American Families Face a Growing Rent Burden

High housing costs threaten financial security and put homeownership out of reach for many

Overview

Nearly 43 million U.S. households rented their homes in 2016, including about 9 million households that were formed over the preceding decade, according to the Harvard Joint Center for Housing Studies. Demand for rental properties has increased across age and socio-economic groups since 2008. Recent research indicates that although some of those increases can be explained by population shifts, a significant portion is the result of declines in homeownership since the Great Recession.

In the aftermath of the 2007-09 downturn, households that rent have been slower to transition to homeownership than they were before the recession and housing crisis. Many families struggle to save enough for a down payment or lack a sufficiently strong credit profile to meet the stringent underwriting standards that were put in place in the wake of the crisis. But some renters—even with down payment assistance programs— simply cannot afford the monthly payments for homes that in many areas are commanding prices near those of the 2007 market peak.

But as more households rely on renting for their long-term housing needs, they are finding the cost of renting increasingly onerous. The steadily rising demand for rental properties over the past decade has reduced vacancy rates to near historic lows, fueling a rapid increase in rental market prices that has outpaced household incomes for many families. This imbalance is contributing to high rates of “rent burden,” which for the purposes of this analysis is defined as spending 30 percent or more of pretax income on rent. Rent-burdened households have higher eviction rates, increased financial fragility, and wider use of social safety net programs, compared with other renters and homeowners. And as housing costs consume a growing share of household income, families must cut back in other areas.

The increasing share of income that goes toward rent may have broad implications for the long-term stability of renter households and for the economy as a whole. To better understand this growing threat and its potential consequences, The Pew Charitable Trusts undertook an in-depth study of the country’s rent-burdened households. Using the Panel Study of Income Dynamics (PSID), a data set of U.S. household finances developed by the University of Michigan, Pew examined how increasing rent affected the ability of American households to use financial services, accumulate savings, and transition to homeownership between 2001 and 2015. Key findings include:

- In 2015, 38 percent of all “renter households” were rent burdened, an increase of about 19 percent from 2001.

- The share of renter households that were severely rent burdened—spending 50 percent or more of monthly income on rent—increased by 42 percent between 2001 and 2015, to 17 percent. Increasing rent burdens were driven in part by year-over-year growth in gross rent—contract price plus utilities—that far exceeded changes in pretax income, which means that after paying rent, many Americans have less money available for other needs than they did 20 years ago.

- In 2015, 46 percent of African-American-led renter households were rent burdened, compared with 34 percent of white households. Between 2001 and 2015, the gap between the share of white and African- American households experiencing severe rent burden grew by 66 percent.

- Senior-headed renter households are more likely than those headed by people in other age groups to be rent burdened. In 2015, about 50 percent of renter families headed by someone 65 or older were rent burdened, and more than a fifth were severely rent burdened.

- Rent-burdened families are also financially insecure in many other ways:

- Nearly two-thirds (64 percent) had less than $400 cash in the bank; most (84 percent) of such households are African-American-headed.

- Half had less than $10 in savings across various liquid accounts, while half of homeowners had more than $7,000.

- Fewer rent-burdened households transitioned from renting to owning in 2015 than in 2001. Households that were rent burdened for at least a year were less likely to buy a home than those that never experienced a rent burden.

The growing number of rent-burdened households suggests that a rising share of Americans may be experiencing serious financial fragility. Policymakers should be aware of the increase in rent burdens because if the trend continues, it could limit household consumption and reduce the economic mobility and financial resiliency of American families.

In the aftermath of the 2007-09 downturn, households that rent have been slower to transition to homeownership than they were before the recession and housing crisis. Many families struggle to save enough for a down payment or lack a sufficiently strong credit profile to meet the stringent underwriting standards that were put in place in the wake of the crisis. But some renters—even with down payment assistance programs— simply cannot afford the monthly payments for homes that in many areas are commanding prices near those of the 2007 market peak.

