Federal Agencies Can Improve Access to Credit for Manufactured Home Buyers

FHA, Ginnie Mae, and Freddie Mac are well positioned to expand loan programs for certain borrowers

Personal property loans—which finance the purchase of a manufactured home but not the land beneath it—are used by more than 4 in 10 manufactured home buyers who take out a loan. These homes are constructed in a factory in one or more sections and driven to land for final installation. The affordability of these factory-built homes compared with housing built on-site has helped make them a key component of efforts to ease the national housing shortage. But the federal government currently does little to foster the availability of safe and affordable personal property loans to finance just the home and not the land beneath it.

That means many buyers face serious challenges getting access to safe and affordable financing for manufactured homes. Importantly, a quarter of personal property loan borrowers own their land, so they are not at risk for rent increases or eviction. In addition, a quarter don’t own land but don’t pay to live on it—likely family or Tribal land—and may be more able to get a long-term lease. Regardless of land ownership or long-term stable rights to land, nearly all home buyers who can’t or don’t want to title their home and land as real estate are excluded from federal support today. This disproportionately affects Hispanic, Black, and Indigenous borrowers, who are more likely than other borrowers to use personal property loans. Such problems with loan access then reduce the role that manufactured housing can play in boosting the supply of lower-cost homes.

In 2022, renewed federal interest in serving personal property loan borrowers marked a promising shift. The White House noted the need to make headway in improving manufactured home financing. Then the Federal Housing Administration (FHA), one of the federal agencies that insure home loans, and Ginnie Mae, the government-owned guarantor of federally insured home loans, proposed revamping the Title I insurance and guaranty programs for personal property loans. And Freddie Mac, one of the government-sponsored enterprises (GSEs) for housing finance, published plans to start a program for purchasing personal property loans. These initiatives could reduce barriers to entry for new lenders, increase the supply of loans to credit-ready buyers, improve consumer protections, and reduce borrower costs.

