Policymakers Can Expand Access to Lower-Cost Housing With Manufactured Homes

Homebuyers see significant savings compared with buying a new site-built home—especially when using a mortgage

Most renters in the United States say they would like to own their own homes, but with a limited supply of entry-level or affordable options available, many find it difficult to buy. Making it easier to buy manufactured homes could be part of the solution for first-time homebuyers and middle- or lower- income families that may not have enough savings for a down payment or the income to afford such an expensive purchase.

Prospective buyers face significant obstacles, in part because of high home prices, which have risen much faster than inflation in recent years. The median sale price in the first quarter of 2023 was $416,100, an increase of 26% the beginning of 2020. So policymakers are looking for ways to improve affordability by increasing the supply of entry-level housing, including manufactured homes.

Manufactured homes are affordable factory-built residences that are installed in one to three sections after being delivered to residential property. The majority of the building process is automated and standardized to one federal specification, which reduces costs compared with site-built or even modular housing. These homes come in all size ranges and can be built to look like other single-family homes: They can have slanted roofs, be affixed to foundations, and be owned as real estate just like site-built or stick-built homes (which are assembled on their permanent house location). Notably, about two-thirds of all owners of manufactured homes also own their land.

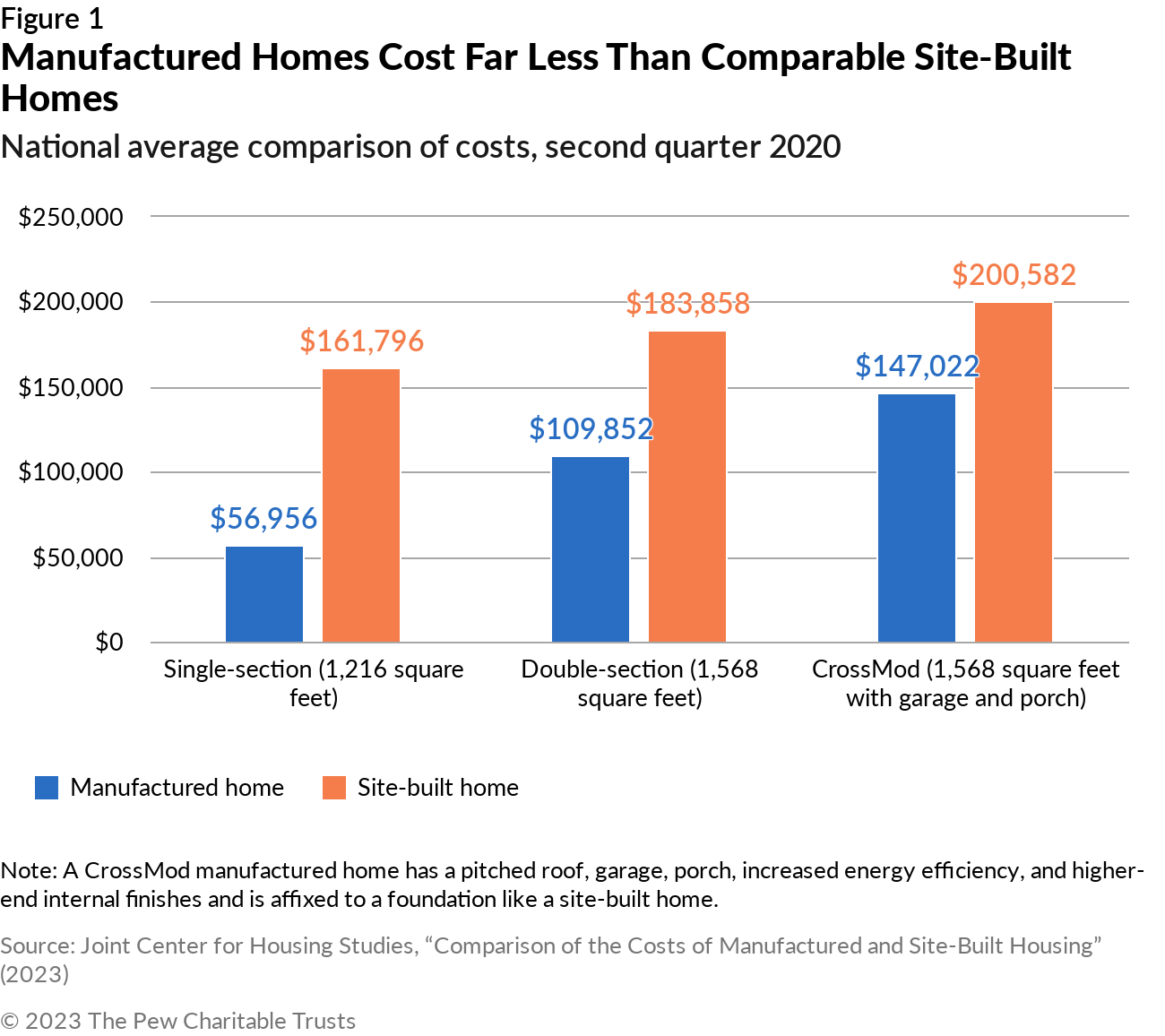

A recent study from the Joint Center for Housing Studies (JCHS) at Harvard University, funded by The Pew Charitable Trusts, found that manufactured homes cost far less than similar site-built homes.

Several factors determine the cost of a manufactured home—as paid by the homeowner—including the kind of structure being built and the financing used. The JCHS study found that the smallest of these homes, known as single-section or single-wide, have the greatest cost savings compared with a site-built home of a similar size. However, even larger manufactured homes with higher-end finishes such as porches and garages (called CrossMods by the Manufactured Housing Institute) still cost less than site-built versions.

The smallest savings compared with a site-built home would come from using a higher-end CrossMod, in part because such homes have more of the features of site-built homes. But even in that case, a buyer could save over $300 per month and more than $100,000 over the life of a 30-year mortgage compared with a site-built home. These estimated savings are consistent with findings from a prior manufactured housing cost-saving study published in 1998 by the National Association of Home Builders, indicating that these benefits have endured over multiple decades (See Table 1.)

