FHA Loan Programs Do Not Reach Black Buyers of Manufactured Homes

Reforms could improve access to federally insured financing for historically underserved communities

Overview

Americans have difficulty getting loans to buy manufactured homes: Denial rates for these loans are more than seven times higher than for those used to purchase comparable site-built (nonmanufactured) homes.1 However, financing challenges are not the same for all buyers. Research shows that lenders deny manufactured home loans to Black applicants at significantly higher rates than they deny loans to White applicants, effectively keeping many Black buyers from one of the nation’s most affordable pathways to homeownership.2

This disparity is due in part to the type of loan product applicants seek. Manufactured home buyers who already own, or are financing, the land beneath their home are known as “landowners” and have multiple options when searching for manufactured home financing. They can apply for a mortgage, which finances both the manufactured home and the land beneath it, or a personal property loan, which finances the manufactured home only.

Lenders deny applications for personal property loans more often than they deny applications for mortgages—in part because some mortgages are insured by the Federal Housing Administration (FHA), which reimburses lenders when a borrower is unable to repay a loan. In contrast, personal property loans almost never have government backing, because the only federal program designed to insure such loans—the FHA’s Title I program—has been rendered obsolete as a result of outdated program rules. (Mortgages and personal property loans that lack government insurance are known as “conventional” loans.)

Although personal property loans are denied more often than mortgages, data shows that Black buyers are more likely than White buyers to apply for such loans. In some cases, Black buyers may choose to use personal property loans because they have no need or desire to include in the loan the land beneath their home. In addition, sometimes the land isn’t eligible to be used as collateral. However, other Black buyers may be responding to the loan options available to them—with few lenders to choose from. Nearly three-fourths of Black manufactured home buyers apply for financing from just two lenders, who are the nation’s leading issuers of personal property loans.

Policymakers looking to expand homeownership opportunities for Black households should consider ways to increase the number of Black manufactured home buyers who apply for FHA mortgages—and decrease the number who apply for conventional loans. To do this, the FHA should actively encourage major lenders to offer more federally insured loans. The agency should also expand its outreach efforts in the Southeastern United States, where most Black manufactured home buyers live—and where few manufactured home lenders offer FHA financing.3

At the same time, policymakers should seek to improve the accessibility of personal property loans for landowners who prefer or need them. The FHA should revitalize its dormant Title I program, which was designed to support personal property lending, by increasing the amount that can be borrowed under the program; permitting lenders to cut their expenses by using automated underwriting systems; and boosting the program’s insurance coverage rate.

Taken together, expanding the FHA’s mortgage program and updating Title I would help remedy the disparities Black applicants face when seeking manufactured home financing. The Pew Charitable Trusts estimates that such changes would allow the FHA to double Black applicants' access to manufactured home financing while adding only minimally to the risks borne by the agency.

Black applicants rarely seek FHA mortgages despite the program’s high approval rates

Landowners (manufactured home buyers who own or finance the land beneath their home) often apply for one of three types of financing: a conventional mortgage, a conventional personal property loan, or an FHA mortgage. Collectively, these options account for 95% of home purchase applications submitted by manufactured home buyers between 2018 and 2022.4 (Some buyers apply for loans insured or guaranteed by the Department of Veterans Affairs or the Department of Agriculture, but these loans are not available to all buyers and constitute a small share of the financing market.)