Renting is on the rise

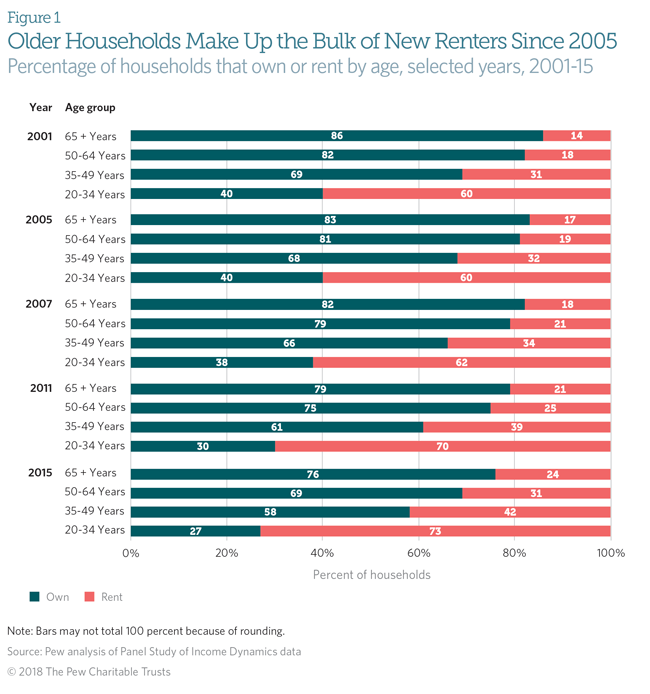

From 2001 to 2015, the demand for rental housing grew dramatically, driving prices to historic highs. In 2015, nearly 43 million American households lived in rental housing, an increase of 9.3 million since 2004 and the largest rise since 1970, when baby boomers (born between 1946 and 1964) were coming of age.1 The share of households that rent has increased by at least 10 percentage points since 2001 for all age groups. However, unlike the early 1970s when young families drove the increase in renting, the 2015 spike is largely propelled by those 55 and older, largely baby boomers, who are responsible for a 4.3 million jump in the number of renters since 2005.2 (See Figure 1.)

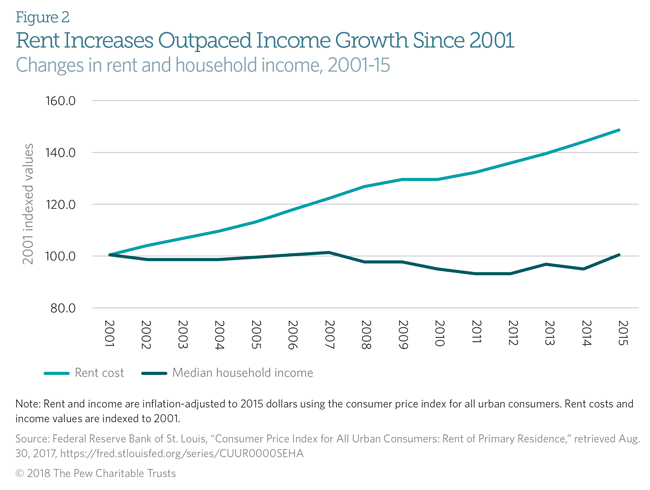

As their numbers grow, American renter households are also spending more on housing. Between 2001 and 2015, the median rent rose from $512 a month to $678, a 32 percent increase.3 These figures exclude the cost of utilities, though, and therefore do not fully measure the increase in expenditures. And year-over-year growth in gross rent far exceeds changes in pretax income during the same period. Since 2001, gross rent has increased 3 percent a year, on average, while income has declined by an average of 0.1 percent annually, falling from $56,531 in 2001 to $56,516 in 2015. (See Figure 2.) This widening gap between rent and income means that after paying rent, many Americans have less money available for other needs than they did 20 years ago.4

Short Supply and Heavy Demand

The home purchase and rental markets are closely linked, as changes in one directly affect the other. If the supply of homes for sale can meet or exceed the demand by potential buyers, experts would expect rental supply to increase and rents to decline. Conversely, if the demand for ownership is not met because of limited supply, unaffordable prices, or tight credit, experts would expect rental stocks to dry up and rents to increase and consume a larger share of household income. The rent data featured in this report reflect a combination of factors: For the years studied, declining homeownership and demographic shifts were the primary drivers of rental demand.*

The nation’s homeownership rate peaked in 2004, when 69 percent of Americans owned their homes.† The recession suppressed home purchases and led to millions of families losing homes to foreclosure, which together helped cut the ownership rate to 63 percent by 2015.‡ Over the years before the crisis, 2001-05, 20 percent of renter households reported becoming homeowners; after the recession, 2009-15, that figure was just 13 percent, a decline of 40 percent. With far fewer renter households becoming owners since the recession, demand for rental homes has grown faster than the supply.

Some experts have suggested that changing attitudes are fueling the decline in ownership, with younger adults preferring to rent.§ However, a 2016 Pew Research Center survey found that 72 percent of renters said they want to buy a home at some point, and most cited financial reasons when asked why they rent.|| Another recent public opinion poll asked renters ages 18-34 why they were not buying homes, and 57 percent said they could not obtain a mortgage.# On the other hand, a recent survey of Americans over 55 found that 71 percent of those who plan to move again said they intended to rent rather than buy.** Most renters over 55 cited cost as a driver of their decision and said it makes the most sense for people their age to rent.††

During the recession and housing crisis, 8 million to 10 million properties were foreclosed. The widespread loss of homes has had a lasting impact on the housing market. According to the National Association of Realtors, less than a third of these households will return to homeownership.‡‡ Some of these families have seen their economic situations improve but, in part because underwriting standards tightened significantly after the crisis, they still lack

the credit profiles necessary to qualify for mortgages. In fact, some experts estimate that 6.3 million additional mortgages would have been issued if not for tighter credit standards between 2009 and 2015.§§ Further, families that went through a foreclosure, short sale, bankruptcy, or deed in lieu of foreclosure face additional hurdles, typically including being ineligible for Federal Housing Administration-insured mortgages for three years and the financial challenges arising from rents that are increasing faster than inflation. Many of those would-be owners are renting, further reducing rental supply and raising rents.

