Extended Family Support and Household Balance Sheets

Getting by with a little help from friends and relatives

Getty

GettyOver the course of a lifetime, the family provides a foundation for financial security. Children’s economic well-being is closely tied to their immediate families’ financial success, and as kids grow up and begin forming their own households, extended family—parents, grandparents, siblings, and others—and friends continue to play an important role in their financial lives. Family and friends can offer critical support in times of difficulty, provide money to those with the greatest needs,1 and act as investors, improving the next generation’s long-term economic mobility,2 but this element of household balance sheets and of the financial system broadly is largely hidden from public view and poorly understood.

This brief uses data from The Pew Charitable Trusts’ Survey of American Family Finances and the Panel Study of Income Dynamics to explore how family and friends—an extended network outside the immediate household—provide short-term financial support and long-term advantages for wealth building and economic mobility. The analysis reveals a duality of support. On the one hand, friends and relatives serve as a financial safety net for many households, pitching in during rough patches and filling in the gaps when households have budget shortfalls, but the financial needs of extended social networks can place burdens on some households, especially those in tenuous situations themselves. On the other hand, mobility-enhancing investments, such as assistance with tuition and down payments on homes, are more often available to and benefit those who already have existing financial advantages.3 Key findings include:

- Households across all income levels give and receive transfers, but the type of transfer, amount, and the burden it places on the giver vary substantially. Lower-income households are more likely to receive assistance from family and friends, while middle- and upper-income households are more likely to provide help. But low-income households typically received half the amount of money that upper-income households received.

- Households that are the most financially precarious are the most likely to receive transfers to help make ends meet. Households that in the past year experienced material hardship—missing a mortgage or rent payment, skipping or delaying paying a bill, not going to the doctor or filling a prescription when needed, overdrawing a bank account, having a credit card declined, or withdrawing money prematurely from retirement accounts—were notably five times more likely than those that did not to have received money from friends or family.

- Single mothers stand out for giving and receiving support within their social networks, but this may be a challenge for them. Half of single mothers gave to or received money from those outside their households in the past year. Three-quarters of those who gave or lent reported that doing so was burdensome.

