Workplace Retirement Plans Tend to Sharpen Focus on Financial Futures

Survey looks at how availability of on-the-job savings opportunities relates to retirement security

Getty Images

Overview

For many, retirement security in the United States is uncertain. Experts recommend that Americans have multiple sources of retirement income—including Social Security, personal savings, and employer-sponsored savings plans—to ensure financial health after their working years. However, more than one-third of all private sector workers lack access to a workplace plan. Moreover, 31 percent of those whose employers offer retirement benefits do not participate. Some may decide they are unable to afford regular contributions, while others may be ineligible because of plan rules, such as requirements for a minimum number of hours worked each year.

But are those without access to an employer-sponsored plan and those who do not participate in available plans preparing for retirement in other ways? Are they prioritizing retirement savings outside of the workplace? Answers to these questions are important as government policymakers consider steps to boost access to retirement plans. The value of getting people to save on the job and to think about how they will finance life after their working years seems clear. Earlier research, for example, indicates that planning is associated with higher levels of wealth at retirement.

This analysis of data from a nationally representative internet survey of private sector workers shows a correlation between access to and participation in workplace-based retirement savings programs and more planning and saving. The survey conducted in 2016 by The Pew Charitable Trusts included those between the ages of 18 and 64 who were not self-employed, agricultural workers, or in the armed forces.

Among the key findings:

- Few workers have tried in the past two years to figure out how much income they would need in retirement.

- Those who are participating or have ever participated in an employer-sponsored plan are more likely than those who have never participated—regardless of current access—to have done any planning.

- How workers get planning information suggests that those who have participated in employer-sponsored plans have access to better planning resources.

- Most workers said they get planning guidance from online tools and calculators, while few get it from automated statements or benefits experts through their human resources department.

- Guesstimating—informal or “back of the envelope” calculations—is common, but more so for workers without access to a workplace plan (43 percent) than those with access (31 percent).

- Workers currently without access to a plan could still have other retirement savings, such as an individual retirement account (IRA) or a plan from a previous employer. However, just 27 percent of those without access to a plan said they have any retirement savings.

- Of those currently without access to a workplace plan but who have any retirement savings, 41 percent have not contributed to that savings in the past two years.

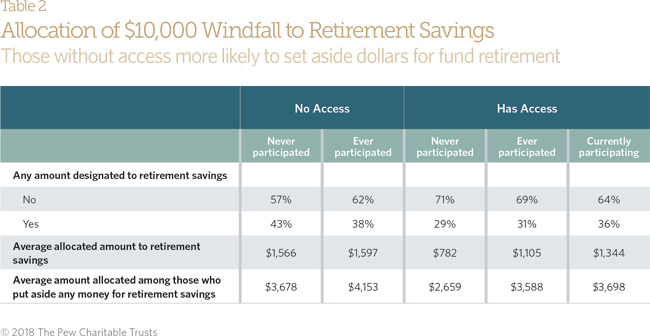

- Asking how workers would use a hypothetical $10,000 windfall can help reveal savings and spending priorities. On average, those without access to a retirement plan would allocate $1,580 toward retirement, more than those with access to a plan who are not currently participating, possibly because they cannot save at work.

- Workers are more likely to use the hypothetical money to pay down debt or build liquid savings than to boost retirement savings, which suggests that these factors may be more pressing concerns for many workers.

Who plans for retirement?

Understanding how much money will be needed in retirement to maintain a pre-retirement lifestyle provides guidance for how much to save and when to retire. Moreover, how Americans get information about retirement savings shapes how—and whether—they save and when they plan to retire. Although 56 percent of respondents in a separate 2015 survey said they worry about running out of money before they die, only 39 percent have tried to figure out their retirement needs.1

Research from 2016 shows that more than half (54 percent) plan to work past age 65 or not retire at all, either out of necessity or because of the satisfaction that work brings to their lives.2 Still, Americans generally underestimate how much they will need in retirement and overestimate how long they are likely to work.3 One- fifth of workers are overconfident. They are typically higher income workers with defined contribution plans who overestimate how much retirement income their contributions will generate. More than one-third of those working at 58 retire before they plan to because of failing health or job layoffs, neither of which can be predicted.4