With fewer people transitioning from renting to owning, the stock of available rental properties is declining. As of late 2016, the national rental vacancy rate was about 7 percent,|| || which is among the lowest levels since the 1980s, when the rate reached a historic low of 5 percent. At the same time, owners are staying in their homes longer: Between 1985 and 2008, the median tenure of an owner in a home (that is, time residing there) before selling was six years, but since 2009 that has increased to nine years.## The recession left millions of families in housing that was worth less than the amount still owed on the mortgage, effectively forcing them to stay in their homes longer. As of 2016, an estimated 3.2 million to 4 million U.S. homes were valued below the mortgage balance.***

The housing crisis also disrupted the single-family rental property market by altering the traditional owner-to-landlord cycle. Individual investors who convert their starter homes into a rental property after upgrading to a different home have traditionally accounted for a large share of the single-family rental market. The proportion of rental properties owned by individual investors was about 87 percent in 2015, which though still high is down from the peak of 92 percent in 1991.†††

In summary, the increased demand for rental properties and their limited supply, along with the lingering effects of foreclosures, demographic changes, and a decline in the rate of renters transitioning to owning, have led to higher rents.‡‡‡ In turn, rising rental prices have

outpaced wage increases and inflation across America, leading to a growing number of rent- burdened households.

* This report focuses on the factors that Pew believes have the most impact on the housing market. Rising rental demand may also be the result of credit scoring issues, lack of savings, quality of rental properties, location of available rental properties, inability to save, and eviction laws, among other causes.

† U.S. Census Bureau, “Quarterly Residential Vacancies and Homeownership, First Quarter 2017” (April 27, 2017), https://www.census.gov/housing/hvs/files/qtr117/Q117press.pdf. The Census Bureau announced the following residential vacancies and homeownership statistics for first quarter 2017: https://www.census.gov/housing/hvs/files/currenthvspress.pdf.

‡ Ibid.

§ Chris Matthews, “Young People Can Afford Homes, They Just Don’t Want to Be Homeowners,” Forbes, Aug. 18, 2015, http://fortune.com/2015/08/18/young-people-can-afford-homes-they-just-dont-want-to-be-homeowners.

|| Richard Fry and Anna Brown, “In a Recovering Market, Homeownership Rates Are Down Sharply for Blacks, Young Adults,” Pew Research Center (2016), http://www.pewsocialtrends.org/2016/12/15/in-a-recovering-market-homeownership-rates-are-down-sharply-for-blacks-young-adults.

# Fannie Mae, “Fannie Mae National Housing Survey: What Parents Tell Us About Their Adult Children Living at Home” (2014), http://www.fanniemae.com/resources/file/research/housingsurvey/pdf/ nhsjuly2014presentation.pdf.

** Freddie Mac, “Americans 55+ Assess Current and Future Housing Options” (2016), http://www.freddiemac.com/ research/consumer-research/20160628_five_million_boomers_expect_to_rent_next_home_by_2020.html.

†† Ibid.

‡‡ Laura Kusisto, “After Foreclosure, Fewer Buy Homes,” The Wall Street Journal, April 21, 2015, http://online.wsj.com/ public/resources/documents/print/WSJ_-A002-20150421.pdf.

§§ Laurie Goodman, Jun Zhu, and Bing Bai, “Overly Tight Credit Killed 1.1 Million Mortgages in 2015,” Urban Institute (2016), https://www.urban.org/urban-wire/overly-tight-credit-killed-11-million-mortgages-2015.

|| || U.S. Census Bureau, “Quarterly Residential Vacancies and Homeownership, Third Quarter 2016.”

## Keeping Current Matters, “How Long Do Most Families Stay in Their Home?” accessed Oct. 12, 2017 https://www.keepingcurrentmatters.com/2017/02/28/how-long-do-most-families-stay-in-their-home.

*** Gail MarksJarvis, “Chicago Among Cities With Largest Share of Underwater Homeowners, Studies Show,” Chicago Tribune, June 9, 2016, http://www.chicagotribune.com/business/ct-underwater-homeowners-chicago-0610-biz- 20160608-story.html; Diana Olick, “How Are Millions Still Underwater as Home Prices Rise?” CNBC, April 4, 2016, https://www.cnbc.com/2016/04/04/how-are-millions-still-underwater-as-home-prices-rise.html. ††† U.S. Census Bureau, “Who Owns the Nation’s Rental Properties? Statistical Brief, March 1996, https://www.census.gov/prod/1/statbrief/sb96_01.pdf; Ronda Kaysen, “Smaller Housing Markets Lure Individual Investors,” The New York Times, July 28, 2017, https://www.nytimes.com/2017/07/28/realestate/smaller-housing-markets-lure-individual-investors.html?_r=0.

