Independent Mortgage Companies Are Critical to Small Mortgage Access

Nonbank lenders dominate home lending, but banks and credit unions still play an important role

Independent mortgage companies—institutions that don’t accept deposits and focus instead on mortgage lending and servicing—have surpassed banks as the nation’s dominant lenders of small mortgages (those under $150,000). Banks and credit unions, which in 2004 originated over two-thirds of small mortgages, today produce less than half of these loans.

This trend bucks the conventional wisdom that small mortgages are primarily originated by small financial institutions—such as community banks and credit unions—and demonstrates that policymakers seeking to expand small mortgage access should focus on lowering origination costs for independent mortgage companies.

However, despite their rise, independent mortgage companies (also known as nonbanks) have not fully replaced the lending hole left by banks and credit unions. Even though nonbanks originate more loans to low-income borrowers and borrowers of color than banks and credit unions do, they still don’t issue enough small mortgages to satisfy consumer demand. This reflects the difficulties nonbanks face in reaching rural communities, where small mortgages are common. Therefore, in addition to lowering origination costs for independent mortgage companies, policymakers should focus on expanding the capacity of smaller lenders who operate in rural areas.

This two-pronged approach would help further the Biden administration’s stated goals of investing in underserved communities, increasing the availability of small mortgages, and helping Americans across the country purchase affordable, low-cost homes.