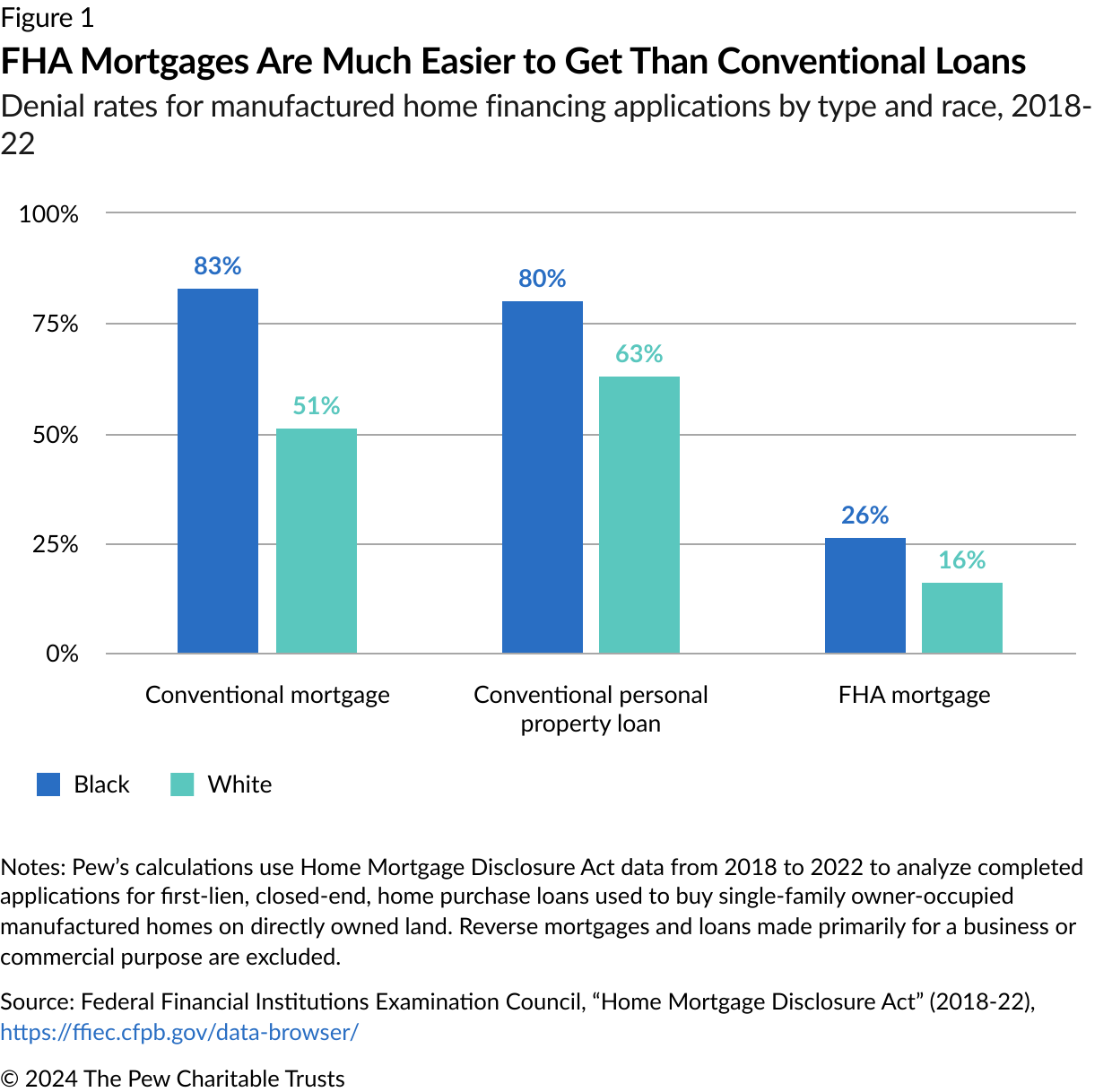

The type of financing borrowers apply for plays a major role in determining their likelihood of approval. Between 2018 and 2022, Black manufactured home buyers who applied for conventional mortgages or personal property loans were denied 83% and 80% of the time, respectively, compared with just 26% of Black manufactured home buyers who applied for FHA mortgages. White applicants were also more likely to be denied for conventional loans than for FHA ones, but the disparity was smaller between loan types—and White applicants were substantially less likely than Black applicants to be denied for all loan types. (See Figure 1.)

