Financial Shocks Put Retirement Security at Risk

Smart policies can help meet immediate needs without depleting long-term savings

Overview

Because most households have relatively fixed and expected expenses each month, a single financial shock— such as a major car repair or a sudden loss of income—can make meeting those obligations more difficult. When Americans experience these unexpected expenses, most look to multiple sources of money.

Household savings are designed for such emergencies but are often insufficient to completely cushion an income loss or the cost of unexpected repairs on a home or vehicle. A 2015 report by The Pew Charitable Trusts gives a sense of how Americans say they would respond to a hypothetical scenario involving a financial emergency: Some 78 percent said they would use their savings and checking accounts, and 49 percent would turn to credit cards. About a quarter, though, would look to defined contribution retirement accounts, such as a 401(k), a 403(b), or an individual retirement account (IRA).

The availability of early withdrawals from certain retirement accounts such as Roth IRAs or in permitted situations like financial hardship creates a dilemma for policymakers and plan sponsors. The primary goal of tax-sheltered retirement savings is to increase the savings available for people when they leave the workforce. Taking out money early reduces the savings available at retirement as well as retirement income from these savings. For example, workers who take loans against their 401(k) accounts forgo any investment earnings on the borrowed amount for the length of the loan. Those who make withdrawals—known as distributions—from defined contribution accounts or IRAs before age 59½ not only pay taxes on the money but often also pay a 10 percent early withdrawal penalty.1 In addition, following a hardship withdrawal from a defined contribution plan, employees are often prohibited from contributing to the plan for at least six months. That typically results in permanently lower retirement account balances because it is so hard to catch up.

On the other hand, allowing people to withdraw funds early under limited conditions helps them manage financial shocks. In fact, such early withdrawals can in some cases prevent cascading economic problems, for example, by allowing people to keep a car in working order or retain a house and home equity. In most instances, the cost of borrowing could be cheaper via a 401(k) loan than through an auto title loan, a rent-to-own loan to replace an appliance, or a personal loan. Early withdrawals also could help boost earnings or wealth for retirement by helping to pay for more education or a home purchase. Maintaining access to such funds is critical for those who might not contribute to their retirement plans at all if they could not access any of the savings until they retire.2

To examine the impact of financial shocks on retirement security, Pew analyzed data from its Survey of American Family Finances, a nationally representative survey with a sample size of more than 5,661 households conducted in two waves, in late 2014 and late 2015. Participants were asked about financial shocks that occurred in the 12 months before the survey, about retirement account withdrawals in the same time period, and about their current financial situations. This brief focuses on survey respondents ages 20-58 who were not retired and did not have a retired spouse.

This brief documents the relationship between financial shocks and loans or early withdrawals from retirement plans. Among the major findings:

- About 13 percent of people with retirement accounts said they had drawn on these savings in the previous year and had experienced a financial shock in the same period; only 2 percent with an account made a withdrawal but reported no shock.

- As the number of financial shocks experienced increased, so did the likelihood that a household had drawn on its retirement account.

- The median cost of the most expensive financial shock was $2,000 among households experiencing a shock. One-quarter of survey respondents had unexpected expenses of $700 or less, although another quarter faced expenses of $6,000 or more and 10 percent experienced a shock that cost at least $15,000.

- People with lower annual incomes were more likely than higher-income individuals or households to withdraw money from retirement accounts.

- As the cost of the shock rose relative to monthly income, so did the likelihood that an individual would draw on retirement account savings.

- Households were more likely to have withdrawn from their retirement accounts during years in which they experienced spells of unemployment, a pay cut, or a marital change such as divorce, separation, or the death of a spouse.

- People with lower levels of education were more likely to draw from their retirement accounts in response to a financial shock than were those with a college education or more. Among the factors contributing to this could be that those with more schooling tend to have higher incomes, more savings, greater access to affordable credit, and more opportunities to build financial know-how.

- African-Americans were more likely than whites to turn to retirement accounts to respond to financial shocks. African-Americans have lower wealth on average than whites, which means many have smaller cushions against financial shocks.

More than half of households experience at least one annual financial shock

Pew defines financial shocks as large unplanned expenses, such as a major home or car repair, or income lost to unemployment, a pay cut, illness, injury, or death.3 In most cases, families have not budgeted for such expenses or income losses, but these incidents are not rare. According to the survey, 56 percent of workers ages 20-58 lived in a household that experienced a financial shock in the previous year.