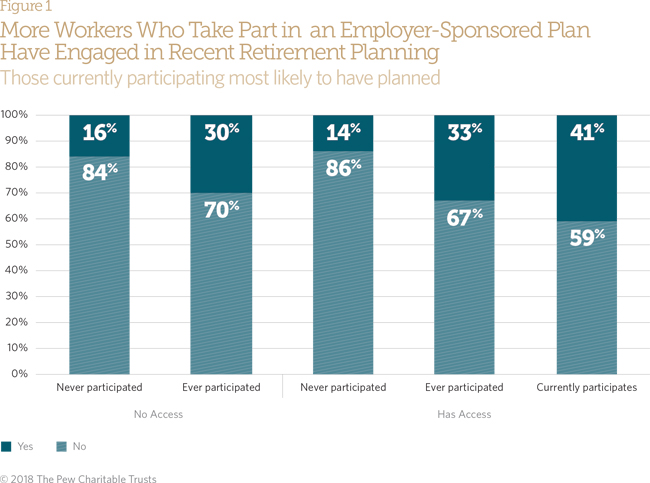

Pew’s research shows a clear connection between planning and retirement plan access and participation. Overall, workers with access to a plan were much more likely to report that they had tried to figure out in the previous two years how much retirement income they would need.

Past participation in a workplace savings program also is associated with a greater likelihood of retirement planning: among workers who do not currently participate, 30 percent of those who do not have access and 33 percent of those with access but who do not participate report planning for retirement. That’s about twice as high as those who never participated, regardless of access. In contrast, 41 percent of those with access and currently participating said they have planned in the past two years.

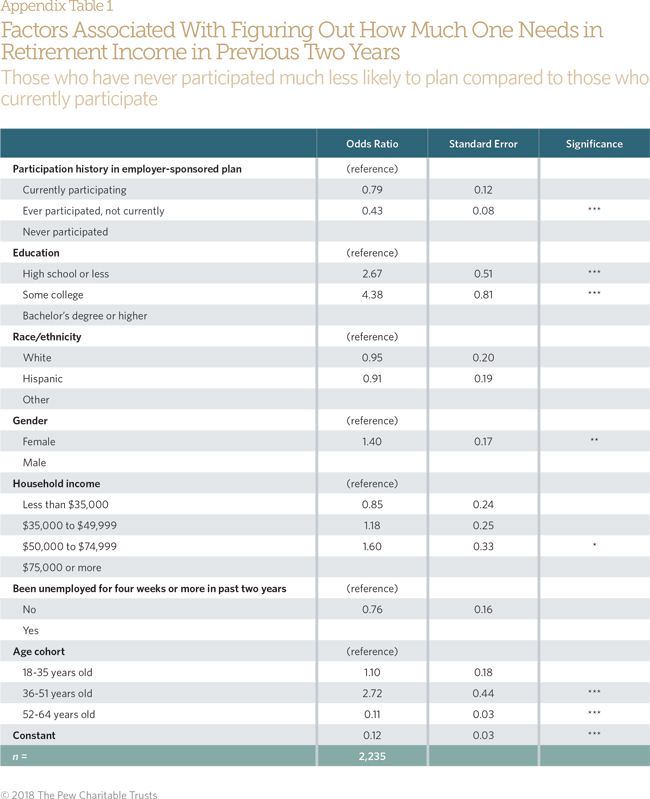

Even when accounting for other worker characteristics, such as education, race/ethnicity, gender, household income, unemployment history, and age, those who have never participated in employer-sponsored retirement plans are much less likely to plan for retirement than those who have participated or are currently participating. (See Appendix Table 1 for full regression results). Participation may make workers more cognizant of the need to plan or give them more resources, such as employer-provided tools or seminars. It is also possible that those who have planned are more likely to know they should build retirement savings by participating in available opportunities, a notion supported by earlier research.5

Demographic groups differ in their rates of planning. For example, men are 42 percent more likely than women to report having planned in the past two years, a troubling finding because women typically live longer than men. Among all workers, those with some college and those with at least a bachelor’s degree are 2.6 times and 4.3 times, respectively, more likely than those with a high school diploma or less education to plan. Among the reasons that education appears to be related to planning may be the larger salaries on average among those with college degrees, a group that also tends to have higher rates of financial literacy.