Lenders deny applications for conventional loans more frequently than for FHA mortgages in part because conventional financing lacks federal government insurance to cover lender losses if a borrower defaults. For instance, if a borrower is unable to repay an FHA mortgage, the federal government reimburses the lender for 100% of the loan’s unpaid balance.5 But conventional loans include no such protections, so when lenders make conventional loans, they’re more selective about the borrowers they agree to finance. Borrowers who are approved for these loans have above-average household incomes, below-average debt-to-income-ratios, and below-average loan-to-value ratios; applicants who are unable to meet these strict standards are often denied.6

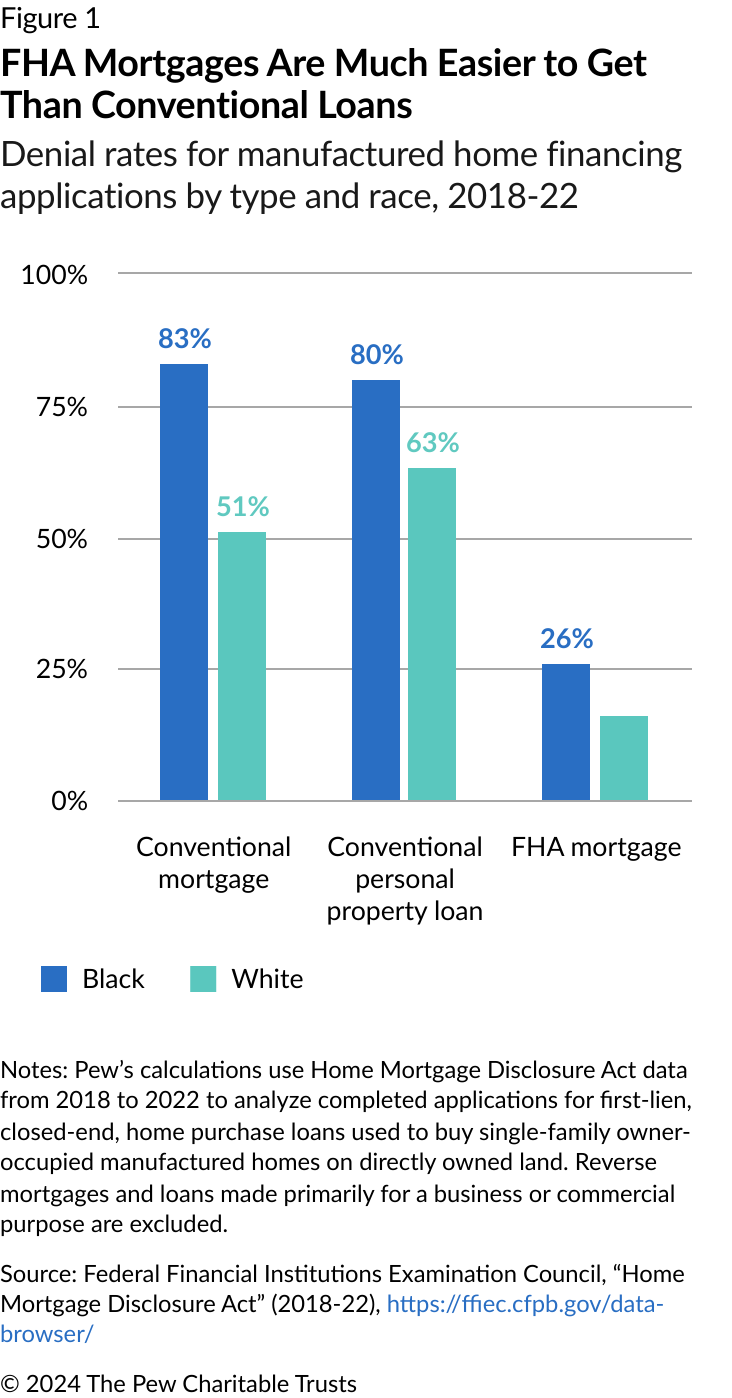

Yet despite the higher chance of being denied for a conventional loan than for an FHA loan, Black manufactured home buyers apply for conventional loans far more often than for FHA mortgages. From 2018 to 2022, 92% of Black borrowers applied for a conventional mortgage or personal property loan compared with just 6% who applied for an FHA mortgage (the other 2% applied for loans from the Department of Veterans Affairs or from the U.S. Department of Agriculture). In contrast, 75% of White applicants for manufactured homes sought a conventional loan and 19% applied for an FHA mortgage. (See Figure 2.) This difference is mostly accounted for by the relatively high share of Black applicants who sought personal property loans.