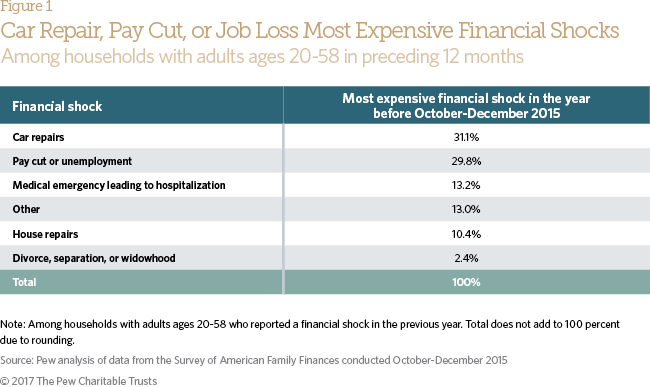

Among households reporting one or more financial shocks, most said that their most expensive were either car repairs or income losses from a pay cut or unemployment. (See Figure 1.) Smaller numbers reported that their most expensive financial shocks were caused by house repairs, medical emergencies leading to hospitalization, or a change in marital status such as separation, divorce, or the death of a spouse.4 “Other” shocks were attributed to a variety of causes, including funeral expenses, veterinary bills, moving expenses, or unexpected costs associated with running a small business.

The median cost of the most expensive financial shock was $2,000 in households with adults ages 20-58 experiencing a shock. One-quarter of survey respondents had unexpected expenses of $700 or less, although another quarter faced expenses of $6,000 or more and 10 percent experienced a shock that cost at least $15,000.

Drawing on retirement savings

The cash and savings that households have on hand are intended to help in emergencies such as car repairs or medical expenses, but they are often not large enough to weather a serious financial shock. Pew’s 2015 analysis of data from the Survey of American Family Finances found that 41 percent of surveyed households did not have enough liquid savings to cover the $2,000 cost of the median “most expensive financial shock.”5 Pew also asked about several other sources of emergency funding, including “retirement accounts, such as 401(k)s or IRAs.” In the analyses that follow, the figures refer to respondents ages 20-58 who owned retirement accounts and also experienced financial shocks in the year leading up to Pew’s survey from October to December 2015.

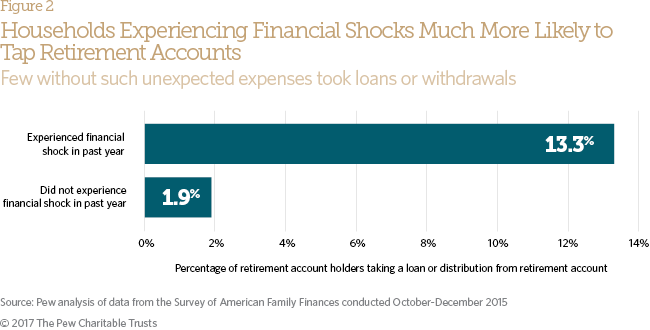

Just 15 percent of retirement account holders reported that they or somebody in their household took a loan or distribution6 from a retirement account during the previous year, though nearly 90 percent of those who drew from their retirement savings—13 percent of all retirement savings account holders—had experienced a financial shock in the same time period.7 (See Figure 2.) By comparison, only 2 percent of account holders withdrew cash from their retirement accounts but reported no shock during the same period.8 As the number of financial shocks experienced increased, so did the likelihood that a household had drawn on its retirement account. About 9 percent of households that experienced a single financial shock used retirement accounts, compared with 11 percent of households that experienced two financial shocks and 30 percent of those that experienced three or more financial shocks during the previous 12 months.9

Although causation cannot be determined, the financial shock may have been the direct cause of retirement account withdrawals—or, perhaps, was an indirect cause as people used retirement savings to pay back loans from credit cards, relatives, or other sources. The latter, or indirect, causation may be more likely because retirement savings accounts are often less liquid than other financial resources.