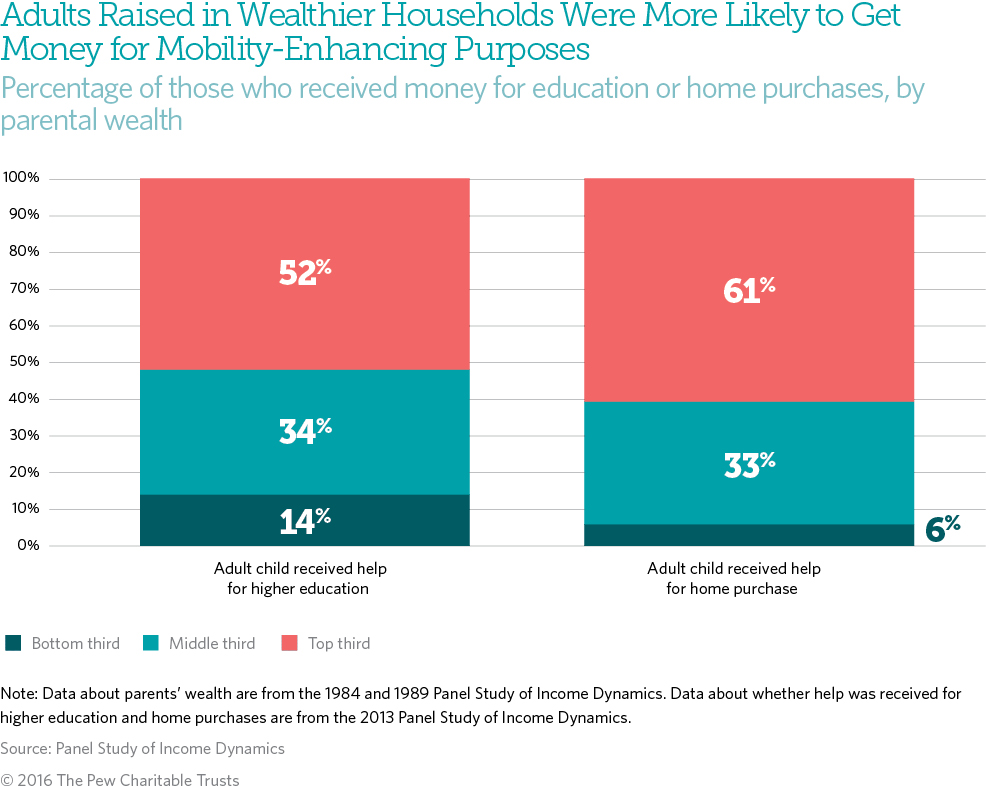

- Conversely, wealthy households are the most likely to receive transfers that boost their mobility or encourage even more wealth building. Among adults who received help for higher education or a home purchase, most were raised in the wealthiest households (52 percent and 61 percent of recipients, respectively) and had much healthier balance sheets. This suggests that family wealth advantages often convey to the next generation through mobility-enhancing transfers.

Households across all income levels give and receive transfers, but the type of transfer, amount, and the burden it places on the giver vary substantially

One-quarter (26 percent) of Americans reported providing financial assistance for day-to-day expenses to someone outside their immediate households in the previous year. In contrast, fewer (12 percent) reported receiving such help, likely due to the underreporting of transfers or some families receiving multiple transfers.4 The size of these gifts and loans was not trivial; the median dollar amount of assistance provided was $1,000 and that received was $560. Just 4 percent reported having both given and received money across household lines in the past year.5