Mortgages generally have lower interest rates and stronger consumer protections than personal property loans, but some borrowers nevertheless need or prefer to use personal property loans. The reasons vary, but many homebuyers who already own the land beneath their home cite a desire to avoid encumbering the land, especially when it is family or Tribal land.7 Research has shown that others opt for personal property loans because lenders can offer shorter terms and faster closing times for these loans than for mortgages, or because personal property loans enable buyers to skip the often cumbersome and sometimes impossible process for classifying manufactured homes as real property (i.e., real estate)—a necessary step for obtaining a mortgage.8 In the Southeastern United States, where most Black manufactured home buyers live, landowners are more likely to have inherited their land as heirs’ property than landowners in other parts of the country—which means they don’t have clear title to the land and may have an ownership stake with other family members. This circumstance is especially common among Black landowners and prevents them from titling home and land together as real estate to get a mortgage.9

Still, because most applications for personal property loans are denied, buyer preference cannot be the only reason why Black buyers apply for these loans at a higher rate than White buyers: If borrower preferences were the primary factor affecting loan selection, then one would expect to see fewer applications for conventional mortgages and more applications for FHA mortgages to maximize the chances of approval. Instead, it appears that some Black borrowers don’t have the option of using an FHA mortgage and end up applying for financing that may not be ideal for their particular situation.

Survey research from Texas, for instance, has found that recent manufactured home buyers who own their land and were assisted in obtaining financing by a manufactured home seller or retailer were more likely to choose a personal property loan than those who were assisted by a lender or real estate agent.10 This appears to indicate that how borrowers get their financing information can meaningfully influence the type of loan they apply for, which in turn can affect their chances of being approved.

Just two lenders handle 71% of loan applications from Black manufactured home buyers nationwide (the same two lenders handle just 39% of applications from White manufactured home buyers). These two lenders, who are affiliated with the nation’s largest manufactured home retailer, offer almost exclusively conventional loan products and are the nation’s leading issuers of personal property loans. Partly because of the loan products they offer, these lenders often deny applications for manufactured home financing: From 2018 to 2022, they rejected 76% of all applicants, including 84% of Black applicants, while all other manufactured home lenders collectively denied only 31% of applicants.

FHA programs can improve Black buyers' access to financing

Although Black manufactured home buyers rarely apply for FHA mortgages, these loans—which have more flexible underwriting standards than conventional loans—are especially well-suited to expanding access to credit for Black borrowers, who on average have lower incomes, credit scores, and savings than the U.S. population as a whole.11 For example, applicants with credit scores as low as 500 can qualify for an FHA loan while many conventional loans require a minimum score of 620. In addition, FHA loans enable borrowers to make down payments of as little as 3.5% of the total purchase price compared with 13% for the average conventional loan.

Not every Black manufactured home buyer is credit-ready, but data suggests that many of those who are denied conventional loans would qualify for FHA financing. Between 2018 and 2022, nearly 1 in 4 Black applicants who were denied conventional loans for a manufactured home had higher incomes and lower debt-to-income ratios than the average Black borrower who received an FHA loan for a manufactured home. Had those buyers who were denied a conventional loan instead applied for FHA financing, they likely would have been approved.