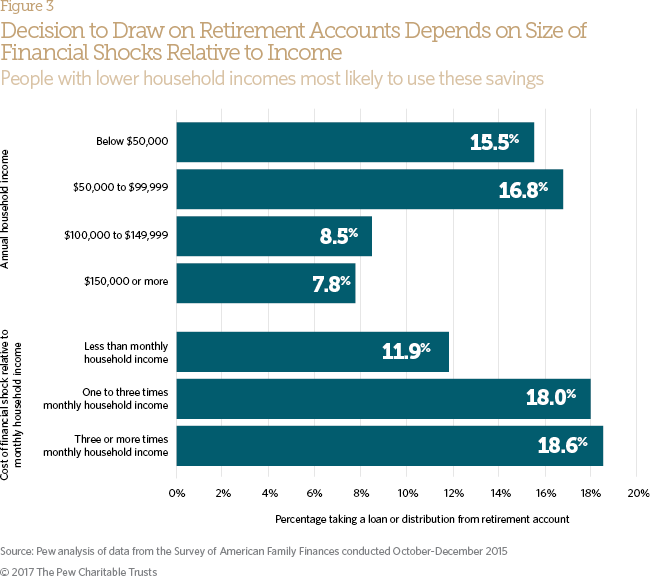

People with lower annual incomes were more likely to withdraw money from their retirement accounts, as a loan, a withdrawal while still employed, or a distribution, than were higher-income individuals or households. About 16 percent of those with an annual income under $50,000 used their retirement accounts during a year in which they experienced a financial shock, compared with 8 percent of those with an annual income of $150,000 or more.10 For some lower-income households, an income shock such as unemployment or a pay cut may help explain their income status at the time of the survey.

The actual dollar cost of the financial shock, by itself, was not a significant factor in whether a household turned to its retirement account. Not surprisingly, the likelihood increased when the cost represented a greater share of monthly income. (See Figure 3.) In cases where the cost was less than or equal to reported monthly household income, about 12 percent of retirement account owners who experienced a financial shock drew from their accounts that year. That figure jumped to 18 to 19 percent when the financial shock exceeded monthly income.11

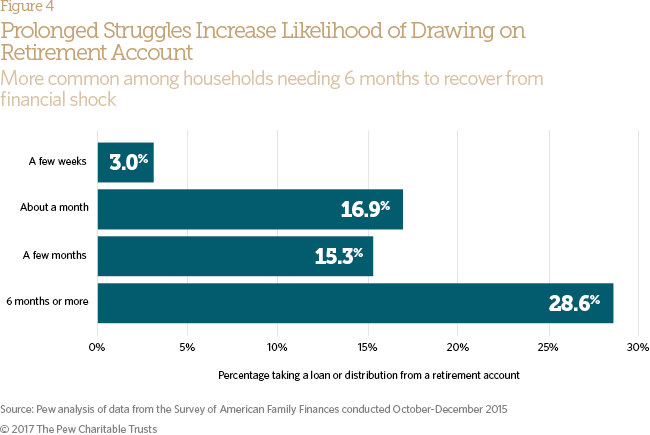

Many households struggled to make ends meet after their most expensive financial shocks, including a third of high-income households. Of those who had recovered from a financial shock by the time of the survey, the average respondents reported that it took “a few months” before they could make ends meet again. Some 14 percent said recovery took at least six months.12

Struggling for a longer period to make ends meet then increased the likelihood that a household with a retirement account would take a distribution or loan. (See Figure 4.) Among survey respondents who had recovered from a financial shock in the previous year, 29 percent who said that the impact of the shock lasted at least six months drew on their retirement accounts. By contrast, only 3 percent of respondents who were able to make ends meet within a few weeks said they turned to their retirement accounts.13

The likelihood that households would use their retirement accounts increased during years in which they experienced an income loss, such as unemployment or a pay cut. About 25 percent of those who had experienced such a loss turned to their retirement accounts.14 Many of those who had lost jobs were out of work for months. According to federal statistics, the average length of unemployment for full-time workers in 2014 was four months.15

Job losses can have other consequences as well. For example, employers may require employees who leave work to move retirement accounts with small balances, which can lead to a distribution of savings if the money is not rolled into a new tax-protected account. Some separated workers may not understand the tax consequences of holding on to a distribution, while others may decide they need the money regardless. A loan from a retirement account that is outstanding at separation becomes a distribution—with tax consequences—if not paid in full.