‡‡‡ Pedro Gete and Michael Reher, “Systemic Banks, Mortgage Supply, and Housing Rents,” 6 (paper presented at the annual meeting of the American Economic Association, Chicago, Jan. 4–8, 2017), https://www.aeaweb.org/conference/2017/preliminary/1668?page=11&per-page=50.

Measuring rent burden

Today, more families are putting a larger share of their income toward rent. In the Housing and Urban Development Act of 1969, Congress defined housing affordability as monthly costs of no more than 25 percent of household income. During the 1981 budget crisis, however, Congress increased the amount to 30 percent or less of household income to reduce the amount the federal government spent on housing subsidies.

But that definition has its critics,5 because it may not capture the true cost of renting, for several reasons. First, the federal figure is based on annual pretax, post-transfer income—total household income plus benefits from government programs such as Social Security—which is often meaningfully larger than after-tax, post-transfer income and so produces a lower estimate of cost burdens than the after-tax figure. Second, estimates that rely on gross rent fail to capture differences in housing quality, which affect renters’ costs. In addition, variations across data sets and methods of collecting and calculating income, rent, and gross rent can result in substantial variation in cost estimates.

Given this debate, Pew opted to use a conservative calculation for rent burdens. The findings in the subsequent sections of this paper are based on the concepts of gross rent and pretax, post-transfer income, including housing assistance. Renters who do not pay rent are considered to not be burdened by rent, and those without income are assumed to be rent burdened. These choices, combined with the selected data sets, result in a highly conservative estimate—probably the bare minimum percentage of households that experience rent cost burdens. Regardless of the methodological differences, however, most studies come to the same conclusion: The number of people who are financially constrained by the cost of rent is increasing. (See the methodology for more information.)

A closer look at rent-burdened Americans

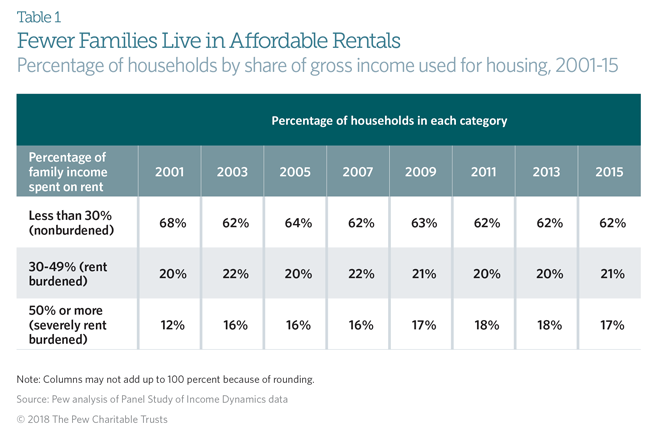

In 2015, at least 38 percent of renter households were rent burdened, compared with 32 percent in 2001, an increase of 19 percent over that period.6 (See Table 1.) Further, the number of severely burdened families grew by 42 percent—to 17 percent of all renters—during the same period. That 11 million Americans have so little slack in their budgets is troubling, but further study is needed to fully understand how rent burdens affect long-term household financial security and economic mobility.7 Because of the PSID’s sampling and methodology, this report’s estimated percentage of renter households that are burdened should be viewed as the most conservative approximation available, representing the minimum assessment of rental burdens and not the maximum.