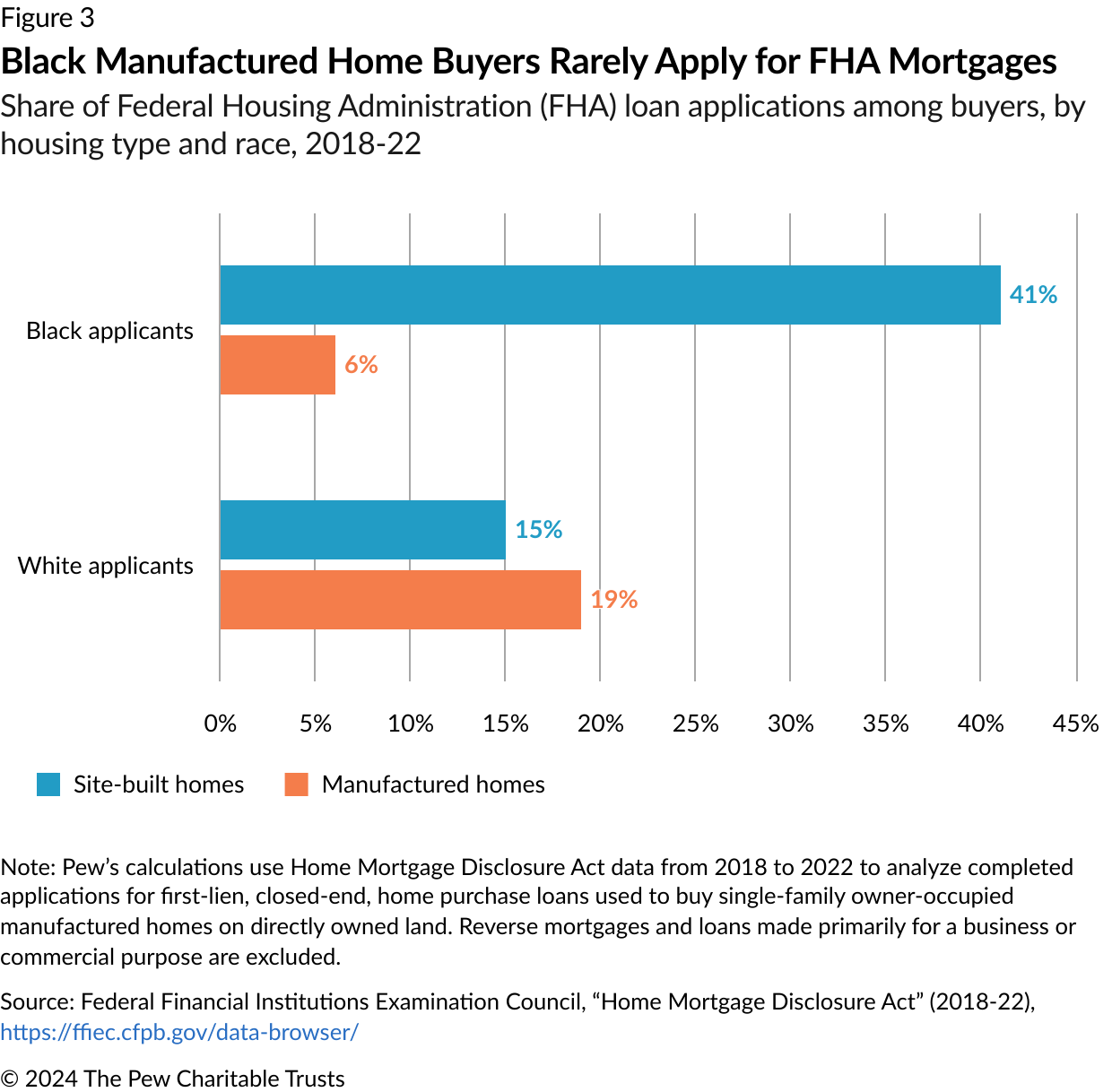

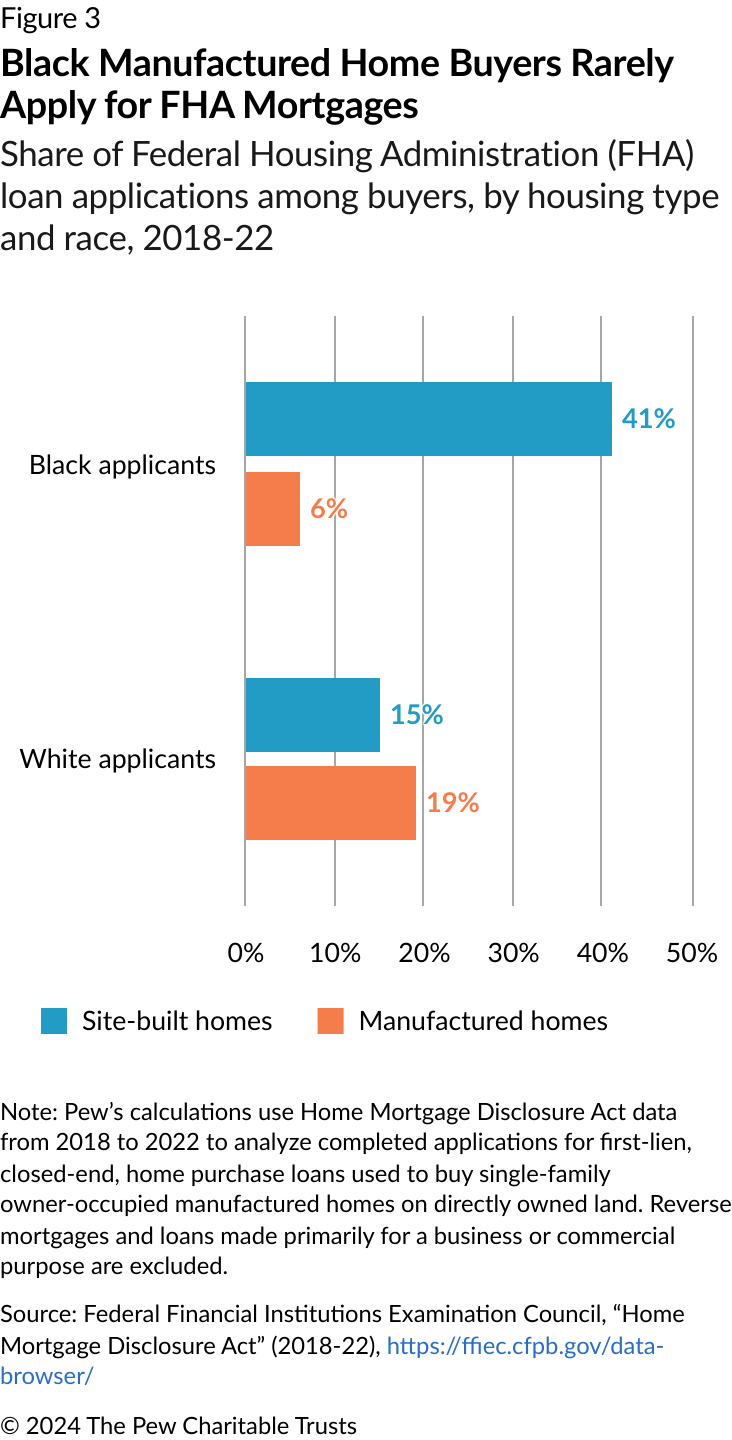

Moreover, data shows that FHA loans are popular among Black buyers of site-built homes. From 2018 to 2022, 41% of Black applicants seeking financing for a site-built home applied for an FHA mortgage, nearly seven times the rate of Black applicants seeking a manufactured home loan (see Figure 3)—further evidence suggesting that Black manufactured home buyers might choose an FHA mortgage if presented the option. In contrast, White applicants sought FHA loans in roughly equal measure regardless of how their home was constructed—about 15% of site-built and 19% of manufactured home loan applications from White borrowers were for FHA financing.

Expanding the availability of FHA mortgages could materially improve financing options for Black manufactured home buyers. If Black manufactured home buyers applied for FHA mortgages at the same rate as White buyers, an additional 2,000 loans would be made to Black borrowers every year, even if denial rates remained at current levels. And if Black manufactured home buyers sought FHA mortgages at the same rate as Black site-built home buyers, financing for Black manufactured home buyers would more than double, adding about 5,500 loans a year.

In fact, expanding the FHA’s lending portfolio would materially benefit manufactured home borrowers without substantially increasing risk to the agency. Data from Fannie Mae and Freddie Mac (government-sponsored enterprises that purchase mortgages in the secondary market) indicates that mortgages for manufactured homes had similar delinquency rates to mortgages for site-built homes from 2012 to 2021: Just 2.46% of manufactured home loans in Fannie Mae’s portfolio and 1.92% of those in Freddie Mac’s portfolio had ever been more than 180 days delinquent, compared with 2.22% and 2.05% of all Fannie’s and Freddie’s portfolio loans, respectively.12 Although these two government-sponsored enterprises have somewhat higher credit standards than the FHA, the figures suggest that expanding FHA loan programs is likely to involve little additional risk.