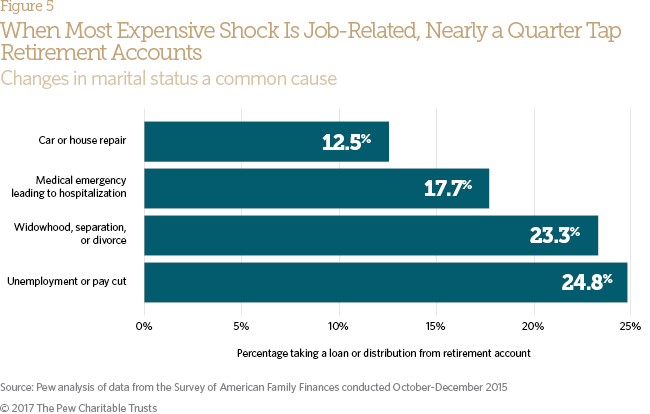

While only 2 percent of respondents cited marital change as their largest expense in the previous year (see Figure 1), the costs of these changes can be high. Some 23 percent of respondents who said marital change was their most expensive shock turned to their retirement account. (See Figure 5.) The death of a spouse can mean lost income. A separation or divorce often brings the costs of setting up a second household as well as substantial attorneys’ fees. Among all respondents who reported a change in marital status in the year before the survey, the median financial cost resulting from that change was $4,500, which was greater than the median cost experienced by those who had a medical emergency ($2,000) or who saw their income drop because of a pay cut, reduced hours, or unemployment ($2,000). Other researchers have also found that income loss and changes in marital status are important causes of retirement account withdrawals.16

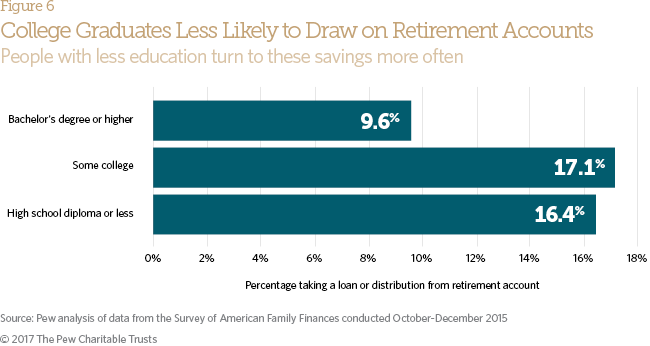

The level of education also can be an indicator of whether people turn to these savings in response to a financial shock. More years of schooling significantly reduces the likelihood of drawing on a retirement account in these circumstances. (See Figure 6.) A college degree or more education can mean increased financial literacy and the mathematical skills that are helpful in retirement planning.17 This level of schooling also can translate into higher incomes,18 more savings and wealth, and better access to affordable credit. Those factors all make it easier for those with college degrees to deal with unexpected expenses. Just under 10 percent of those with a college degree and a retirement account tapped those accounts in the year following a financial emergency, compared with 16 or 17 percent of those with a high school diploma or less education, or with some college, respectively.19

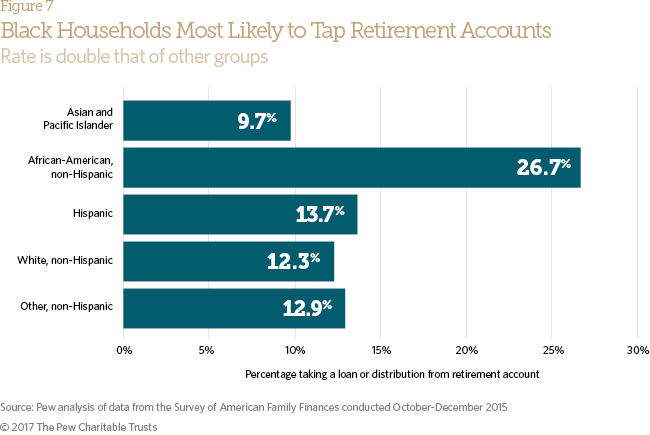

African-Americans were much more likely, and Hispanics were somewhat more likely, to turn to their retirement accounts during a financial shock than were Asian-Americans or non-Hispanic whites. (See Figure 7.) About 27 percent of African-Americans and 14 percent of Hispanics who had retirement accounts drew on these accounts during a financial shock. By comparison, about 12 percent of whites and 10 percent of Asian-Americans and Pacific Islanders drew on their accounts during a financial shock.20

In general, households with lower incomes, and members of certain minority groups, often have more precarious financial pictures and fewer resources to cushion against financial adversity. The typical white household has a little more than one month’s income in liquid savings, compared with 12 days for the typical Hispanic household and just five days for the typical African-American household.21 Whites and households with more education and greater income also typically have better access to affordable credit.22 Those who draw on their retirement accounts at higher rates in the event of financial shocks do so because they have few other options. The finding that lower-income households and minorities are more likely to have accessed their retirement accounts also may help explain persistent gaps in retirement account balances by income and race.23

Conclusion

Retirement savings are a critical part of a family’s broader financial picture. Many working families face financial shocks at one point or another and may draw on their retirement savings accounts if other savings are insufficient. Lower-income households and minorities are more likely than other groups to draw on their retirement savings when facing financial adversity.

