Neighborhood Poverty and Household Financial Security

Quick summary

In a previous study, The Pew Charitable Trusts examined the effects of neighborhood context on American families’ economic mobility. That analysis found that neighborhood poverty is associated with downward mobility, reinforcing other research that has shown a link between high-poverty neighborhoods and unemployment, poorer performing schools, and increased violence, all of which pose risks to residents’ economic security.

This chartbook draws on data from the Survey of American Family Finances, commissioned by Pew in November 2014, to illustrate the health of family balance sheets in high- and low-poverty communities across the United States and to examine how neighborhood context influences people’s attitudes toward the economy.

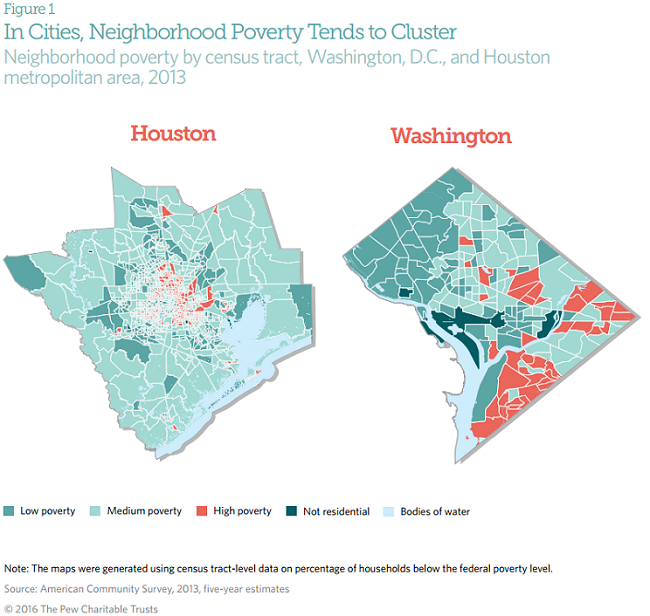

Neighborhood poverty is characterized by the percentage of households that live in poverty within a census tract. These maps illustrate the distribution of low-, medium-, and high-poverty neighborhoods in Washington, D.C., and the Houston metropolitan area and show that high-poverty neighborhoods tend to cluster geographically, as do low-poverty areas.

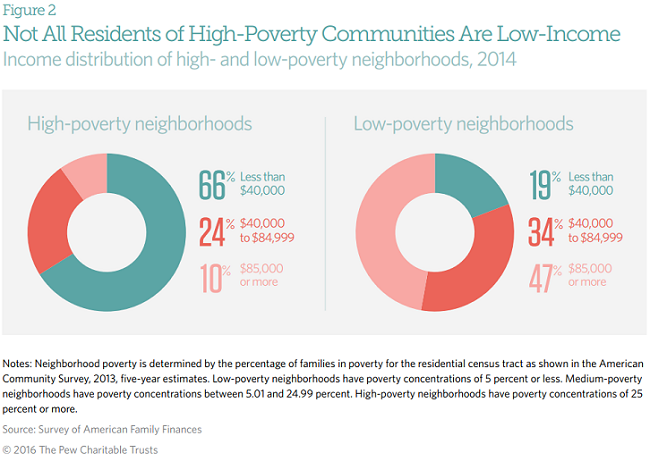

The designations of high and low poverty characterize neighborhoods generally, but the residents of these communities are not homogeneous in terms of income. Sizable numbers of high- and middle-income families live in high-poverty neighborhoods, and even more income variation is evident in low-poverty neighborhoods. Although most residents of high-poverty neighborhoods are in the bottom tier of the income distribution, almost a quarter are in the middle, and 1 in 10 is in the top of the income distribution. Similarly, fewer than half of residents of low-poverty neighborhoods are top earners, but more than a third are in the middle, and about a fifth are in the bottom income tier.