Independent mortgage companies do most of the nation’s small mortgage lending

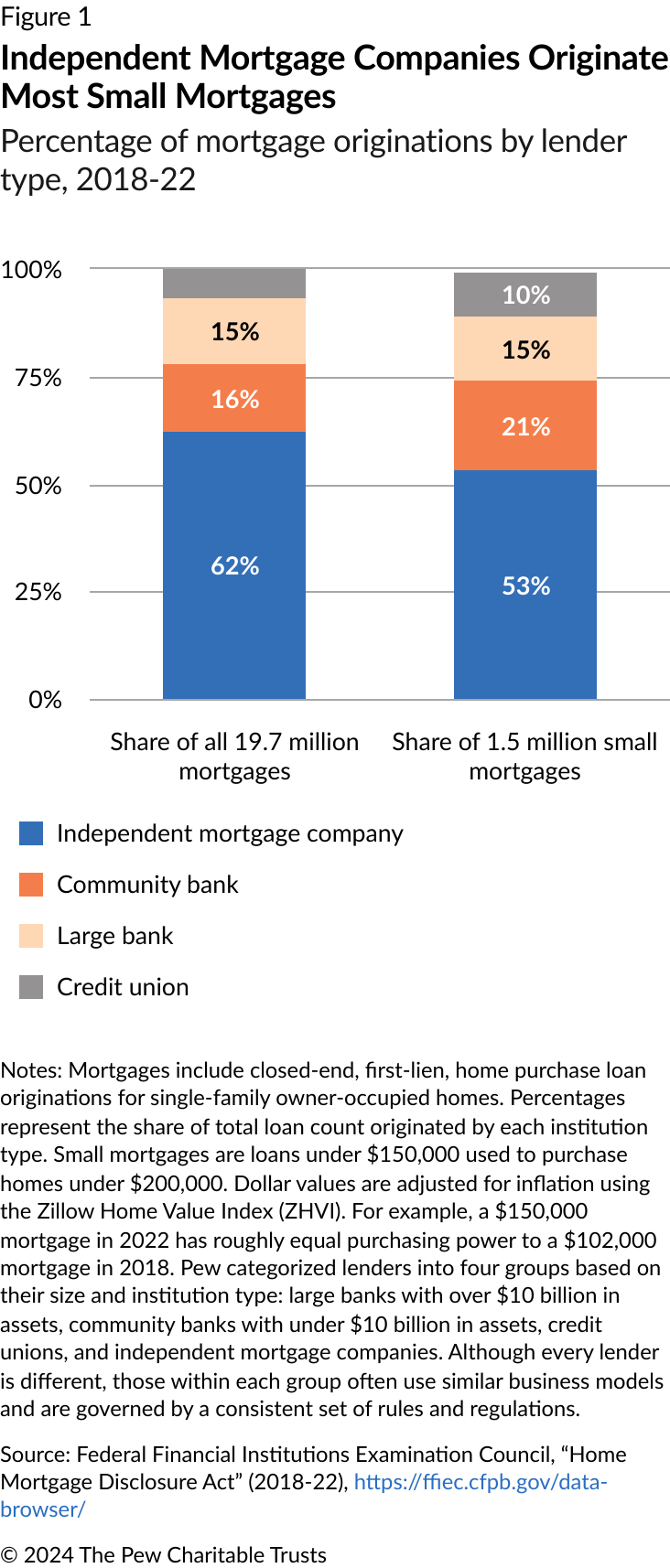

Since 2018, independent mortgage companies have originated more small mortgages than banks and credit unions combined; an analysis by The Pew Charitable Trusts of Home Mortgage Disclosure Act data found that 6,154 lenders issued 19.7 million home purchase mortgages between 2018 and 2022, including 1.5 million small mortgages. Independent mortgage companies were responsible for the bulk of this lending, originating 62% of all mortgages and 53% of small mortgages. (See Figure 1.) In contrast, community banks, large banks, and credit unions played more minor roles in the small mortgage market, originating 21%, 15%, and 10% of small mortgages, respectively.