Demographics

Race

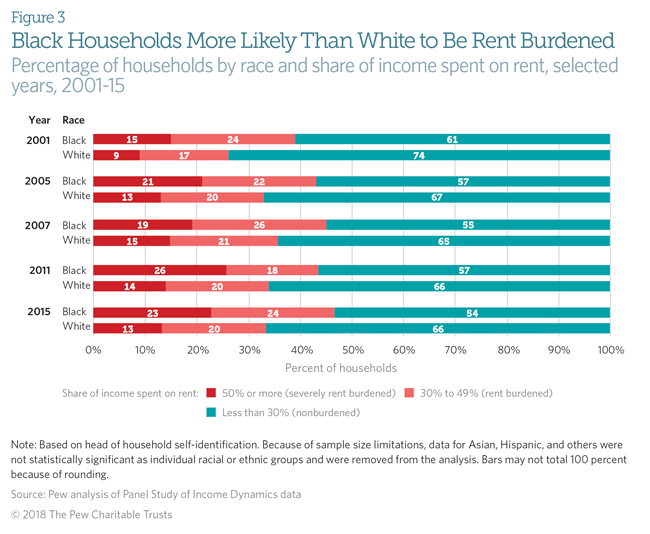

The percentages of African-American and white renter families that were rent burdened grew from 2001 to 2015, but although African-American renter households were consistently more likely to be burdened, the gap between the two groups remained roughly stable. However, the difference between the shares of white and black renter households that were severely rent burdened widened by 66 percent over that period. In 2001, 13 percentage points separated the shares of white and African-American renter households that were burdened: 26 and 39 percent, respectively; the gap between severely rent-burdened white and black renters was 6 percentage points: about 9 percent versus 15 percent, respectively. (See Figure 3.) By 2015, the share of African-American-led renter households that were burdened had risen to 46 percent and severely burdened, 23 percent; among white renter families, the figures were 33 and 13 percent, respectively.

Income

For families in the bottom 20 percent of household income, for whom rent burdens are most pronounced, the racial disparities are even more substantial. The 2015 median income for all bottom-quintile households was $11,701, but medians differed starkly across racial groups: $12,700 for white families and $11,000 for African- Americans, a difference of $1,700, or more than 13 percent. However, black families in this income group paid slightly higher median rent in 2015 than did their white counterparts: $6,024 versus $5,940 annually.

Age

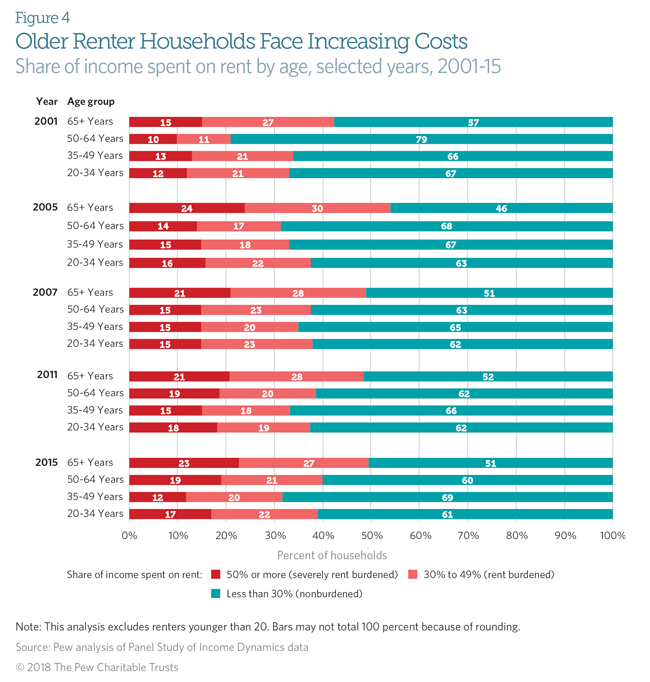

Although Americans of all ages rent, older households tend to be more rent burdened than younger families. In 2001, 43 percent of households headed by someone 65 or older were rent burdened, compared with 33 percent for 20- to 34-year-olds, 34 percent for 35- to 49-year-olds, and 21 percent for 50- to 64-year-olds. (See Figure 4.) Over time, the proportion of rent-burdened households rose for all age groups, but older households remained the most affected. By 2015 the proportion of households that were rent burdened increased to 39 percent among 20- to 34-year-olds, 31 percent for 35- to 49-year-olds, 40 percent for 50- to 64-year-olds, and about 50 percent of those 65 and older. Further, more than a fifth (23 percent) of households 65 and older were severely rent burdened in 2015.

Financial health of cost-burdened renters

Rent-burdened families are financially insecure in many other aspects of their lives, too. They often have trouble meeting basic consumption needs, frequently rely on public assistance, and typically have little connection to the banking system and limited savings.

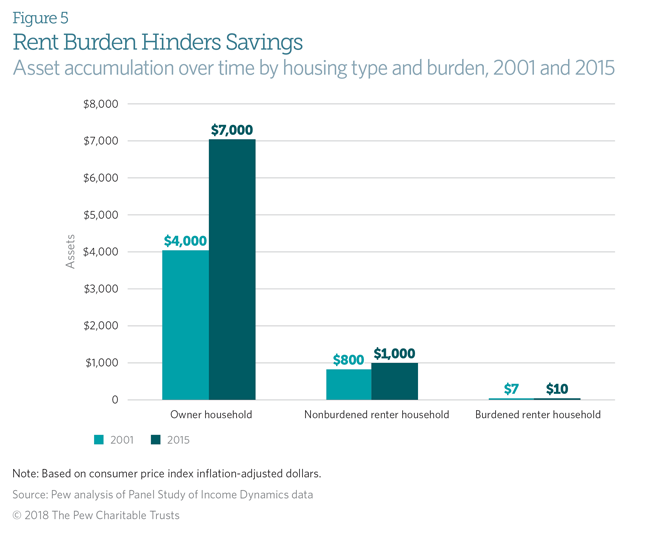

In general, renter households have less money across their financial accounts than do nonburdended families and those that own their homes.8 In 2001, half of rent-burdened households had less than $10 in savings, while the median non-rent-burdened family had $800 in inflation-adjusted dollars, and half of homeowners had more than $4,000.9 By 2015, the savings of nonburdened renter families had increased to slightly more than $1,000 at the median10 and that of owner households had nearly doubled, to $7,000. But rent-burdened households still had less than $10. (See Figure 5.)

