Cap on the State and Local Tax Deduction Likely to Affect States Beyond New York and California

2 key facts suggest impact of the new federal tax provision could be far-reaching

The tax law passed by Congress in 2017 placed a $10,000 cap on the state and local tax (SALT) deduction, which allows filers who itemize to subtract state and local property and sales or income taxes from their federal taxable income. Policymakers across the country are examining this new cap’s potential impact on states, but much of that attention has concentrated on a handful of coastal states with large urban centers, such as New York and California. However, IRS data for tax year 2015 reveal two key facts about the deduction—the variety of states with average claims above the cap and the difference in states’ claim rates (the percentage of filers who claimed the deduction)—which together suggest this focus may be too narrow.

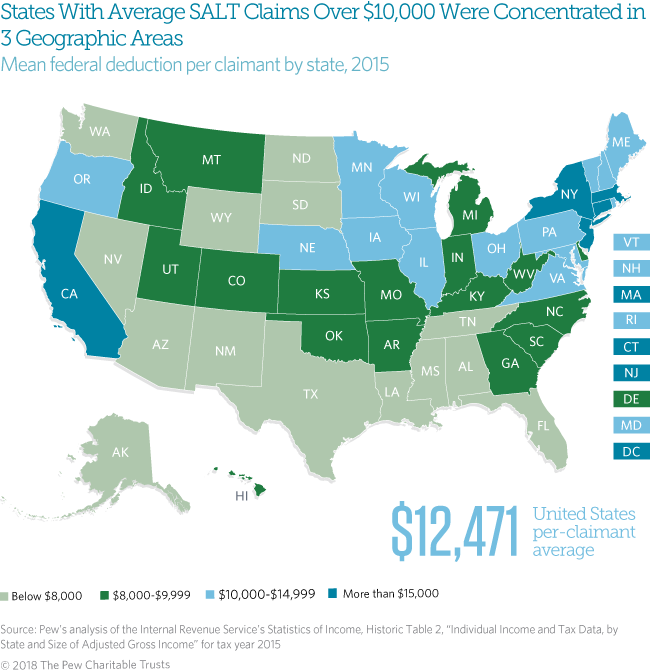

Fact 1: Claims in 19 states and D.C. averaged more than $10,000

In 2015, filers in 19 states and the District of Columbia who took the SALT deduction claimed more on average than the new cap allows. These jurisdictions are clustered in three geographic areas—the Northeast, upper Midwest, and West—each consisting of diverse states in terms of population size. (See Figure 1.) For example, the Northeast group includes states with large populations such as Pennsylvania, New York, and New Jersey, and some with smaller populations, including New Hampshire, Maine, and Vermont. The Midwest cluster similarly includes an array of state types, from populous Illinois to less populous Iowa.

States’ above-the-cap averages ranged widely from over $22,000 in New York to just $10,121 in New Hampshire. Five states—California, Connecticut, Massachusetts, New Jersey, and New York—had average deduction amounts that exceeded $15,000 per claimant in 2015. (See Table 1.)

Fact 2: Higher average deductions do not always correspond to higher claim rates

States with the highest mean deduction amounts do not necessarily have the nation’s highest claim rates—the share of filers that take the deduction. For example, California ranked third in the average amount claimed ($18,438) but 11th in claim rate (34 percent), while Maryland was eighth and first, respectively. These numbers indicate that the cap may affect a greater share of filers in Maryland, even though California filers claimed more on average.

SALT Claims in 19 States and D.C. Averaged More Than $10,000

Mean federal deduction per claimant and claim rate by state, 2015

| State | Per-claimant average | Claim rate |

|---|---|---|

|

New York |

$22,169 |

35% |

|

Connecticut |

$19,665 |

41% |

|

California |

$18,438 |

34% |

|

New Jersey |

$17,850 |

41% |

|

Washington, D.C. |

$16,443 |

40% |

|

Massachusetts |

$15,572 |

37% |

|

Minnesota |

$12,954 |

35% |

|

Maryland |

$12,931 |

46% |

|

Oregon |

$12,617 |

36% |

|

Illinois |

$12,524 |

31% |

|

Rhode Island |

$12,434 |

33% |

|

Vermont |

$12,408 |

27% |

|

Wisconsin |

$11,653 |

31% |

|

Maine |

$11,432 |

28% |

|

Virginia |

$11,288 |

37% |

|

Pennsylvania |

$11,248 |

29% |

|

Nebraska |

$11,088 |

28% |

|

Ohio |

$10,445 |

26% |

|

Iowa |

$10,164 |

30% |

|

New Hampshire |

$10,121 |

31% |

|

Notes: Per-claimant average is the average deduction for each tax filer in the state who claims it. Claim rate is the percentage of all tax filers in the state who claimed the deduction. Source: Pew’s analysis of the Internal Revenue Service’s Statistics of Income, Historic Table 2, “Individual Income and Tax Data, by State and Size of Adjusted Gross Income” for tax year 2015 |

||

Beyond the key facts

Although these two key points show that the focus on large, coastal states is probably too narrow, they still tell only part of the story. Even in the states where average claim amounts fall below the cap, individual filers whose SALT claims exceed $10,000 will face restricted deductions under the new provision. At the same time other provisions in the law, such as the increased standard deduction, could cause fewer filers to itemize their returns, changing the number of taxpayers who deduct state and local taxes and altering the SALT deduction’s distribution across states. These additional variables reinforce the need to look at all states, not only New York and California, when considering the impact of this policy change.

Phillip Oliff is a senior manager and Brakeyshia Samms is an associate with The Pew Charitable Trusts’ fiscal federalism initiative.

ADDITIONAL RESOURCES