Employer Reactions to Leading Retirement Policy Ideas

Insights from Pew's national survey of small business

Note: The overview for this report was updated on July 28 , 2017 to reflect the correct percentage of leaders at businesses without retirement plans who said that having access to an online marketplace exchange would encourage them to offer a plan. The correct number is 56 percent.

Overview

The ease with which private sector workers can routinely put aside earnings for their retirement has made the workplace an effective place to accumulate money for the post-work years. Still, only about half (52 percent) of businesses with fewer than 100 employees offered retirement plans in 2012, leaving millions of American workers with no opportunity to save on the job.1 Boosting that percentage is essential and is probably the most feasible path to increase retirement savings, considering how few people take advantage of savings arrangements outside of work.

With a lack of action at the federal level, policymakers in many states are looking for ways to increase access to retirement plans in the workplace. These legislative efforts are intended to boost retirement savings while also helping to reduce poverty and the demand for government social assistance that can strain state budgets. Creative approaches to encourage retirement savings are needed at a time when the nation’s population is aging, fewer workers have access to traditional pension plans, and many American do not set aside a sufficient amount for retirement. Only about a fifth of Americans (22 percent) are “very confident” that they will have enough money for a comfortable retirement.2

So far, states have pursued three basic approaches. Some are implementing state-sponsored individual retirement account (IRA) programs that automatically enroll workers who don’t have access to employer-based plans—though workers can opt out. Others allow employers to band together to offer a retirement plan, sharing costs and liabilities. And a third group of states is establishing online marketplaces where employers can easily compare and select from plans that meet basic standards offered by private financial firms.

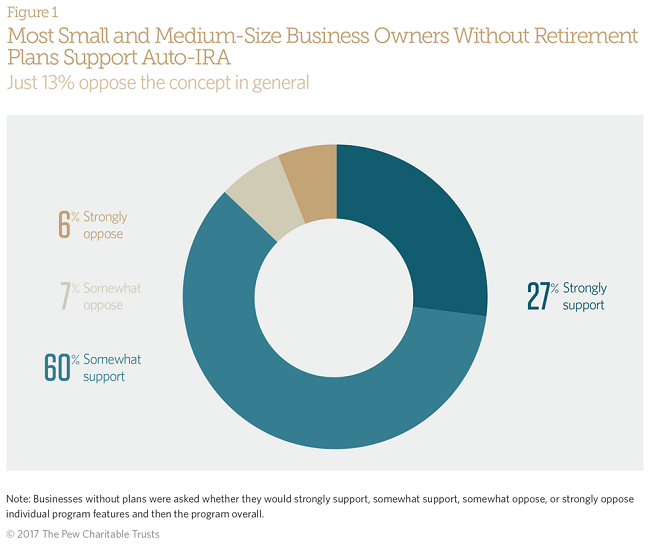

A key to the success of these programs will be how they are received by small and midsize businesses and their workers. To help inform policymakers considering the three approaches, The Pew Charitable Trusts in 2016 surveyed over 1,600 small and medium-size private sector businesses (those with five to 250 employees)—some of which sponsor plans.

The survey was designed to help better understand the barriers to and motivations for offering retirement plans, and to get employers’ views on policy initiatives; few similar surveys have been conducted over the past decade. The responses generally show strong interest in offering retirement benefits, as well as support for various policy initiatives intended to boost employee savings.

Among the key findings:

- Nearly 9 in 10 (87 percent) of small to midsize employers that do not offer a retirement plan support the concept of an IRA program with automatic enrollment, known as an auto-IRA.

- Most of those without plans back specific elements of the auto-IRA approach; 92 percent supported providing employees with access to a retirement plan as well as allowing employees to stop or change contributions at any time.

- Of the businesses supporting auto-IRAs, 76 percent said they did so with the belief that such a program would help their employees. Those that opposed this approach provided a mix of reasons, most often citing concerns about the concept of automatic enrollment. A third said they didn’t think their employees wanted, or needed, a retirement plan.

- While general support was high, firms with shrinking workforces or earnings appear to be less concerned with retirement benefits than with their companies’ basic financial viability. Businesses without plans that had recently downsized or recorded a decrease in earnings were more likely to oppose or offer limited support for auto-IRAs than to strongly support them.

- Most employers preferred that private firms, such as mutual fund companies or insurers—as opposed to state governments—administer an auto-IRA program, perhaps a sign of concerns about governments’ ability to operate such programs effectively. The reservations also could reflect limited familiarity with the public-private partnership structure typically used with these programs.

- Businesses that outsource their payroll—nearly half of the sample—were more likely to somewhat support state sponsorship of auto-IRAs than oppose it, as were those that expected to offer their own plan in the next two years.

- Some 52 percent of businesses without plans said they would start their own if asked to choose between doing so and enrolling workers in a state-sponsored auto-IRA. Meanwhile, just 13 percent of businesses with plans said they would drop current offerings to enroll workers in a state program.

- Many employers without plans expressed willingness to consider other government-promoted options, such as an online retirement plan marketplace or a multiple employer plan (MEP). Fifty-six percent said availability of a marketplace would make them more likely to offer a plan; 61 percent said they would consider participating in a MEP.

Endnotes

- Irena Dushi, Howard Iams, and Jules Lichtenstein, “Retirement Plan Coverage by Firm Size: An Update,” Social Security Bulletin 75, no. 2 (2015): 41–55, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2604116.

- Ruth Helman, Craig Copeland, Jack VanDerhei, “The 2015 Retirement Confidence Survey: Having a Retirement Savings Plan a Key Factor in Americans’ Retirement Confidence,” EBRI Issue Brief, no. 413 (April, 2015): 6, https://www.ebri.org/pdf/briefspdf/ebri_ib_413_apr15_rcs-2015.pdf.

America’s Overdose Crisis

Sign up for our five-email course explaining the overdose crisis in America, the state of treatment access, and ways to improve care

Sign up

ADDITIONAL RESOURCES

Fact Sheet

Article