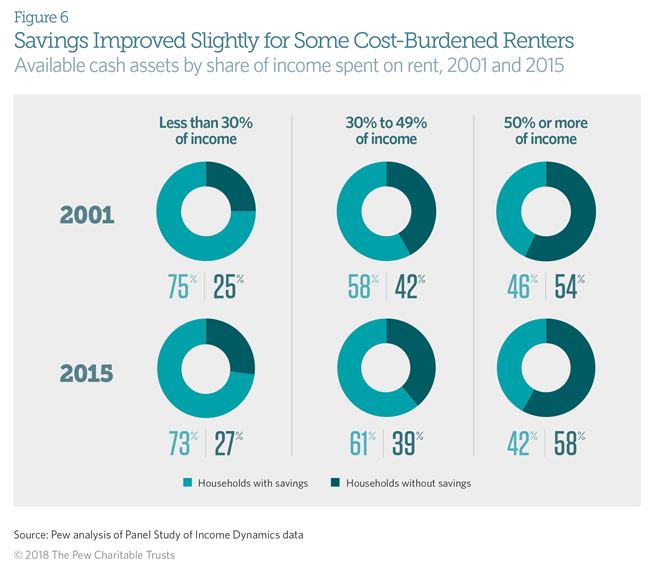

Similarly, rent-burdened families are generally less likely than nonburdened renter households to have money in an account at a financial institution. In 2001, 33 percent of all U.S. renter households had no money in an account; by 2015, it was 36 percent. In 2001, 42 percent of rent-burdened families were without savings; by 2015, it had declined to 39 percent. For the severely rent burdened, however, the story went from bad to worse: The percentage without cash assets increased from 54 percent in 2001 to 58 percent in 2015. (See Figure 6.)

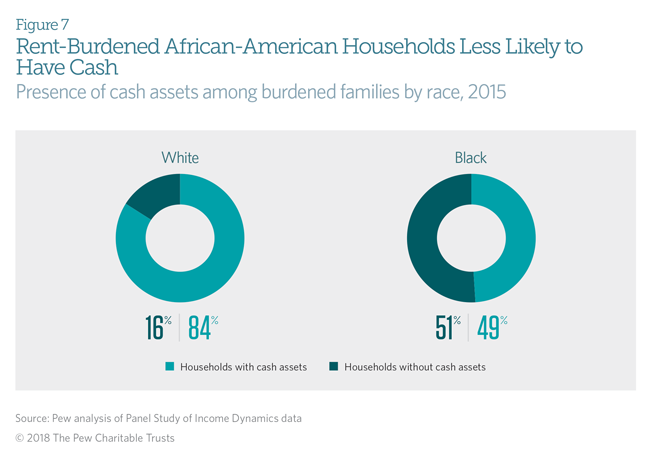

Rent-burdened families clearly have lower savings than do the nonburdened. Overall, 64 percent of rent-burdened families, including the severely burdened, had less than $400 in savings in 2015. When considered by race, however, stark differences emerge: A vast majority (84 percent) of African-American rent-burdened households had less than $400, compared with 54 percent of similar white households. And as of 2015, more than half of black rent-burdened households had no savings versus just 16 percent of burdened white households. (See Figure 7.) As previous Pew research has shown, households that lack liquid savings have more difficulty coping with unexpected expenses and income volatility, making them more vulnerable to long-term material hardship.

The percentage of severely rent-burdened African-American households without savings improved slightly from 2001 to 2015, dropping from 81 to 79 percent. Among rent-burdened black families, households with heads under age 34 had the lowest savings rate in 2015: Only 14 percent had money in a financial institution. The only age group that had a higher savings rate in 2015 than in 2001 was families 65 and older. These low savings rates suggest that rent-burdened families have marginal attachment to the traditional banking system and that many of these households may rely on nonbank services such as check cashers and high-cost, small-dollar lenders to meet their financial needs.11

Overall, 64 percent of rent-burdened families, including the severely burdened, had less than $400 in savings. When considered by race, however, stark differences emerge: A vast majority (84 percent) of African-American rent-burdened households had less than $400, compared with 54 percent of similar white households. As previous Pew research has shown, households that lack liquid savings have more difficulty coping with unexpected expenses and income volatility, making them more vulnerable to long-term material hardship.