Options limited and costly for personal property loan borrowers

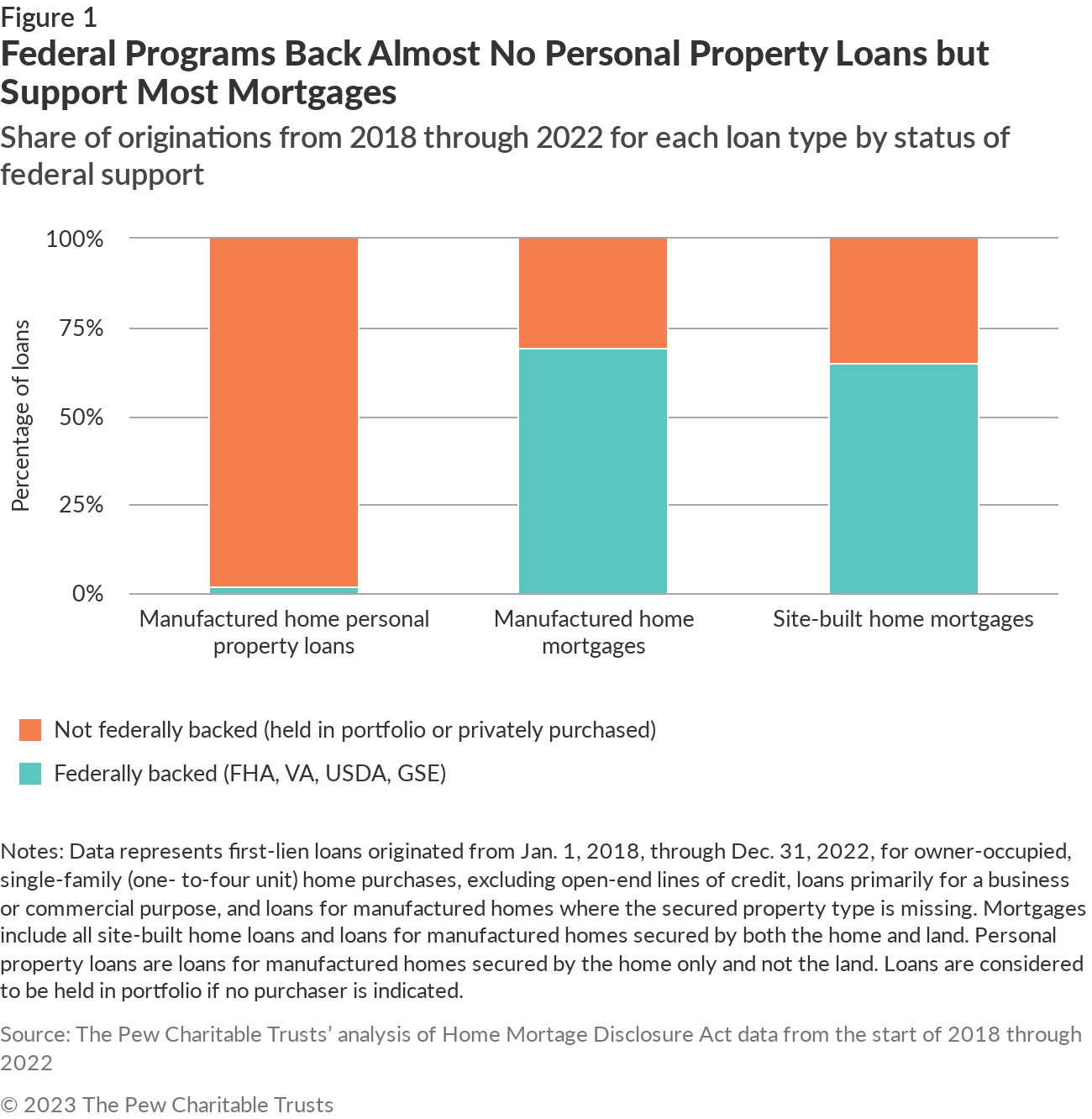

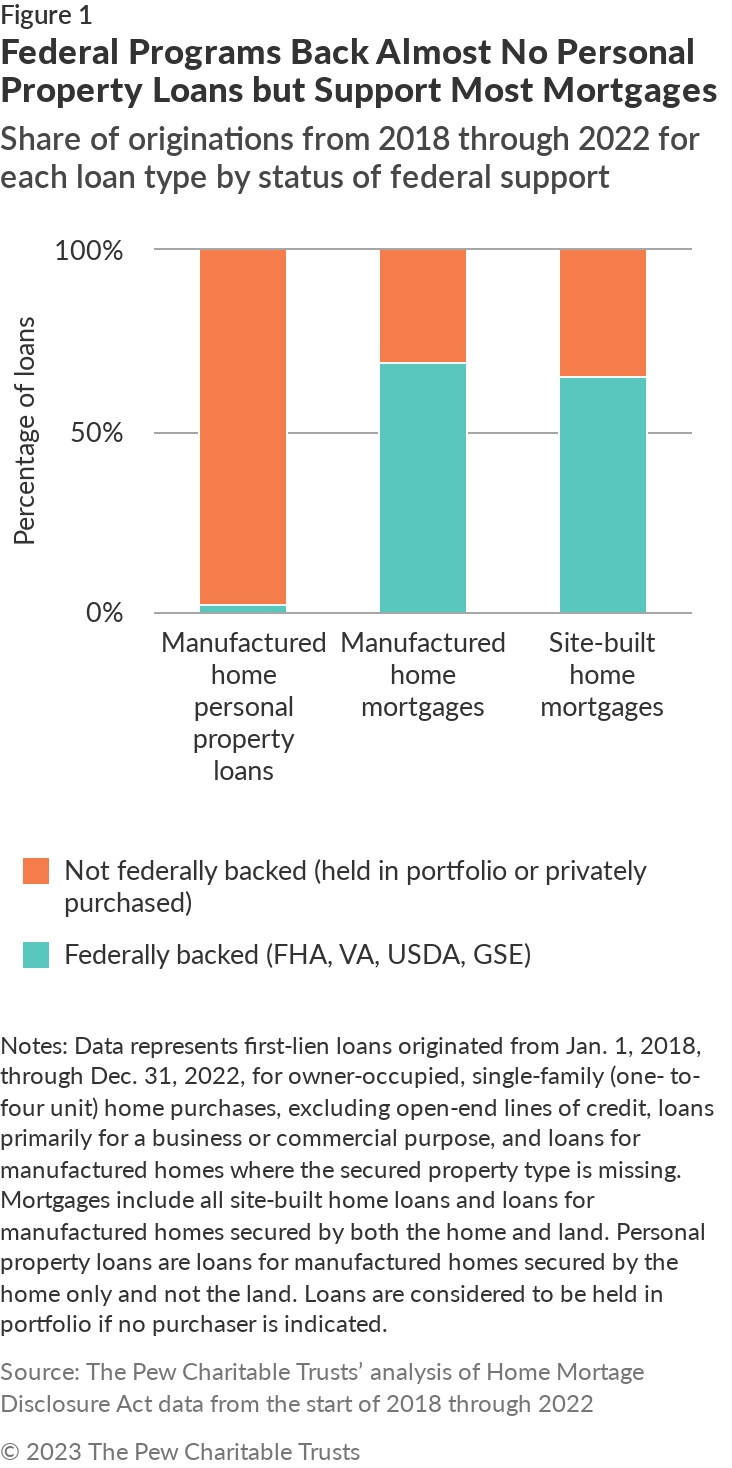

Federal lending supports play a critical role in creating a competitive mortgage market made up of thousands of lenders, but nothing comparable exists for personal property loans. Without government backing, just five lenders made 78% of personal property loans from 2018 through 2022. The Pew Charitable Trusts’ analysis of data collected by the Consumer Financial Protection Bureau under the Home Mortgage Disclosure Act found that the federal government supported more than 6 in 10 mortgages—loans for both a home and the land beneath—originated between 2018 to 2022 for site-built and manufactured home purchases. Meanwhile, 2% of personal property loans those years received federal support. (See Figure 1.)