The FHA has an opportunity to expand access to credit for Black manufactured home buyers

To better serve Black manufactured home buyers, the FHA should identify and reduce barriers that limit the reach and usefulness of its loan programs. For instance, although FHA mortgages work well for many borrowers, they are infrequently used by Black landowners seeking manufactured homes, in part because few manufactured home lenders offer FHA financing in rural parts of the Southeastern United States.

The FHA should engage with manufactured home lenders in the region to better understand why many choose not to participate in its programs. Furthermore, the FHA should partner with community development financial institutions and nonprofit organizations that specialize in delivering loans to Black manufactured home applicants—which could help the FHA better identify any unique challenges to serving these borrowers and begin to understand how to overcome them.

At the same time, the FHA should update its Title I program to resolve the issues that have rendered it unusable in recent years. Title I worked reasonably well when its rules were last updated in 2008, but the program has since become obsolete because inflation has pushed average manufactured home prices above the maximum permitted loan amount. From 2018 to 2022, the program insured less than 1% of all personal property loans, which disproportionately affects Black manufactured home buyers, as they most often use these loans.

To resurrect Title I, the FHA could update the program’s loan limits and index them to inflation (a process the agency began in 2022); enable loans to be underwritten using the FHA’s TOTAL Mortgage Scorecard (an algorithm that helps lenders determine whether a loan is eligible for FHA insurance); lengthen the maximum loan term from 20 years to 30 years; and reduce net worth minimums that lenders require of applicants so that the minimums align with their mortgage program.13 These reforms would make Title I viable again, enabling lenders to extend government-insured personal property loans to more borrowers and increasing the overall availability of affordable manufactured home financing.

Conclusion

Black households often struggle to obtain manufactured home loans, even if they own or finance the land beneath the home. In part, this is because Black buyers rarely apply for FHA mortgages and instead turn to personal property loans, which lack government insurance; typically have stricter underwriting standards; and are denied at very high rates. The decision to apply for personal property loans may reflect Black borrowers' individual needs or preferences but may also be a product of their loan shopping experience: Nearly three-fourths of these buyers apply for financing from just two lenders, and these lenders almost exclusively offer conventional loans.

The FHA can improve Black households’ access to manufactured home loans by seeking to expand the number of lenders who offer FHA mortgages and by updating its Title I loan program for personal property loans. Doing so could more than double Black landowners' access to financing, enabling these borrowers to build wealth, keep their housing costs in check, and achieve homeownership.

External reviewers

This brief benefited from the valuable insights of Eileen Divringi, community development research specialist at the Federal Reserve Bank of Philadelphia, Lance George, director of research and information at the Housing Assistance Council, and Arica Young, Associate Director, I'm HOME Network and Underserved Mortgage Market Coalition (UMMC), Lincoln Institute of Land Policy. Although they reviewed drafts of the brief, neither they nor their institutions necessarily endorse the findings or conclusions.

Acknowledgments

This brief was researched and written by Pew staff members Adam Staveski and Rachel Siegel. The project team thanks Jennifer V. Doctors, Abi Ingoglia, David Lam, Aesah Lew, Omar Antonio Martínez, Avi Meyer, Tricia Olszewski, Reagan Ortiz, Travis Plunkett, and Mabel Yu for providing important communications, creative, editorial, and research support for this work.

Endnotes

- L. Liang, R. Siegel, and A. Staveski, “Data Shows Lack of Manufactured Home Financing Shuts Out Many Prospective Buyers,” The Pew Charitable Trusts, Dec. 7, 2022, https://www.pewtrusts.org/en/research-and-analysis/articles/2022/12/07/data-shows-lack-of-manufactured-home-financing-shuts-out-many-prospective-buyers. K. Kaul and D. Pang, “Manufactured Housing Could Ease the Supply Shortage, but Stakeholders Need to Be Cognizant of Existing Inequities,” Urban Wire (blog), Urban Institute, Aug. 24, 2022, https://www.urban.org/urban-wire/manufactured-housing-could-ease-supply-shortage-stakeholders-need-be-cognizant-existing.