Manufactured homes can be financed in various ways, but the greatest cost savings are achieved with a traditional home mortgage that covers both the home and the land. For a borrower to qualify for a mortgage, most states require that the home be attached to a foundation and be titled as real estate, which means it must be sited on owner-occupied land. Another common type of financing is a personal property loan that covers just the home and not the land. Such loans are an important source of financing for those who cannot get a mortgage but generally carry higher interest rates and fewer consumer protections. These borrowers include many who own both the home and land but title them separately, or those who rent the land.

Table 1

Homebuyers Can Save Significant Amounts With Manufactured Homes and Mortgage Financing

Cost comparison for CrossMod manufactured and comparable site-built homes

| Total cost of building and foundation | Interest rate | Term | Monthly payment | Total interest | Total payments | |

|---|---|---|---|---|---|---|

| Manufactured home CrossMod | $147,022 | 5.55% | 30 years | $839 | $155,159 | $302,181 |

| Site-built with garage (1,568 square feet with garage and porch) | $200,582 | 5.55% | 30 years | $1,145 | $211,684 | $412,266 |

| MH CrossMod cost savings (using a mortgage) | $53,561 | $306 | $56,524 | $110,084 |

|

Note: A CrossMod manufactured home has a pitched roof, garage, porch, increased energy efficiency, and higher-end internal finishes and is affixed to a foundation like a site-built home. The total cost of both housing types is based on findings from the Joint Center for Housing Studies, which added up the building costs for the home as well as the cost of the foundation and installation. For the manufactured home, transportation costs were also included. The average interest rate for a mortgage in 2022 was 5.55%. The higher the interest rate, the greater the difference in savings when a comparable quality lower-cost home is used. Cost savings are equal to manufactured home minus comparable site-built home but may be slightly different due to rounding of these numbers. Source: Joint Center for Housing Studies, “Comparison of the Costs of Manufactured and Site-Built Housing” (2023) |

The JCHS study highlights that policymakers have an effective tool at their disposal to address the issue of housing affordability in certain areas by enabling and encouraging greater deployment of manufactured homes. However, two keys to retaining the cost savings for the buyer are to ensure that these homes can be used as a substitute for more expensive single-family homes and that they can be financed with mortgages. With those two factors in place, homebuyers are more likely to achieve the substantial cost savings.

Federal and state policymakers can improve housing affordability and increase opportunities for prospective homebuyers by reducing barriers that limit the viability of manufactured homes compared with site-built homes, including differences in how they are zoned, appraised, and titled. Allowing for greater deployment of manufactured homes would expand the affordable housing stock and help make homeownership a reality for more Americans.

Rachel Siegel is a senior officer with The Pew Charitable Trusts’ housing policy initiative, and Alan van der Hilst is a senior research officer with Pew’s research review and support team.

ADDITIONAL RESOURCES