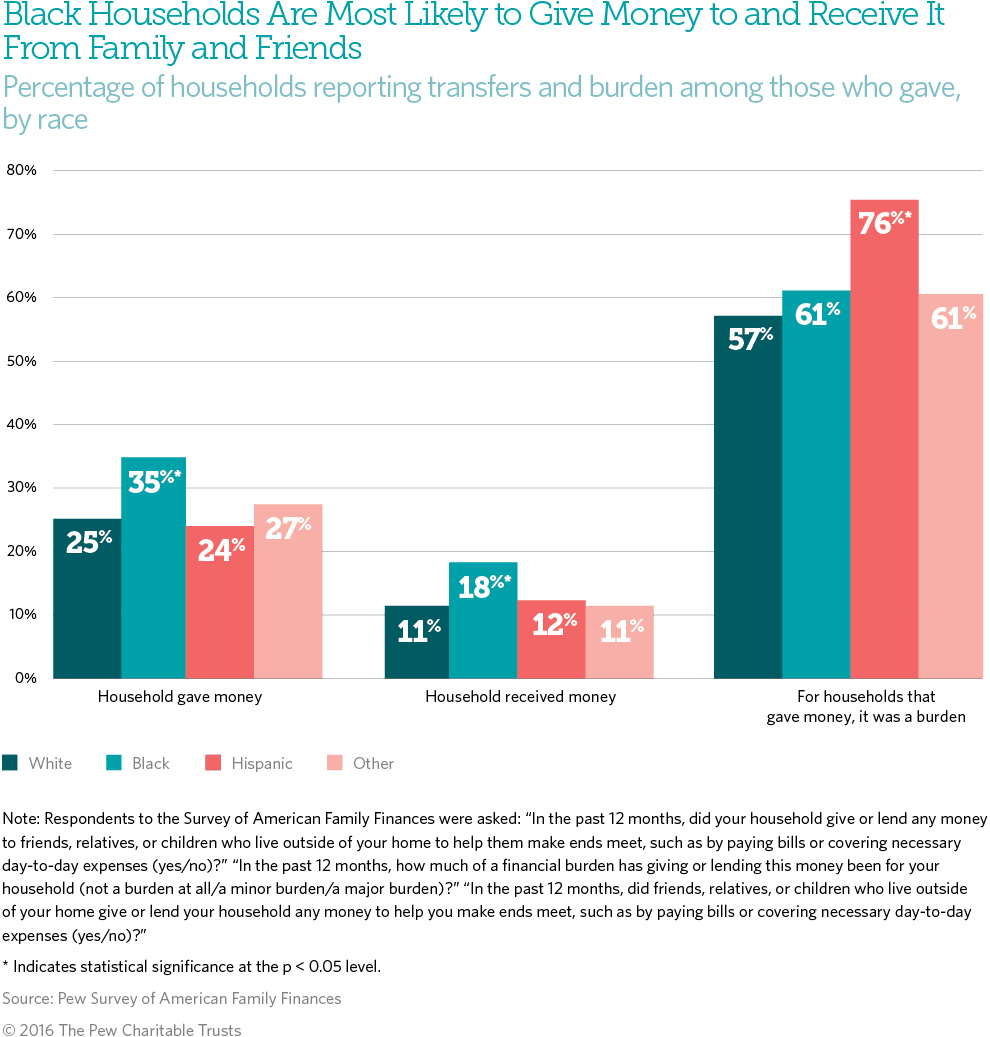

Black households were significantly more likely to provide assistance to those outside their immediate family (35 percent) than were white (25 percent), Hispanic (24 percent), or other households (27 percent).6 The frequency of transfers across black households is quite high: One-quarter reported giving money to a friend or relative more than once in the past year. Black households also report receiving help (18 percent) more than other households (11 percent).7 However, black households did not report the greatest burden with respect to giving or lending money. Rather, it was Hispanic households, among whom three-quarters of those who gave help felt burdened by doing so.8

Not surprisingly, low-income households are more likely to receive and less likely to provide such support. One in 5 households making less than $40,000 annually received money from friends and family in the past year, and of those, two-thirds got help on multiple occasions. But the amount that low-income households typically received ($500) was half that given to households making $85,000 a year or more ($1,000).

Households making over $40,000 a year were more likely than those making less than that annually to have given money to family or friends (28 percent versus 23 percent). Seven in 10 making less than $40,000 a year said giving money was a burden, while less than half making $85,000 a year or more said the same. (See Table A.1 on Page 12.)

Households that are the most financially precarious are the most likely to receive transfers to help make ends meet

The households that were most likely to have received money in the past year were also among the most financially fragile in other ways. While 12 percent of all households received money last year, this was reported more often by those with nonhousing net worth of less than $10,000 (23 percent), those headed by a single mother (28 percent), and those that experienced material hardship in the past 12 months (27 percent). (See Table A.1.) Four in 10 Americans who were unable to make their full rent payments or had credit cards declined also received money from friends or relatives in the past year.9 Transfers of money across household lines are an important and immediate form of help when families encounter difficult financial times.

In fact, having experienced a material hardship in the past year—for example, missing a mortgage or rent payment, skipping paying a bill or paying one late, not going to the doctor or filling a prescription when needed, overdrawing a bank account, having a credit card declined, or withdrawing money prematurely from retirement accounts—was the most important factor associated with households receiving money, more so than race, age, employment status, education, presence of kids, homeownership, being a single mother, income, or having less than $1,000 in liquid savings.10 Such households were five times more likely to have received money from friends or family. Considering that financially precarious households are often embedded together within the same networks, they likely received money from others who were also struggling to make ends meet.11

In fact, having experienced a material hardship in the past year—for example, missing a mortgage or rent payment, skipping paying a bill or paying one late, not going to the doctor or filling a prescription when needed, overdrawing a bank account, having a credit card declined, or withdrawing money prematurely from retirement accounts—was the most important factor associated with households receiving money. ...

Single mothers stand out for giving and receiving support within their social networks, but this may be a challenge for them