To preserve retirement savings for retirement income security, policymakers and the financial sector could consider how to establish additional financial buffers that encourage short-term savings in addition to retirement savings. Given that new tools like automatic enrollment in retirement savings programs have greatly boosted participation, it may be possible to look at using payroll systems to help Americans improve their rainy day savings and allow them to keep more of what they save for retirement. For example, policymakers are in the early stages of looking at ways to allow workers to save for financial shocks, as well as for their retirements, through payroll deductions, possibly in a bank account or Roth IRA. These “sidecar” accounts could provide workers with flexibility to manage emergencies and help prevent the need to draw from retirement accounts.

Methodology

The data reported here were collected in waves 1 and 2 of Pew’s Survey of American Family Finances, conducted by The Pew Charitable Trusts, with most statistical analyses drawn from wave 2. The survey was administered to a nationally representative panel between Nov. 6 and Dec. 3, 2014. The second iteration was administered to the same panel between Oct. 27 and Dec. 1, 2015. Including only respondents who answered both years and oversamples of black and Hispanic respondents, the total sample size was 5,661. Survey firm GfK collected the data on behalf of Pew and administered the computer-based questionnaire in English and Spanish. All reported data were weighted. For clarity of analysis, respondents who chose not to answer a question were excluded from the statistics generated for that item. Overall, item nonresponse was 2.2 percent for the 2014 survey and 1.5 percent for the 2015 survey. Additional details about the survey and its methodology are available at pewtrusts.org/Survey-of-American-Family-Finances-Methodology.

The analysis focuses on respondents ages 20-58. Members of this age group are still in their working years and have not reached the age at which retirement account holders may make penalty-free withdrawals (59½). Respondents who reported that they or their spouse or partner were retired were dropped from the sample in order to focus the analysis on retirement account withdrawals that were not related to retirement itself. Retirement account ownership was measured in wave 1 to capture all owners, including those who cashed out their accounts or took a lump sum distribution upon separating from a job by wave 2. Because of data limitations, regressions were not included in the analysis.

Endnotes

- Robert Argento, Victoria L. Bryant, and John Sabelhaus, “Early Withdrawals From Retirement Accounts During the Great Recession” (November 2013): 1–16, table 2, https://www.irs.gov/pub/irs-soi/14rpearlywithdrawalretirement.pdf.

- Alicia H. Munnell, Annika Sunden, and Catherine Taylor, “What Determines 401(k) Participation and Contributions?” Center for Retirement Research at Boston College (December 2000). See also Overture Financial, “Final Report to the California Secure Choice Retirement Savings Investment Board” (March 2016), http://www.treasurer.ca.gov/scib/report.pdf.

- See The Pew Charitable Trusts, “How Do Families Cope With Financial Shocks?” (October 2015), for a discussion of some of the survey questions designed to understand the types of financial shocks Americans encounter most frequently and how families addressed these shocks.

- The Federal Reserve Board’s Survey of Household Economics and Decisionmaking (SHED), using slightly different categories of economic hardship, finds a higher reported incidence of financial disruption over the year prior to the survey. For example, the SHED reports that 36 percent of families experienced a “health emergency,” while Pew’s Survey of American Family Finances, used in this report, found that 13 percent of households experienced a “medical emergency leading to hospitalization.” See Board of Governors of the Federal Reserve System, “Report on the Economic Well-Being of U.S. Households in 2015” (May 2016).

- The Pew Charitable Trusts, “What Resources Do Families Have for Financial Emergencies?” (November 2015), 4, http://www.pewtrusts.org/~/media/assets/2015/11/ emergencysavingsreportnov2015.pdf.

