow to nearly $4.4 trillion using a 6.5 percent return assumption. That equals a $1.7 trillion funding gap between assets and liabilities.

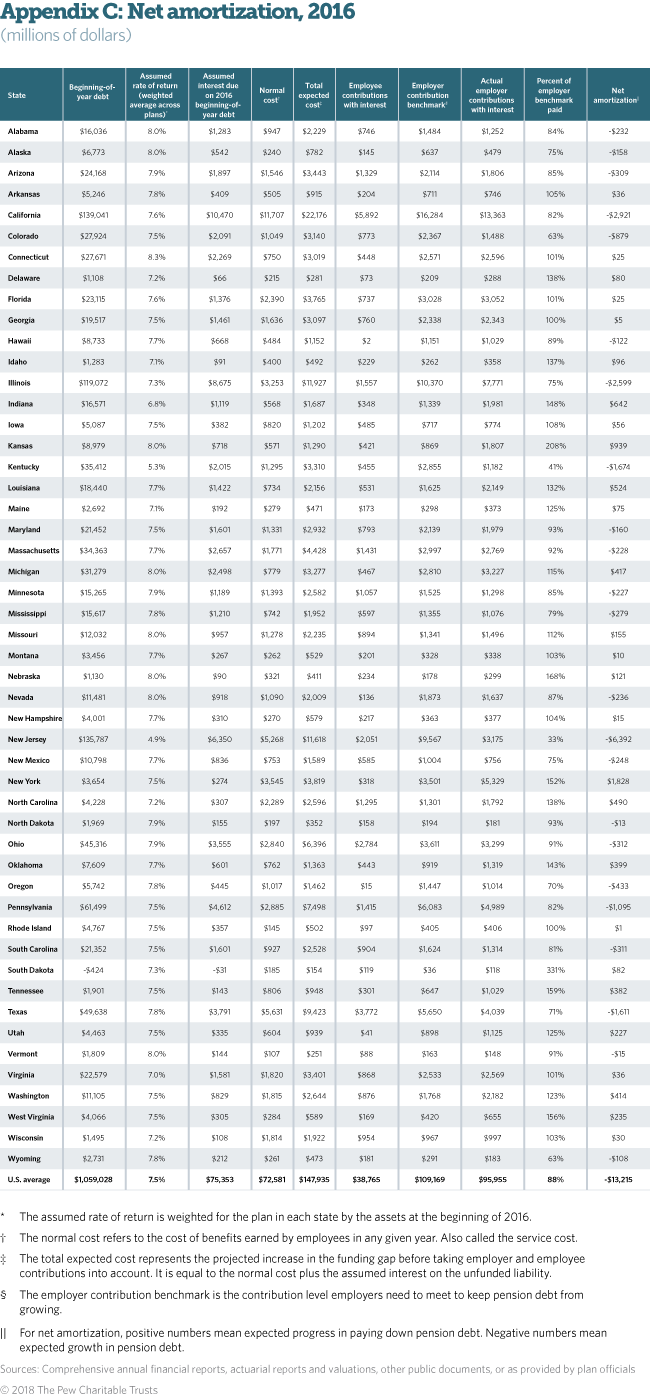

Net amortization

Public pension plans typically set an actuarially determined rate for government employers to contribute to the plan so the plan will have sufficient resources to pay out expected benefits while trying to keep employer contribution rates relatively stable. Historically, many states have fallen short on these contributions, but even those that make the full actuarial contribution still may not reduce their funding gap. To address the potential inadequacy of the contribution rates set by plan actuaries, credit rating agencies and other pension analysts can use data collected under the new GASB standards. Pew’s net amortization metric, introduced in its 2014 funding gap brief, creates a contribution benchmark. This is the third year that data have been available to calculate net amortization.

The net amortization benchmark for the required employer contribution is the combined cost of new benefits earned in a given year—known as the service cost—plus the interest on the pension debt minus the expected employee contributions. The interest on the pension debt represents the net pension liability at the beginning of the year multiplied by the assumed rates of return. Employee contributions totaled $39 billion in 2016, after factoring in interest.