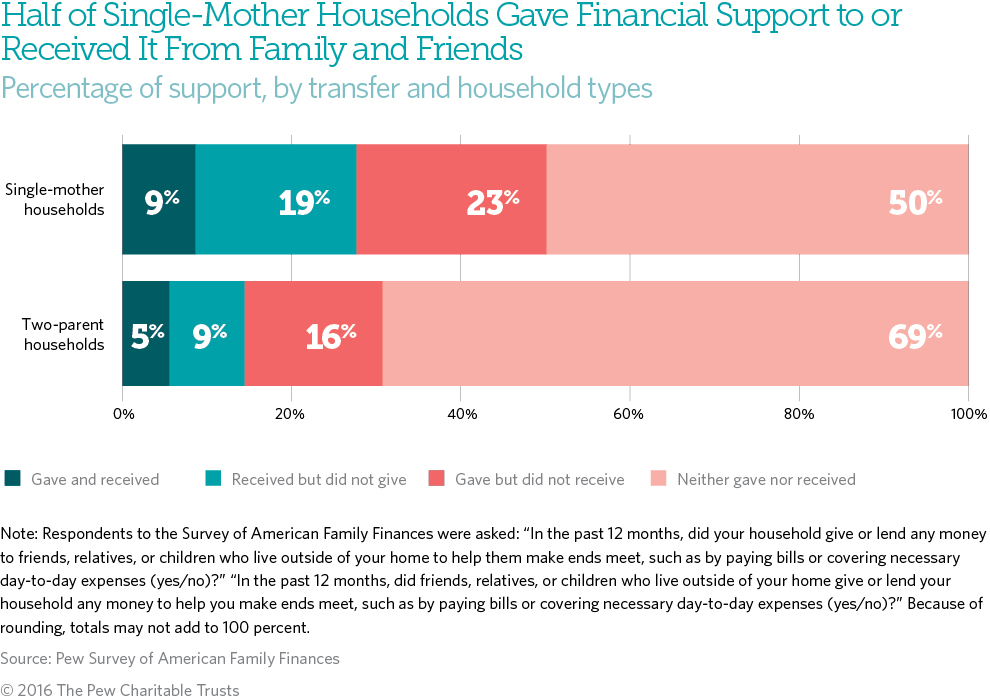

Households headed by single mothers appear to be more firmly rooted in their networks than those headed by two parents, if being both a giver and receiver of financial help is any indication.12 They are more likely than two-parent families to give or lend money to friends and family, despite having less wealth. This may be because they are more often linked with others who also have considerable financial need. In order to receive help in the future—financially, emotionally, or with in-kind help such as child care—single mothers may feel obligated to assist those in their networks as needed, in part because of norms of reciprocity.13

Half of all single-mother households reported having given financial help to or received it from friends or family in the past year, compared with just 3 in 10 two-parent households. Nearly one-quarter of single mothers reported giving financial support to those outside their household in the past year without receiving anything in return. (See Figure 2.) Even after accounting for other factors such as race, age, labor force participation, education, material hardship, homeownership, income, and low savings, being a single mother was still significantly associated with a higher likelihood of giving money to family and friends in the past year.14 Single mothers are also twice as likely as two-parent households to say they received help more than once in the past 12 months (19 percent and 8 percent, respectively). (See Table A.1 on Page 12.)

Despite their generosity, three-quarters of single mothers who gave or lent money considered the practice to be a burden, compared with two-thirds of respondents from two-parent households. That single mothers gave anyway may indicate what some scholars call “negative social capital,” in other words that the network of family and friends that single mothers depend upon for assistance may also ask so much of them in return that they bear emotional and financial costs.15