Among the many federal supports for mortgage lending are FHA, U.S. Department of Veterans Affairs (VA), and U.S. Department of Agriculture programs for insuring or guaranteeing loans. Mortgages are often supported further by Ginnie Mae’s guaranty as well as purchases of loans by the two GSEs, Fannie Mae and Freddie Mac. Thanks to these programs, mortgage lenders have more funds available for originating new loans. They also bear less risk if a borrower defaults and charge less interest compared with lenders who make personal property loans because of stronger competition and lower cost of funds. In turn, federally backed mortgages allow more people with lower incomes, lower credit scores, and less savings to access homeownership safely and affordably.

In comparison, without federal support, most personal property lenders keep their loans in private portfolios, meaning they shoulder much of the risk and have less money available to originate more loans. Relatively few lenders can offer personal property loans under these constraints, reducing competition and likely increasing the cost to borrowers at least somewhat because of the higher cost of funds. For borrowers, these factors result in higher required credit standards to qualify for a loan compared with mortgages, and nearly two-thirds of applications are denied. With limited access to loans, some seeking a manufactured home use their savings for all-cash purchases, take risks with alternative financing, or cannot become homeowners.

Pew’s research has shown that lenders deny applications for FHA- or VA-backed mortgages for manufactured homes just slightly more often (14% and 13% respectively) than those for site-built homes (10% and 5%). In comparison, completed conventional mortgage applications (without government backing) are denied nearly nine times more often for manufactured homes (52%) than for site-built homes (6%). The success that federal programs have had in providing sources of safe and affordable mortgage financing for manufactured home purchases demonstrates what is possible in personal property financing with similar support.

Federal entities are well positioned to improve the market for personal property loans

Based on the FHA and Ginnie Mae’s 2022 request for input and Freddie Mac’s 2022-24 Duty to Serve plan, these agencies are well positioned to expand credit access in the personal property loan market, and their support for important consumer protections could greatly improve access to safe and affordable credit.

The FHA and Ginnie Mae operate Title I loan programs meant to support personal property loans, but outdated requirements have eliminated their usefulness over time. For example, strict caps on loan amounts haven’t been updated since 2009, so the average new manufactured home is too expensive to be financed with a Title I personal property loan. To address this, the FHA has proposed a method for routinely updating the loan limits based on average sale prices.

Currently, there are several lender requirements for the Title I program that are more onerous than those for FHA mortgages. The FHA mortgage program, for example, requires automated underwriting, which reduces lender costs, but is not allowed for Title I personal property loans. In addition, in order for lenders to be eligible to sell loans to Ginnie Mae, they must maintain a net worth at least four times higher for personal property loans than those in their Title II mortgage program.

Freddie Mac and Fannie Mae, meanwhile, have a congressionally mandated Duty to Serve manufactured home buyers, but their absence from the personal property loan market means that many potential purchasers are still excluded. Although personal property loans are explicitly allowed and stakeholders have noted the need for their inclusion repeatedly since 2017, none of these loans have yet to be purchased nor a program launched. However, in its latest plan, Freddie Mac proposed purchasing up to 2,500 conventional personal property loans in 2024 as part of a new program. Fannie Mae has yet to include such a program but has an opportunity to do so for its upcoming 2025-27 plans.

This is a long overdue start, and both GSEs should begin the process of purchasing loans—even if they start with some of the least-risky buyers, such as those with long-term rights to the land or who also own land.

Key consumer protections for new programs

The FHA and Freddie Mac have opportunities to bolster consumer protections for personal property loans as they update and craft their programs that would improve a buyer’s ability to maintain homeownership. Examples of such measures include standardization of:

- Default/eviction protections comparable to those for mortgage loans in default. These should include the right to cure or catch up on missed payments to reduce the risk of a home being repossessed.

- Minimum lease requirements for land renters needed to ensure federal programs support stable, long-term homeownership and reduce risks of default linked to unexpected changes in land rents or rights. Existing FHA and GSE policies could be combined to improve land-renter stability. For example, the FHA already requires a three-year initial lease and 180-day notice of community closure. And both Freddie Mac and Fannie Mae (in a program focused on loans used to purchase manufactured home communities) require additional protections for residents who live in the homes. Examples include a 30-day notice of rent increases, five-day grace periods for late land rent payments, and 60-day minimum notice of a community sale. The combination of requirements from these programs could provide important consumer protections.

If the FHA and Ginnie Mae update their Title I programs and Freddie Mac begins purchasing personal property loans, underserved populations would have greater access to safe and affordable loan options such as those available to homebuyers seeking traditional mortgages. Fannie Mae should also be looking at changes that can help improve access to these loans. The federal government and its housing finance partners must fill this financing gap to achieve the goal of using manufactured homes to meet more of the nation’s affordable housing needs.

Rachel Siegel leads research on financing for manufactured housing for The Pew Charitable Trusts’ housing policy initiative.

ADDITIONAL RESOURCES

Opinion