- The survey questions did not differentiate between distributions and loans from retirement accounts. Employer-sponsored retirement plans such as 401(k), 403(b), and 457(b) plans may, but are not required to, provide for hardship distributions. Plan sponsors determine the criteria for a hardship withdrawal, with plan rules often allowing for hardship withdrawals for unreimbursed medical expenses, death, higher education expenses, imminent foreclosure, purchase of a first home, or house repair expenses. Some employees who take distributions upon separating from an employer may roll the money over to an IRA, but the survey does not allow us to determine when this happens. Employees who left a company at which they had a 401(k) plan at age 55 or older may withdraw their 401(k) funds without penalty before age 59½, paying only income tax, so in order to preserve the focus on pre-retirees we dropped respondents who said that either they or a spouse was retired. Some defined contribution plans also allow workers to borrow from their accounts; however, if the loan is not paid back when a worker separates from the employer, it will be treated as a distribution. Withdrawals from traditional IRAs are subject to a 10 percent penalty, although some exceptions may apply for a first-home purchase, significant unreimbursed medical expenses, or postsecondary education. Post-tax contributions to Roth IRAs may be withdrawn at any age without penalty; earnings from the contributions may be withdrawn penalty-free after five years.

- Pew combined two survey variables to increase cell sizes and statistical significance. The first survey question asked whether respondents had “used a retirement savings account” to address a financial shock in the previous year. A second survey question asked whether “a person in the household took a loan, a distribution, or cashed out a retirement account, not including things that were legally required” in the previous year, and without reference to a financial shock. It is likely that at least some retirement account withdrawals during the year before the survey occurred prior to the financial shock and were not related to it. On the other hand, and perhaps more importantly, respondents may have underreported the downstream effects of the financial shock that ultimately led to retirement account withdrawals. For example, a household that paid for a financial shock using credit cards or by borrowing from relatives may have ultimately turned to a retirement account to pay back these loans. Pew’s results are lower than reported in income tax data. Other surveys, such as the Federal Reserve Board’s Survey of Consumer Finances, have also reported results that are lower than tax-based estimates; the reasons why are not immediately clear.

- Retirement account holders who used their retirement savings without having experienced a financial shock generally had lower household incomes than those who withdrew from their retirement accounts after a financial shock. The median income of those who drew from their retirement savings in the absence of a financial shock was $60,000, compared with a $69,000 median income among those who used their retirement accounts during the same period in which they experienced a financial shock. There were not enough observations to examine the educational or racial/ethnic characteristics of this group.

- Significant at p < 0.001.

- Significant at p = 0.027.

- Significant at p = 0.083.

- Figures refer to all respondents who had experienced a financial shock in the preceding 12 months and who had recovered from it by the time of the survey, whether or not they owned retirement accounts or used them during the period.

- Significant at p = 0.078.

- Significant at p = 0.071.

- Bureau of Labor Statistics, “Household Data Annual Averages: Unemployed Total and Full-Time Workers by Duration of Unemployment,” accessed Aug. 25, 2017, https://www.bls.gov/cps/aa2014/cpsaat30.pdf.

- See Argento, Bryant, and Sabelhaus, “Early Withdrawals From Retirement Accounts.”

- Annamaria Lusardi and Olivia S. Mitchell, “Financial Literacy and Planning: Implications for Retirement Wellbeing,” in Financial Literacy: Implications for Retirement Security and the Financial Marketplace (Oxford: Oxford University Press, 2011), 17–49.

- See Bureau of Labor Statistics, “Unemployment Rates and Earnings by Educational Attainment, 2016,” http://www.bls.gov/emp/ep_chart_001.htm; and Anthony P. Carnevale, Stephen J. Rose, and Ban Cheah, “The College Payoff: Education, Occupations, Lifetime Earnings,” Georgetown University Center on Education and the Workforce (2011), https://cew.georgetown.edu/cew-reports/the-college-payoff. Note that the differences in lifetime earnings may in part reflect the underlying capabilities and characteristics of those individuals obtaining additional formal education and cannot be wholly attributed to the degree itself.

- Significant at p = 0.026.

- Significant at p = 0.065

- The Pew Charitable Trusts, “What Resources Do Families Have,” 2. In this Pew report, liquid savings include cash, checking and savings accounts, and unused prepaid cards.

- The Pew Charitable Trusts, “Payday Lending in America: Who Borrows, Where They Borrow, and Why” (July 2012),http://www.pewtrusts.org/~/media/legacy/uploadedfiles/pcs_assets/ 2012/pewpaydaylendingreportpdf.pdf.

- Benjamin W. Veghte, Elliot Schreur, and Mikki Waid, “Social Security and the Racial Gap in Retirement Wealth,” National Academy of Social Insurance (December 2016), https://www.nasi.org/sites/default/files/research/SS_Brief_48.pdf.

America’s Overdose Crisis

Sign up for our five-email course explaining the overdose crisis in America, the state of treatment access, and ways to improve care

Sign up

ADDITIONAL RESOURCES

Article

Fact Sheet