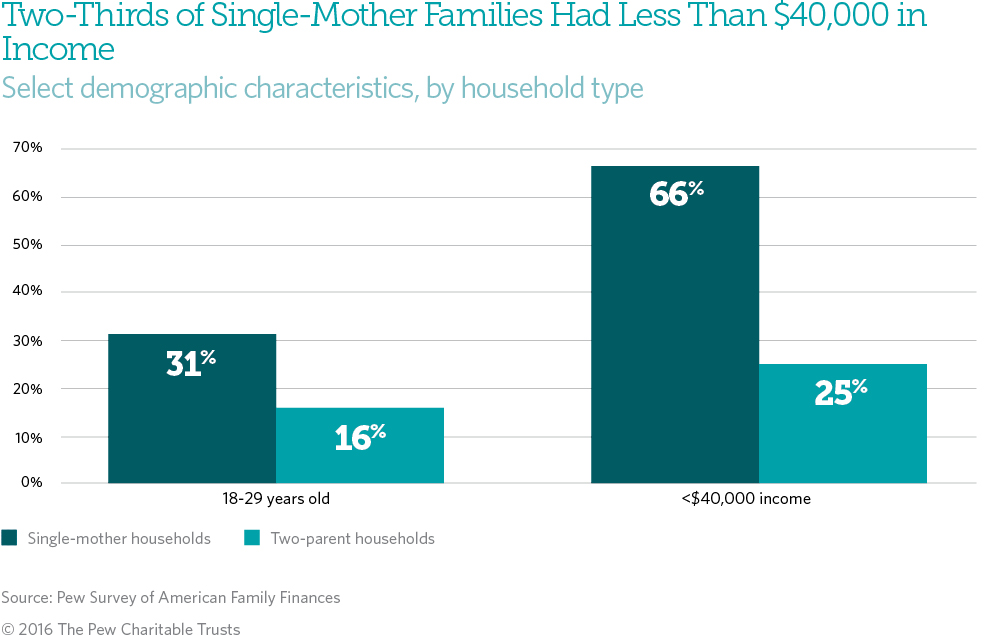

The demographic characteristics of single-mother families may suggest why they give and receive financial support outside their households so frequently. (See Figure 3.) Single mothers tend to be younger than twoparent households raising children, and nearly half have never been married. And they are in a more fragile financial state than households with two parents. Two-thirds of single-mother families had income under $40,000 in the previous year, and most have very little money in reserves: About half have virtually no net worth, while three-quarters of two-parent families have positive net worth. Single mothers report owing personal loans to friends and family at a higher rate than two-parent households (19 percent versus 11 percent) and are twice as likely to have past-due bills (26 percent versus 13 percent).

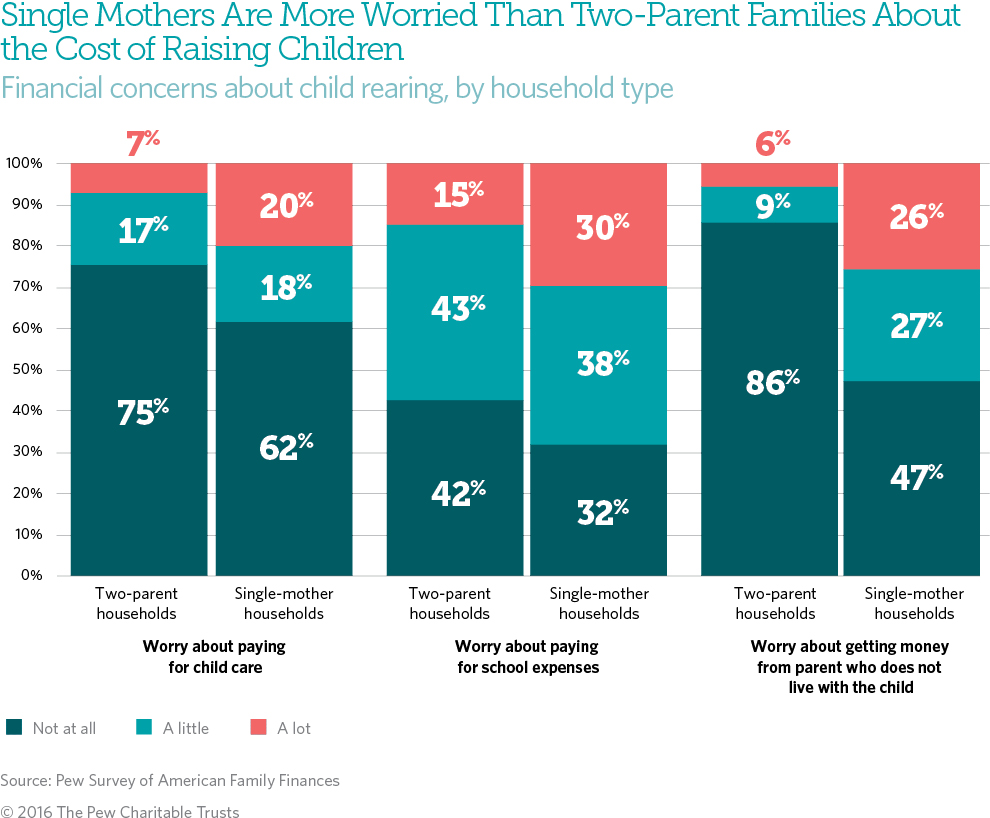

Single mothers also rely heavily on relatives for child care and report anxiety about the costs of raising children. Although single mothers receive regular no-cost child care at similar rates as two-parent households (9 percent), three times more single mothers have moved closer to relatives to access that child care help, compared with two-parent families (21 percent versus 7 percent, respectively). Single mothers are also more likely to say they worry “a lot” about paying for child care (20 percent) and school expenses (30 percent). (See Figure 4.) Onethird reported that the cost of raising children is a major source of stress.