- The Pew Charitable Trusts, “Millions of Americans Have Used Risky Financing Arrangements to Buy Homes” (2022), https://www.pewtrusts.org/en/research-and-analysis/issue-briefs/2022/04/millions-of-americans-have-used-risky-financing-arrangements-to-buy-homes; Consumer Financial Protection Bureau, “Manufactured Housing Finance: New Insights From the Home Mortgage Disclosure Act Data” (2021), https://files.consumerfinance.gov/f/documents/cfpb_manufactured-housing-finance-new-insights-hmda_report_2021-05.pdf; C. Herbert, C. Reed, and J. Shen, “Comparison of the Costs of Manufactured and Site-Built Housing” (Joint Center for Housing Studies of Harvard University, 2023), https://www.jchs.harvard.edu/research-areas/working-papers/comparison-costs-manufactured-and-site-built-housing.

- Consumer Financial Protection Bureau, “Consumer Finances in Rural Areas of the Southern Region” (2023), https://s3.amazonaws.com/files.consumerfinance.gov/f/documents/cfpb_or-data-point_consumer-finances-in-rural-south_2023-06.pdf.

- Data on manufactured home loans comes from the Home Mortgage Disclosure Act. Pew analyzed completed applications for first-lien, closed-end, home purchase loans used to buy single-family owner-occupied manufactured homes on directly owned land. Reverse mortgages and loans made primarily for a business or commercial purpose are excluded from the analysis.

- Federal Housing Administration, “Single Family Housing Policy Handbook 4000.1,” accessed Nov. 8, 2022, https://www.hud.gov/program_offices/housing/sfh/handbook_4000-1.

- Debt-to-income ratio is monthly debt divided by income. Loan-to-value ratio is the dollar amount of a mortgage as a share of the subject property’s appraised value.

- Freddie Mac, Center for Community Capital at the University of North Carolina at Chapel Hill, “The Loan Shopping Experiences of Manufactured Homeowners: Survey Report,” 10, 11.

- Ibid.; I'M HOME: Innovations in Manufactured Homes, “Manufactured Housing Resource Guide: Titling Homes as Real Property” (National Consumer Law Center, 2014), https://www.nclc.org/wp-content/uploads/2022/09/cfed-titling-homes.pdf.

- G.R. Dobbs; and C.J. Gaither, “How Much Heirs’ Property Is There? Using LightBox Data to Estimate Heirs’ Property Extent in the U.S.” (Mississippi State University Southern Rural Development Center, 2023, 2, 16), https://srdc.msstate.edu/sites/default/files/2023-06/dobbs_johnson-gaither_pre-print-manuscript-6.5.23_0.pdf.

- Freddie Mac, Center for Community Capital at the University of North Carolina at Chapel Hill, “The Loan Shopping Experiences of Manufactured Homeowners.”

- J.H. Choi, “Breaking Down the Black-White Homeownership Gap” (Urban Institute, 2020), https://www.urban.org/urban-wire/breaking-down-black-white-homeownership-gap.

- Fannie Mae, Fannie Mae Single-Family Loan Performance Data, 2023, https://capitalmarkets.fanniemae.com/credit-risk-transfer/single-family-credit-risk-transfer/fannie-mae-single-family-loan-performance-data; Freddie Mac, Single Family Loan-Level Dataset, 2023, https://www.freddiemac.com/research/datasets/sf-loanlevel-dataset.

- R. Siegel, R. Canavan, and T. Roche, The Pew Charitable Trusts, letter to Alanna McCargo, president, Ginnie Mae, and Julia Gordon, assistant secretary for housing and federal housing commissioner, U.S. Department of Housing and Urban Development, Sept. 26, 2022, https://www.pewtrusts.org/en/research-and-analysis/speeches-and-testimony/2022/09/26/manufactured-home-loan-program-could-expand-access-to-affordable-financing-but-needs-updates.

ADDITIONAL RESOURCES

Article

Article