Financially constrained, rent-burdened families can have difficulties paying for core needs such as food, transportation, health care, and clothing. For example, in 2015, a severely rent-burdened two-earner, one-child household in which both earners made the federal minimum wage would have had about $250 a week in pretax dollars after rent to cover child care, transportation, food, health insurance, and other necessities.12 A single mother who was severely rent burdened would have had about $124 pretax, or about $17 a day, after the rent was paid.

Long-term financial impact of rent burdens

High rents are a problem for a growing proportion of American households. However, data are limited on how increasing rents affect families’ finances in the long run. The impacts on household balance sheets and future wealth may depend on how long a family rents or is burdened by rent.

To assess the effects of renting duration and the long-term financial implications of being rent burdened, this section of the report narrows in scope to look only at families that participated in the survey for the full 15 years. Among those that rented for at least one year between 2001 and 2015, the average number of years spent renting was eight, with 50 percent of households renting between four and 13 years. At the margins, 20 percent of families rented for 14 years or more, and 17 percent of families rented for two years or less.

Fifty-six percent of all renters spent at least one year being rent burdened,13 and about 34 percent experienced rent burdens for three or more years. The average duration of a rent burden was about three years.14 Further, being rent burdened in one year was correlated with being rent burdened the next year. Among renter households that spent one year with rent burdens, 74 percent endured two to six additional years struggling with rent.

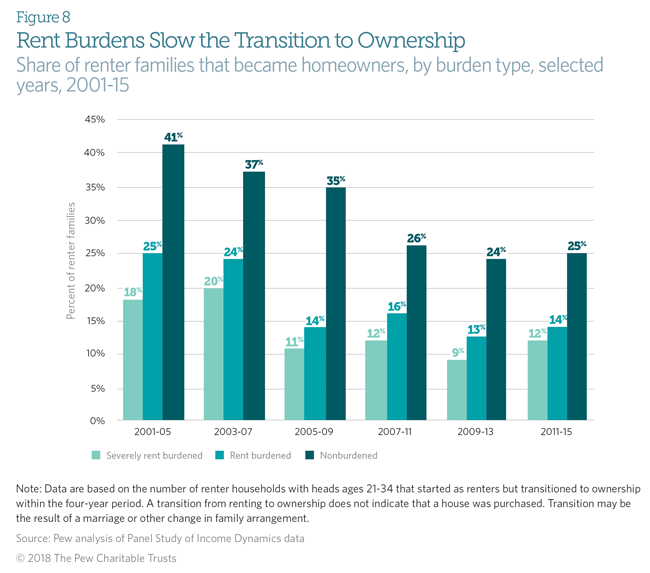

Despite the transitory nature of being rent burdened, even a short spell may have an effect on the potential for homeownership. To get a better idea of how being rent burdened is associated with homeownership, Pew looked at household housing status in one year and then looked at the same households’ housing status four years later. Nationally, the percentage of prime buying-age renter households—those headed by people ages 21-34— that transitioned from renting to owning declined from 26 percent in 2001 to 16 percent in 2015. Even given that overall decrease, compared with households that were never burdened, rent-burdened households were less likely to become homeowners in the four years after a rent-burdened spell.

Among those prime buying-age renter families, 25 percent of those that were rent burdened in 2001 became homeowners by 2005, compared with 41 percent that had affordable rent in 2001. (See Figure 8.) Between 2003 and 2007, the figures were 24 and 37 percent, respectively. Between the start of the housing credit crisis in 2007 and 2015, only 14 percent of prime-age, rent-burdened households transitioned to homeownership each year, on average. Over the same period, an average of 1 in 4 nonburdened families became homeowners annually.

This decline in the share of cost-burdened renters attaining homeownership suggests that although the economy is recovering, rent-burdened households have a harder time accumulating savings and wealth today than they did before the crisis. Although this analysis is descriptive and cannot isolate causal relationships between these factors, the significant decline in rent-burdened households transitioning to ownership may be an early warning sign that those in the lower economic echelons will have a harder time becoming owners in the future.

Conclusion

An increasing number of American families are struggling to pay the rent, and that burden is affecting other parts of their balance sheets. In 2015, 7 million households spent more than half of their income on rent. Cost- burdened renter households have little to no financial slack in their budgets, which puts financial security out of reach for many. Even at moderate levels, being rent burdened erects barriers to saving and wealth building.

Renter households nationwide had little savings growth from 2001 to 2015 and now have a lower probability of transitioning to homeownership than they did 15 years ago. But by far the largest declines in ownership attainment have been among those who pay 50 percent or more of their household income for rent.

These findings on the increasing number of households affected by the cost of rent—as well as on the decline in homeownership—should raise concerns among policymakers at all levels of government who focus on family financial well-being and economic opportunity.