If the employer’s annual contribution, with interest, equals the net amortization benchmark, then the net pension liability will neither grow nor shrink if all plan assumptions are met. If the employer sets aside more than the benchmark, the net pension liability will shrink in a given year and there will be positive amortization of the debt. Alternatively, if the employer contribution falls below the benchmark, the funding gap will increase, resulting in negative amortization.

In the aggregate, states have not set aside enough funds to keep their pension debt from growing, let alone to make significant progress on closing the current funding gap. States and participating local governments contributed $96 billion—including interest—to state pension plans in 2016, $13 billion less than the $109 billion needed to avoid further debt growth. In other words, even if every plan had met its investment target and other assumptions, the unfunded liability would have grown because state contributions were insufficient. The net amortization therefore would be negative.

Only 27 states contributed enough in 2016 to expect their funding gaps to decline if actuarial assumptions were met, while 23 fell short. From 2014 through 2016, 23 states exceeded the net amortization benchmark on average, although only 14 did so in all three years.

Figure 6 shows net amortization as a share of payroll for each state from 2014 to 2016. Factoring in total payroll helps to normalize the results of states of different sizes; it also allows the number to be expressed as the increase in the contribution rate a state would have needed in order to achieve positive amortization over that period. Because volatile investment returns, among other factors, can cause the benchmark to fluctuate, aggregating over three years gives a better picture of the long-term trend.

A new indicator: Operating cash flow ratio

Most pension analyses focus on actuarial measures, which are designed to look at a fund’s long-term balance sheet. Financial metrics such as cash flow, however, can provide early warnings of liquidity concerns and insolvency risk, particularly for state pension plans in severe distress. Cash flow measures also can highlight the annual impact of volatility for plans with comparatively healthy fiscal situations.

A new indicator, the operating cash flow ratio, represents the difference between financial outflows (primarily benefit payments) and cash coming in before investments (primarily employer and employee contributions) divided by the level of assets at the beginning of the year. A plan with an operating cash flow ratio of 3 percent, for example, would need to achieve investment returns of at least 3 percent that year to keep assets from dropping.

Most public pension plans are long-standing and mature, and are therefore likely to have negative ratios because they see more money going out in benefits than coming in from current workers. However, the aggregate trend for this ratio has worsened since 2000—some plans falling to 5 percent or lower—indicating that state pension plans are growing more dependent on investments to pay anticipated benefits. The operating cash flow ratio has improved slightly since hitting a low in 2010, but the recovery after each recession since 2000 has not been as great as the decline during the financial downturn. (See Figure 7.)

In total, state pension plans paid out $214 billion in pension benefits in 2016, and took in $37 billion in employee contributions and $93 billion from employers. Dividing the cash flow by the total asset value of $2.6 trillion results in an average operating cash flow ratio of 3.2 percent for states in 2016. Seven states had ratios below 5 percent; 10 had ratios above 2 percent.

As overall operating cash flow declines, mediocre investment performance is more likely to cause a drop in plan assets, which makes it harder for plans to generate returns in the future. When the absolute value of the operating cash flow ratio exceeds the assumed rate of return, plan managers can expect assets to decline over time—with the possibility of insolvency if the trend is not arrested. For plans with very low funding levels, growing negative ratios can indicate liquidity concerns. States such as New Jersey and Kentucky, which have the lowest operating cash flow ratios, are facing real risks and challenges, but all except the top 10 performers have worse ratios than the average state had in 2000.

Conclusion

The funding gap for the state pension plans studied reached $1.4 trillion in 2016—an increase of $295 billion from 2015. State contribution policies proved insufficient to deal with the unfunded liabilities already on the books. Even if all assumptions had been met, the funding gap would have grown by $13 billion. Instead, investments fell short of assumptions for the second year in a row, leaving state pension debt at historic highs.

Other measures of fiscal vulnerability also show cause for concern. The gap between returns on safe investments and state pension plan investment assumptions was the highest in decades. Independent analyses suggest that states can assume returns of about 6.5 percent a year for at least the next 10 years; 5 percent or lower returns are a real possibility over the next 20 years.7 While strong investment performance in 2017 would lower reported unfunded liabilities in the short term, measures of plan cash flow show that state pension plans increasingly depend on investment performance to keep assets from declining. All of these measures show that plans are more vulnerable to volatility than in the recent past, which could have an adverse impact on funds in the future.