Single mothers are more likely than two-parent households to receive money from and owe loans to friends and family. Single mothers are often in a more precarious financial state, and accordingly have more social and financial pressures because of their reliance on social networks and having few alternatives for monetary or other support.16

Conversely, wealthy households are the most likely to receive transfers that boost their mobility or encourage even more wealth building

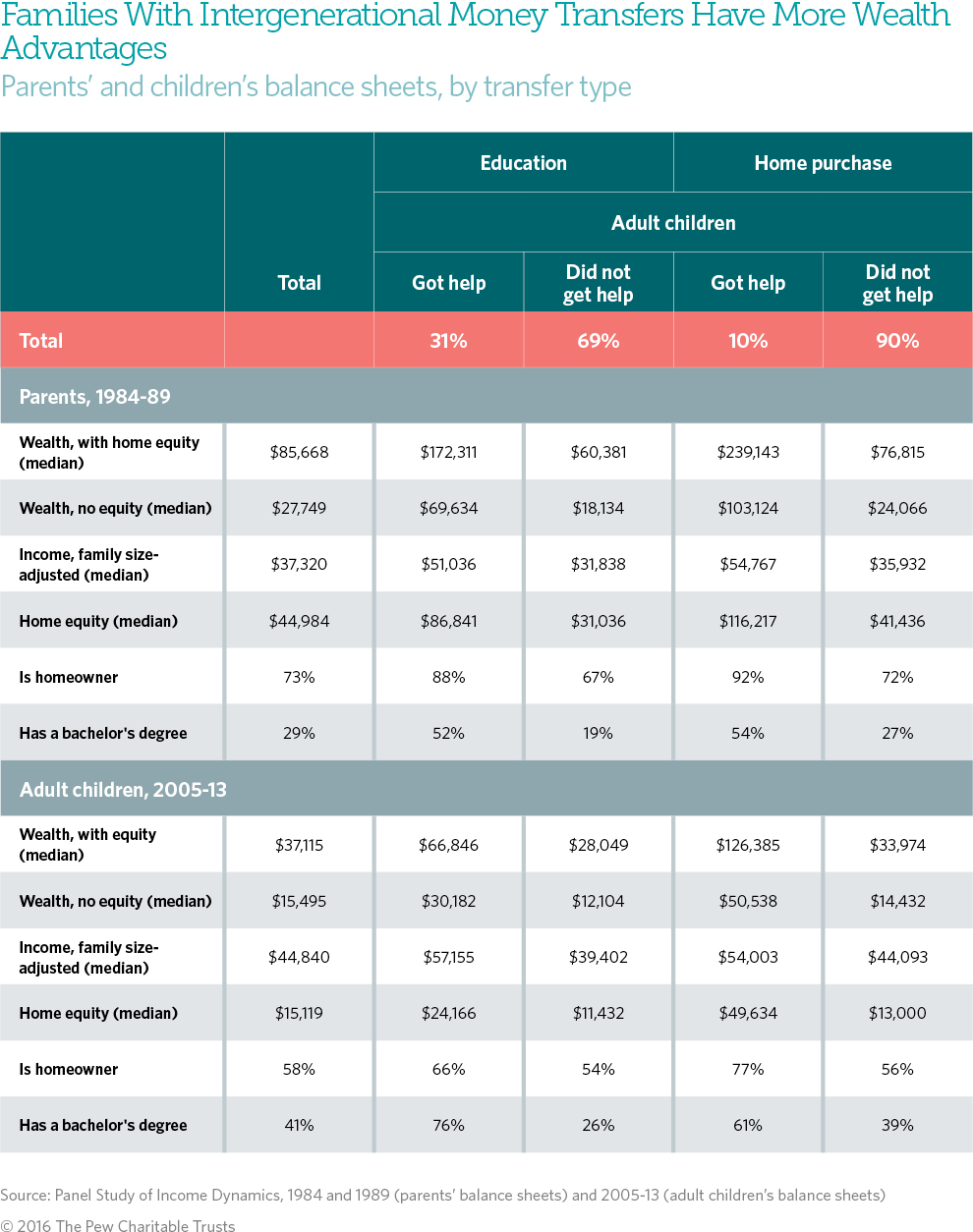

As discussed in the previous sections, extended family and friends often help households navigate financial hardships, but these social networks can also be instrumental for fostering economic mobility. One way in which this occurs is through intergenerational wealth transfers, such as inheritances and gifts of money to support education and home purchases. As of 2013, 10 percent of adults in the Panel Study of Income Dynamics received help buying a home, and another 31 percent got funds for education from their parents.17 (See Table 1; see Appendix: Data and Methods for information about the Panel Study of Income Dynamics.)

Not surprisingly, adults raised in wealthy families were more likely to receive such transfers. Among those who reported receiving money for higher education or home purchases, 52 percent and 61 percent, respectively, came from the wealthiest families, or those among the top third of wealth holders. In contrast, just 14 percent who received help for higher education and 6 percent who received help for home purchases were raised in the least wealthy families. (See Figure 5.)

Adult children who received transfers of money from their parents also have healthier balance sheets on the whole than those who did not. Specifically, those who got help with education had 2.4 times higher total net worth, and those who received money to buy a home had 3.7 times higher total net worth than those who did not receive help. Their parents also had healthier balance sheets. Parents who provided money for education or homeownership in the 1980s had about three times the total net worth of their peers who did not give such transfers and were more likely to be homeowners, to be college-educated, and to have higher incomes. (See Table 1.)

It is important to note that transfers alone do not account for healthier balance sheets among adults today. Those who received transfers of money were raised in more economically advantaged households, and these advantages convey in other ways, in addition to receiving money. The transfers, however, do reinforce existing gaps in wealth, income, and other socioeconomic markers such as homeownership and educational attainment.