Methodology

Throughout this report, rent burden has been measured as having rent equal to or greater than 30 percent of a household’s gross income. This is different from the “greater than 30 percent of gross household income” metric used by the Harvard Joint Center for Housing Studies. Pew researchers conducted a sensitivity analysis using both measures and found no statistically significant differences, and in most cases the variations between the measurements were less than those induced by rounding.

All data reported in this paper are from the PSID, collected by the University of Michigan. The information has been collected from the same families continually since 1968; the study switched from annual to biennial data collection in 1997. Although additional samples have been added periodically over the years, the data used in this analysis come only from the study’s original families from every survey conducted from 2001 to 2015. Family income in the PSID includes the total earnings, transfers, investments, and other nonwage sources of money as reported by all family members for the previous calendar year. Some recoding and cleaning was performed on the income data. The few cases of negative and zero family income in a given survey year were recoded to $1.

The data include 122,440 family-years. When restricted to households that were in the observation period for 10 or more years, the number of family-year observations decreases to 105,298. About 15,305 households are represented in the data for each year.

All statistics relating to household savings are based on the imputed values of the following PSID survey question:

“IMP WTR CHECKING/SAVING (W27) 01 ”

W27. Do [you/you or anyone in your family] have any money in checking or savings accounts, money market funds, certificates of deposit, government savings bonds, or Treasury bills—not including assets held in employer- based pensions or IRAs?

The values may not be monies designated for savings but are considered savings because they had not been consumed at the time of the survey.

Additionally, all questions related to whether a household rents or owns are based on the following PSID question:

A19. Do (you (or anyone else in your family living there) / they (or anyone else in the family living there)) own the (apartment/mobile home/home), pay rent, or what?

For the purpose of this analysis, respondents who answered “neither owns or rents” are considered to be renter households. Sensitivity testing was conducted to determine if the coding decision had a material effect, and the results indicated it did not.

Endnotes

- Harvard Joint Center for Housing Studies, “The State of the Nation’s Housing, 2016”( 2016), http://www.jchs.harvard.edu/research/state_nations_housing; Freddie Mac, “Americans 55+ Assess Current and Future Housing Options” (2016), http://www.freddiemac.com/research/consumer-research/20160628_five_million_boomers_expect_to_rent_next_home_by_2020.html.

- Harvard Joint Center for Housing Studies, “The State of the Nation’s Housing, 2016.”

- This figure was calculated using only 2015 PSID data for those who paid at least $1 a year in rent and was adjusted for inflation to 2017 dollars using the CPI deflator. Stricter definitions would meaningfully raise the median and mean rents.

- According to the U.S. Census Bureau’s American Community Survey, the median rental price was $934 (real dollars) as of 2014, up $72 dollars (8 percent) since 2005. Our published numbers are based on the analysis of PSID data.

- U.S. Department of Housing and Urban Development, “Rental Burdens: Rethinking Affordability Measures,” The Edge, accessed Oct. 12, 2017, https://www.huduser.gov/portal/pdredge/pdr_edge_featd_article_092214.html.

- The PSID data used for this report follows the same families over time, which may result in less variation in the number of renter households found to be burdened and probably produces a very conservative estimate of the number of rent-burdened households.

- U.S. Department of Housing and Urban Development, “Affordable Housing: Who Needs Affordable Housing?” accessed Oct. 12, 2017, https://portal.hud.gov/hudportal/HUD?src=/program_offices/comm_planning/affordablehousing.

- For convenience, this paper refers to these monies as savings, but in actuality they are funds held in financial institutions that can be used for any purpose. (PSID QUESTION: Do you [or anyone in your family living there] have any money in checking or savings accounts, money market funds, certificates of deposit, government savings bonds, or Treasury bills?)

- In 2001, the mean value of savings for non-rent-burdened homes was $7,300, and for households that owned their homes it was

$34,900, both in constant dollars.

- Mean value of savings for nonrent cost-burdened homes was $15,300 in constant dollars in 2015.

- Federal Deposit Insurance Corp., “2015 FDIC National Survey of Unbanked and Underbanked Households” (2016), https://www.fdic.gov/householdsurvey/2015/2015report.pdf.

- This figure is based on the average annual hours actually worked per worker (1,790 in 2015) using data from the Organization for Economic Cooperation and Development. OECD, “Average Annual Hours Actually Worked Per Worker,” accessed Oct. 12, 2017, https://stats.oecd.org/Index.aspx?DataSetCode=ANHRS.

- This figure includes only respondents who were renters and were surveyed for at least 10 years.

- Moving in with a friend or relative and other undisclosed situations were included in terminations of the rental period. This inclusive definition may result in an underestimation of the length of rent burdens because being homeless is not necessarily costless and the likely cost of long-term homelessness would create an economic situation similar to or worse than being severely rent burdened. Some portion of those terminating their rental may have done so through loss of housing.