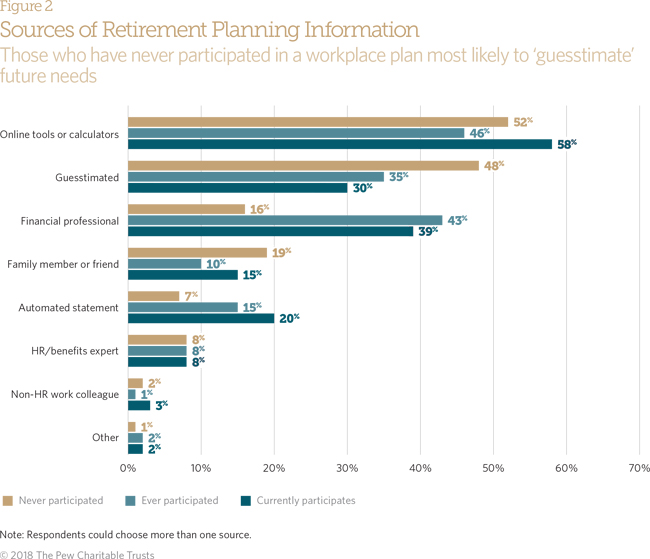

Survey respondents who had planned in the past two years were asked how they did so. Roughly half said they used online tools or had guesstimated their long-term needs; few had spoken with a human resources manager or benefits expert, friends, or family.

A history of plan participation appears to play a role in the resources used. For example, those workers who have never taken part in an employer-sponsored plan are significantly less likely than those who currently do or have done so in the past to say they have used a financial professional or automated statements from financial providers. They also are much more likely to “guesstimate,” or make informal calculations. Moreover, 28 percent of those who have never participated in an employer-sponsored plan have only guesstimated, compared to 14 percent of workers who have ever taken part and 8 percent of those who currently participate. Workers who have participated in a workplace plan use more rigorous tools to determine retirement income needs. These formal tools can be a reality check for workers who may be overconfident in their savings, thus prodding them to better prepare for retirement.

Who has retirement savings or is making contributions?

Workers without access to an employer-sponsored plan have other options to save for retirement, such as an IRA or a 401(k) from a previous employer. Some employees may view these “other” retirement savings as a substitute for a workplace plan at their current job. On the other hand, experience with retirement saving could encourage them to seek jobs with these benefits. Pew’s survey explored these possibilities by asking respondents whether they had any current retirement savings separately from questions about employer-sponsored plans.