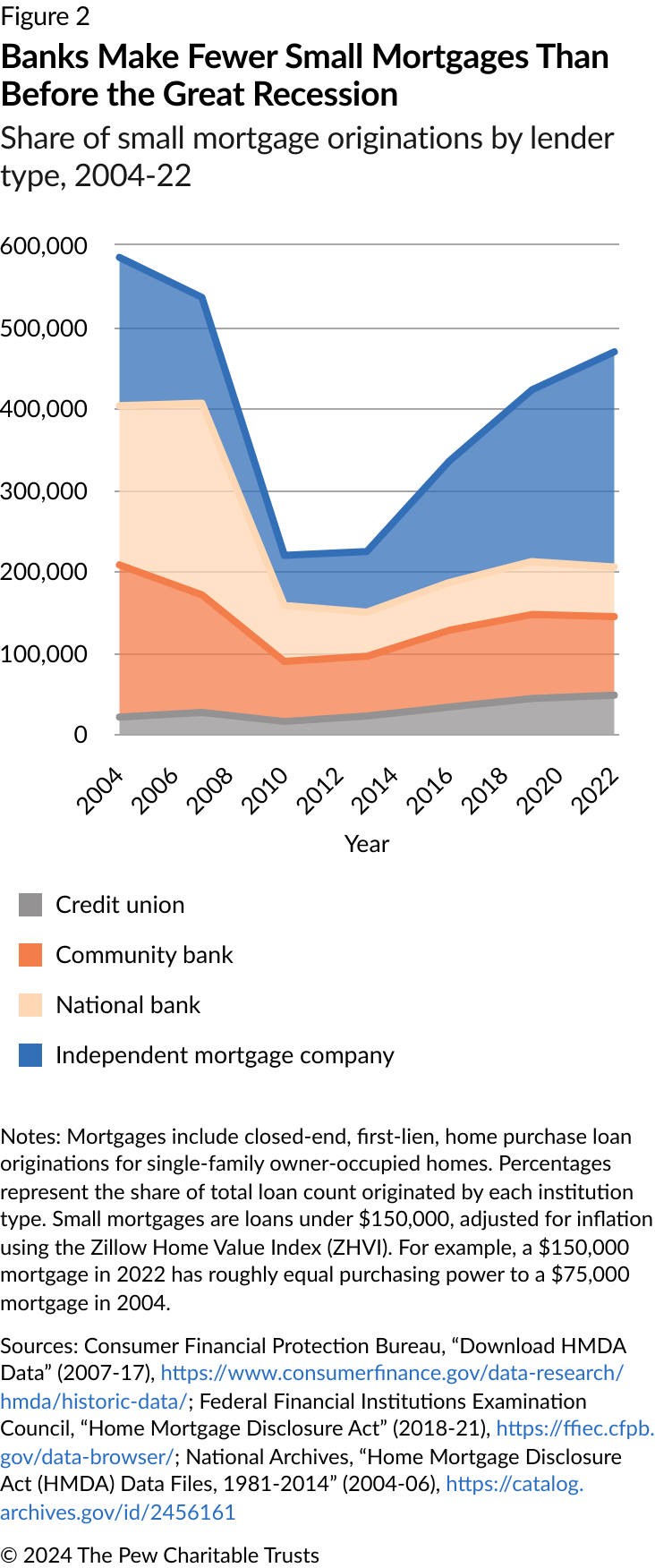

Although independent mortgage companies dominate the small mortgage market today, as recently as 2004 large and community banks issued a combined 65% of small mortgages compared with 31% by independent mortgage companies. (See Figure 2.) But after the Great Recession, banks scaled back mortgage lending, particularly of smaller loans; from 2010 to 2022, large banks reduced their small mortgage originations and community banks only modestly expanded theirs, despite an improving economic environment. Meanwhile, independent mortgage companies grew their small mortgage lending business from 62,000 loans per year in 2010 to 264,000 loans per year in 2022. A similar trend took place in overall mortgage lending, with banks losing market share and independent mortgage companies taking their place.

Several factors help explain why banks retreated from the mortgage market and why the number of community banks originating mortgages fell by more than half between 2004 and 2022. Many banks dealt with financial struggles resulting from billions of dollars of troubled assets, fines from legal settlements, and new and stricter regulatory requirements that improved the stability of the mortgage market and the safety of loans for borrowers, but also increased the cost for lenders to originate a mortgage. For example, community banks became subject to at least 157 new rules and regulations between 2007 and 2019—which, for some lenders with small compliance units, made it more difficult and expensive to adhere to the new regulations.

Not only do independent mortgage companies originate a majority of the nation’s small mortgages, but research shows that they originate a larger proportion of their loans to borrowers of color and to low- and moderate-income borrowers than do banks and credit unions. In part, this is because nonbanks originate about 89% of loans insured by the Federal Housing Administration, which have more flexible down payment and underwriting requirements than conventional loans and thus enable better mortgage access for historically underserved communities.

However, the shift in lending away from banks and credit unions and toward independent mortgage companies may impede small mortgage availability over time. Data shows that for every 100 loans issued by independent mortgage companies from 2018 to 2022, just six were small mortgages. In contrast, credit unions and community banks issued 12 and 10 small mortgages per 100 originations, respectively. (See Figure 3.) This suggests that for every 100 loans that shifted away from credit unions and community banks and toward independent mortgage companies, between four and six small mortgages were lost.

Nonbanks originate fewer small mortgages as a share of their portfolio in part because of challenges reaching rural borrowers. From 2018 to 2022, independent mortgage companies originated a majority of all mortgages in urban areas (63%) and in rural areas (52%), but credit unions and community banks did comparatively more lending in rural communities: These lenders accounted for 35% of all loans made in rural areas but just 22% of mortgages made in urban areas. In part, this reflects the fact that rural borrowers often rely on physical branches of banks and credit unions, and independent mortgage companies typically operate using a web-centric business model that may be challenging for rural borrowers who lack access to broadband internet.

Policymakers must address small mortgage challenges for banks and nonbanks

In general, policies that reduce origination costs for nonbanks or expand their lending capacity will have the largest impact on small mortgage access. Policymakers could consider updating federal housing plans to focus on these loans and examining ways to streamline regulations that add loan costs without improving the safety for borrowers. Even small cost reductions could help meaningfully increase the availability of small mortgages.

Policymakers should also consider solutions that expand the loan production capacity of community banks and credit unions, which originate more small mortgages as a share of their business than independent mortgage companies. This could involve initiatives to expand the use of efficiency-improving loan technology or more active engagement from government-sponsored enterprises such as Fannie Mae and Freddie Mac, which purchase mortgages in the secondary market—an important source of funding for lenders.

There’s no one-size-fits-all approach when it comes to increasing small mortgages across the market, but a combination of policies focused on reducing costs for independent mortgage companies and expanding the capacity of banks and credit unions in rural areas would go a long way in helping to ensure that all Americans have access to safe and affordable mortgage financing.

Adam Staveski is a senior associate and Tracy Maguze is an officer with The Pew Charitable Trusts’ housing policy initiative.

America’s Overdose Crisis

Sign up for our five-email course explaining the overdose crisis in America, the state of treatment access, and ways to improve care

Sign up

Financing a Low-Cost Home Should Be Easier

FHA Loans Don't Reach Black Buyers of Manufactured Homes

Small Mortgages Are Too Hard to Get

ADDITIONAL RESOURCES

Fact Sheet

Podcast