But policymakers have options. As well-funded states have shown, combining strong contribution policies with a focus on managing risk and avoiding unfunded benefit increases can help states offer secure retirement benefits in a sustainable and affordable way. The data, however, show that most states are falling short of this standard.

By many measures, the riskiness of states’ investments is higher than it has been in decades. Stress testing and sensitivity analyses can help policymakers understand the risk and uncertainty under current policies and decide how best to manage or reduce that risk.

Finally, policymakers should monitor measures of cash flow to make sure that their state plans are not in danger of insolvency or illiquidity. Recent results are showing that states are growing more dependent on investments to keep assets from declining since 2000. States vary significantly on this measure; understanding where their state lies can help policymakers manage retirement policies.

Appendix A: Methodology

All figures presented are as reported in public documents or as provided by plan officials. The main data sources used were the comprehensive annual financial reports produced by each state and pension plan, actuarial reports and valuations, and other state documents that disclose financial details about public employment retirement systems. Pew collected data for over 230 pension plans.

Pew shared the collected data with plan officials to give them an opportunity to review and to provide additional information. This feedback was incorporated into the data presented in this brief.

Pew assigns funding data to a year based on the valuation period, rather than when the data are reported. Because of lags in valuation for many state pension plans, only partial 2017 data were available, and fiscal 2016 is the most recent year for which comprehensive data were available for all 50 states. Data on Tennessee aggregate political subdivisions were not available for fiscal 2016, so data were rolled forward from 2015.

Each state retirement system uses different key assumptions and methods in presenting its financial information. Pew made no adjustments or changes to the presentation of aggregate state asset or liability data for this brief. Assumptions underlying each state’s funding data include the assumed rate of return on investments and estimates of employees’ life spans, retirement ages, salary growth, marriage rates, retention rates, and other demographic characteristics.Although the accounting standards dictate how pension data must be estimated for reporting purposes, state pension plans may use different actuarial assumptions or methods for the purpose of calculating contributions. Pew has consistently used reported data based on public accounting standards in order to have comparable information on plan financials.

Endnotes

- Median data from Wilshire Trust Universe Comparison Service (June 30, 2017), compiled for Pew.

- For a technical description of net pension liability and other pension accounting terms, see Governmental Accounting Standards Board, “Statement No. 67” (2012), http://www.gasb.org/jsp/GASB/Document_C/DocumentPage?cid=1176160220594&acceptedDisclaimer=true; Governmental Accounting Standards Board, “Statement No. 68” (2012), http://www.gasb.org/jsp/GASB/Document_C/DocumentPage?cid=1176160220621&acceptedDisclaimer=true.

- Median annual return data from Wilshire Trust Universe Comparison Service (2005-16), compiled for Pew.

- The Pew Charitable Trusts and the Laura and John Arnold Foundation, “State Public Pension Investments Shift Over Past 30 Years” (2014),http://www.pewtrusts.org/~/media/assets/2014/06/ state_public_pension_investments_shift_over_past_30_years.pdf.

- Median 10-year data from Wilshire Trust Universe Comparison Service (June 30, 2016), compiled for Pew.

- Pew, along with outside experts, developed a capital markets assumption model that projects a median long-run return of 6.4 percent for a plan with a typical investment portfolio. Other analysts with similar projections include Voya Financial Advisors (6.4 percent), JPMorgan and Wilshire (both 6.5 percent), Aon Hewitt (6.6 percent), and Bank of New York Mellon (7.2 percent).

- This is derived from a model taking into account the riskiness of pension plan fund investments. A long-term model of returns with a median of 7.5 percent and 12 percent standard deviation will show a 25th percentile of about 5 percent.

America’s Overdose Crisis

Sign up for our five-email course explaining the overdose crisis in America, the state of treatment access, and ways to improve care

Sign up

DID YOU KNOW?

ADDITIONAL RESOURCES

Article

Fact Sheet