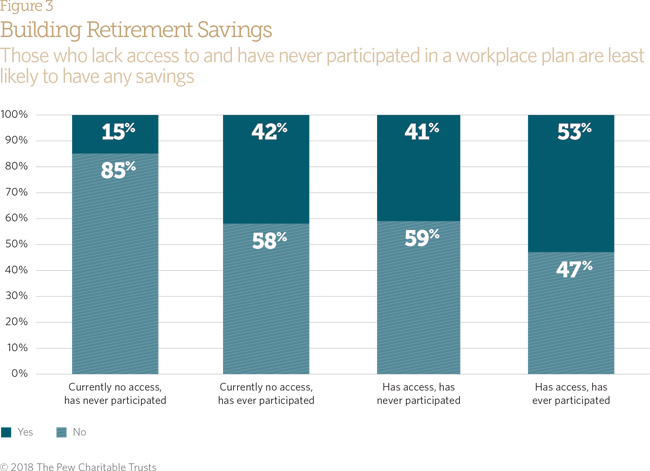

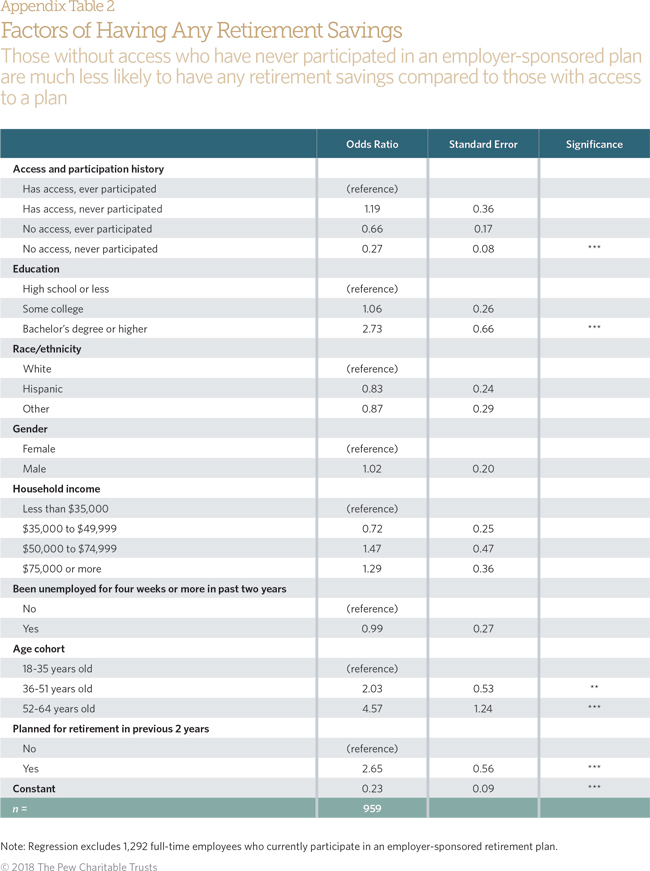

Just 15 percent of those without access to a plan and who have never participated have retirement savings, suggesting that these workers will be unprepared for retirement. Those currently without access to a plan but who have participated in the past are about as likely to have savings as those with access who have never participated. Even when accounting for worker characteristics, those who do not have access and have never participated in an employer plan are more than 70 percent less likely than those who have access and have ever participated to have any retirement savings. (See Appendix Table 2 for full regression results.) Some of those who have the opportunity but do not currently

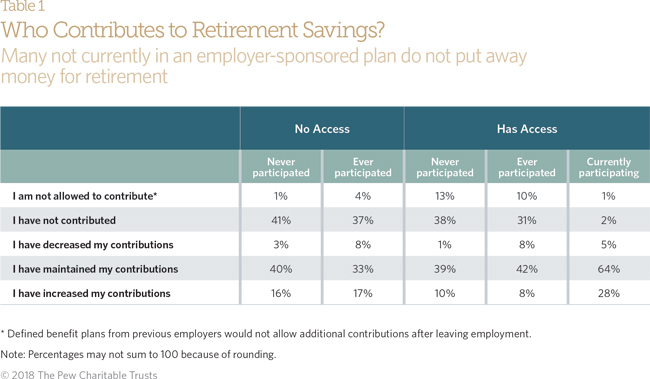

Having any retirement savings does not mean that respondents actively contribute to such a plan. For example, a person might have contributed money or rolled over a prior retirement account to an IRA but is not currently making contributions. When asked, 38 percent of workers who have any savings but do not have access to an employer-sponsored plan said that they had not contributed in the past two years; 3 percent said they were not allowed to contribute. Any available savings is better than nothing, but a dormant plan may offer little in terms of available dollars, especially for younger workers who have had little time to build savings. When comparing access and participation histories, these patterns differ slightly. Among those currently participating in employer- sponsored plans, only 8 percent did not contribute or had decreased their contributions, compared with 45 to 52 percent of all others regardless of current access or participation history. Those who do not participate in an employer-sponsored plan—regardless of access—are not significantly different from one another in these contribution patterns.

Saving versus spending?

Retirement savings behavior can vary because of differing financial priorities (e.g., focusing on paying down debt or saving for a down payment on a house or car). The survey sought to assess the tradeoff between spending and saving by asking respondents what they would do if they were given $10,000. They were told to distribute the money across nine categories, including a retirement account. This hypothetical situation shows how respondents might allocate an unexpected lump sum windfall, as opposed to a pay raise, and provides insight into financial priorities.