Inheritance is relatively rare in the overall population: 15 percent in the Survey of American Family Finances. (See Table A.1.) However, one-quarter (26 percent) of respondents from white, high-income households reported receiving an inheritance, as did one-fifth (20 percent) of those from white, middle-income households.18 This suggests that inheritance is another way in which extended family transfers can reinforce advantages and influence the wealth and economic mobility of the next generation.19

Although inheritance is relatively rare in the overall population (15 percent in the Survey of American Family Finances), one-quarter (26 percent) of respondents from white, high-income households reported receiving an inheritance. ...

Conclusion

The safety net provided to households by friends and relatives is a hidden dimension of the financial system and one that may reinforce existing advantages and disadvantages in family finances. Those who face the most financial difficulties, such as single mothers, often give money to family and friends at higher rates than others, such that three-quarters of households headed by single mothers who provided such help in the past year said doing so was a burden. In contrast, those with the most financial advantages, such as those raised by the wealthiest families, overwhelmingly receive the most mobility-enhancing transfers of money, including help with higher education and home purchases. In this way, households’ social networks may serve to reinforce existing wealth differences.

Despite these concerns, for those in the most difficult financial states—especially significant material hardship— having friends and family available to help may prevent financial ruin. For that reason, this support may be essential to the financial survival of the most vulnerable households, even if it means that they will be called upon at some future date to return the favor.

How Do Families Cope With Financial Shocks?

The role of emergency savings in family financial security

What Resources Do Families Have for Financial Emergencies?

The role of emergency savings in family financial security

Barriers to Saving and Policy Opportunities

The role of emergency savings in family financial security

America’s Overdose Crisis

Sign up for our five-email course explaining the overdose crisis in America, the state of treatment access, and ways to improve care

Sign up

ADDITIONAL RESOURCES

Podcast

Article