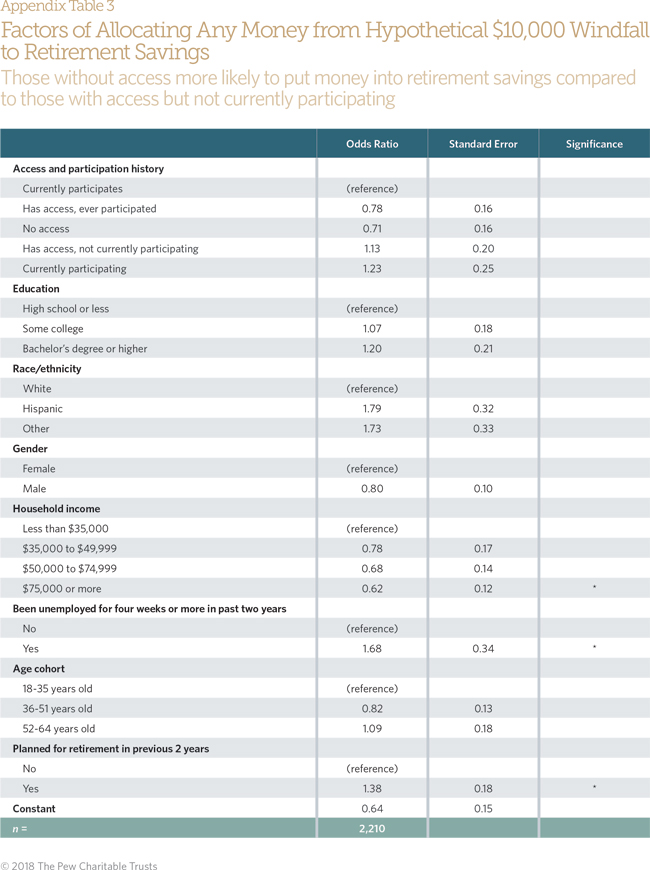

Overall, only 36 percent said they would put some amount into retirement savings, suggesting that for most workers, retirement savings is not a priority. But the numbers differ, depending on access to an employer-sponsored plan: 38 to 43 percent of those currently without access to a plan said they would allocate money to retirement savings, compared with 29 to 31 percent of those currently with access, but who do not participate. Those without access on average said they would allocate more than $1,500—about twice as much as those with access who never participated in a plan. This may be because those with an opportunity to save—but who choose not to—may place less of a priority on putting away money for retirement.

The various groups are more similar when examining average amounts among those who designated any money to retirement savings, though again those with access but who had never participated said they would make much lower allocations ($2,659) than the others. Those without access may be more likely to designate a larger share to retirement compared to those currently participating because they may feel a need to catch up.

Surprisingly, however, those with access but who do not participate are less likely to designate any money than others. Even when controlling for other factors, such as household income, age, and unemployment history, those with access but not currently participating are 37 percent less likely to designate anything to retirement savings than are those who do not have access. This suggests that those who do not participate in available plans are overall less interested in contributing.

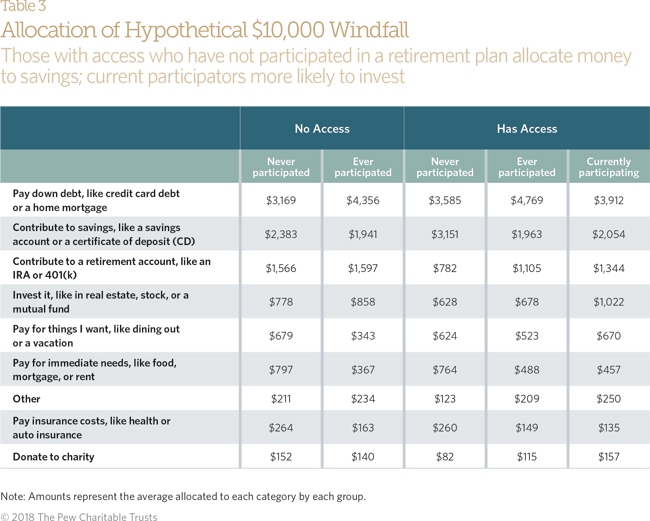

Looking at how all workers would designate money to other options, paying down debt proved the most popular category, based on average dollar amount ($3,169-$4,769). That varies somewhat by access and participation history: those who have participated in employer-sponsored plans said they put more money toward paying down debt on average, which may reflect different types of debt. For example, those able to participate in workplace plans may be more financially comfortable and have more secure debt, such as mortgages. Workers taking part in a plan also could be more likely to take on less secure debt, such as credit card balances. Those who currently participate in a plan are more likely to say they would invest a portion of the money ($1,022), while those with access who have never participated are much more likely to allocate money to liquid savings ($3,151). Workers who have never participated—regardless of access—are almost twice as likely to allocate money to immediate needs and to insurance, an indication that other financial pressures may be preventing them from saving for retirement.

Conclusion

As government policymakers seek ways to ensure that more people are financially secure in retirement, understanding what workers actually do and would like to do regarding retirement savings is essential. Proposed policies—such as IRAs into which new workers are automatically enrolled, multiple employer programs, and online marketplace exchanges—focus on boosting retirement security through employers.6 Though employees have opportunities to save on their own, these findings suggest most are unlikely to do so.

First, the results show that participation in an employer-sponsored retirement plan is associated with behaviors likely to boost retirement preparedness, such as trying to figure out how much income will be needed and contributing to savings regularly. One factor may be access to plan features, such as retirement calculators, that make clear how much saving may be needed. Still, workers who are more likely to participate may also be those who plan for retirement with little external encouragement. Moreover, few workers without access to workplace plans have any savings. Increasing access to and, more importantly, participation in employer-sponsored plans or programs through the workplace would help employees build savings.

Second, responses to the question about allocating a $10,000 windfall indicate that for many workers, paying down debt, liquid savings, and meeting immediate needs take a higher priority than retirement savings. Policy solutions could recognize those competing financial interests by exploring options such as so-called sidecar programs that allow workers to save for short-term needs along with saving for retirement.

Policymakers concerned with boosting retirement savings must consider how workers currently without access to workplace plans prepare for their post-employment years. Policies that encourage greater access to and participation in employer-based plans appear to be a critical pathway to retirement security.

Methodology

To study retirement savings behaviors and attitudes, The Pew Charitable Trusts surveyed 2,918 Americans aged 18 to 64 who are employed and not working for the government, using GfK’s probability based internet panel, KnowledgePanel. The survey was released to a random sample of 15,872 panel members Aug. 2-23, 2016, in English and Spanish. Data are weighted to be nationally representative using several benchmarks (i.e., gender, race/ethnicity, education, census region, household income, language proficiency, and employment status).

Analyses use listwise deletion. The sample focused on in this paper are full-time workers (n = 2,441).

Technical Appendix

The authors used logistic regression to examine whether respondents have tried to figure out how much retirement income they will need (Appendix Table 1), whether the respondent has any retirement savings (Appendix Table 2), and whether the respondent allocated any money from a hypothetical $10,000 windfall (Appendix Table 3). The models aimed to include only variables that were theoretically related to the dependent variable; generally, models included educational attainment, household income, race/ethnicity (in which black, Asian, multiracial, and other races are collapsed into one category due to low cell sizes), gender, has been unemployed for at least four weeks in the past two years, and age cohort (meant to parallel generational cohorts). In Appendix Tables 2 and 3, whether the respondent planned for retirement in the past two years was additionally used as an independent variable. The study used listwise deletion to handle missing data for univariate and bivariate analyses. Statistical significance indicated by * p < 0.05 ** p < 0.01 *** p < 0.001.

Endnotes

- Financial Industry Regulatory Authority, “Financial Capability in the United States 2016” (2016), http://www.usfinancialcapability.org/downloads/NFCS_2015_Report_Natl_Findings.pdf.

- Transamerica Center for Retirement Studies, “Perspectives on Retirement: Baby Boomers, Generation X, and Millennials, 17th Annual Transamerica Retirement Survey of Workers” (2016), http://www.transamericacenter.org/docs/default-source/retirement-survey-of-workers/tcrs2016_sr_perspectives_on_retirement_baby_boomers_genx_millennials.pdf.

- Courtney L. Vien, “More Than Half of Clients Underestimate Their Retirement Expenses,” Journal of Accountancy (2015): http://www.journalofaccountancy.com/news/2015/nov/underestimate-retirement-expenses-201513318.html#sthash.4u6eoc5z.dpuf.

- Alicia H. Munnell, Geoffrey T. Sanzenbacher, and Matthew S. Rutledge, “What Causes Workers to Retire Before They Plan?” (2015), Center for Retirement Research Working Paper No. 2015-22, http://crr.bc.edu/wp-content/uploads/2015/09/wp_2015-22.pdf.

- Annamaria Lusardi and Olivia S. Mitchell, “Baby Boomer Retirement Security: The Roles of Planning, Financial Literacy, and Housing Wealth,” Journal of Monetary Economics 54, no. 1 (2007): 205–224, 10.3386/w12585.

- The Pew Charitable Trusts, “How States Are Working to Address the Retirement Savings Challenge” (July 2016) http://www.pewtrusts.org/en/research-and-analysis/fact-sheets/2016/07/how-states-are-working-to-address-the-retirement-savings-challenge-three-approaches.