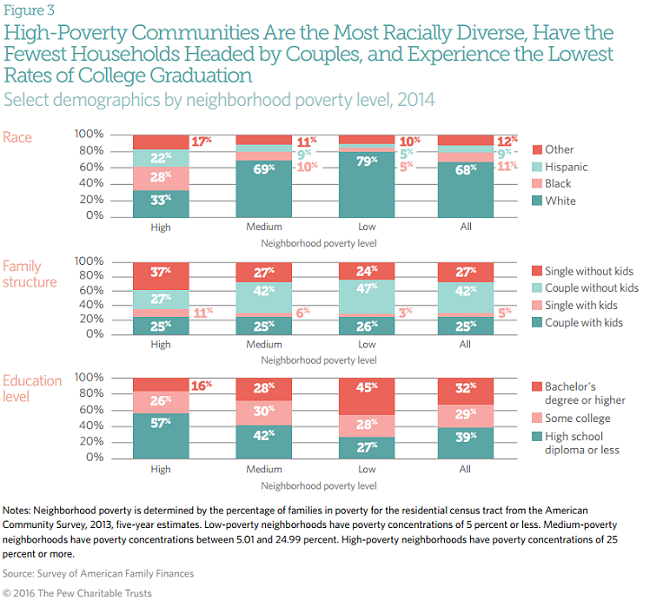

As the concentration of poverty decreases across neighborhoods, so does racial diversity: Three quarters of the residents of low-poverty neighborhoods are white, compared with just one-third in high-poverty communities. High- poverty neighborhoods also have the highest share of households headed by single people, both with and without children, while low-poverty neighborhoods have the highest share of households headed by a couple. The percentage of residents with some college is similar across the neighborhoods, but the share of residents with college degrees is significantly higher in areas that are low-poverty than in those that are high-poverty.

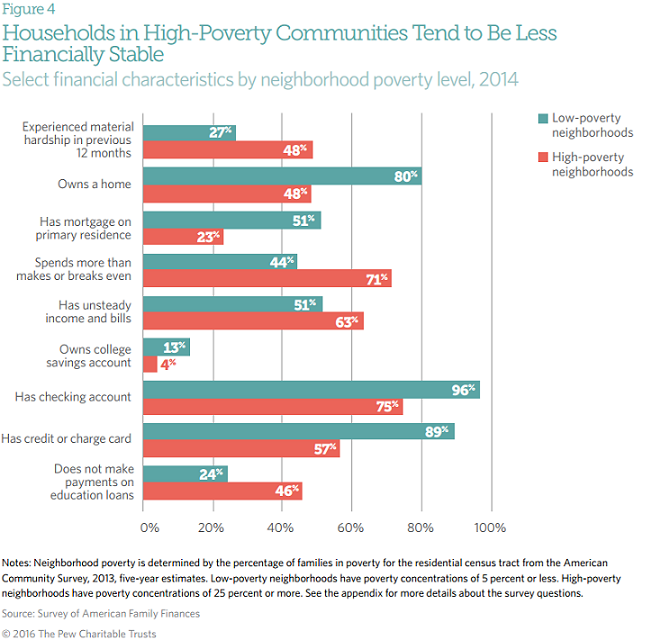

The financial stability of residents of low-poverty neighborhoods tends to be greater than that of those living in high-poverty neighborhoods. Residents of high-poverty areas are more likely to have unstable economic situations, earnings that are equal to or lower than expenses, and difficulty meeting basic financial obligations, such as mortgage, rent, or bills. Those living in low-poverty neighborhoods are more likely to be homeowners—and to have a mortgage on their primary residence—and they tend to be more equipped with practical financial products such as checking accounts, credit cards, or college savings accounts.

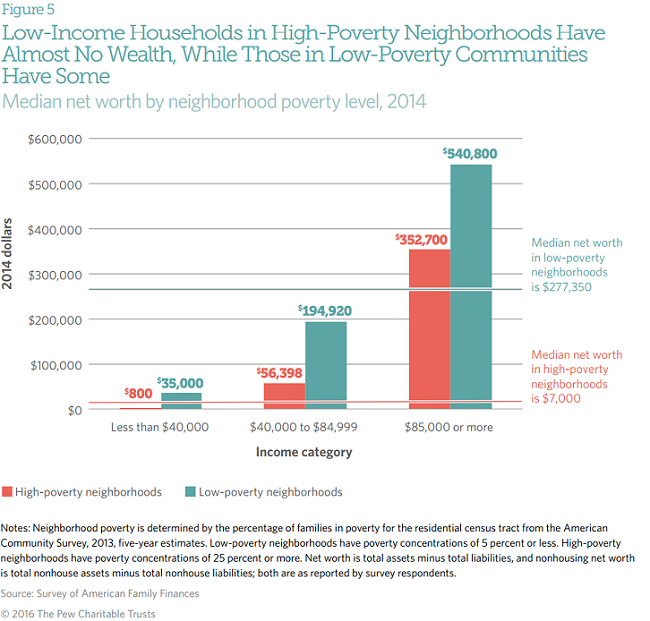

The typical household in a low-poverty neighborhood has 40 times higher net worth than the typical household in a high- poverty neighborhood. But families in the same income categories tend to have very different net worth levels depending on the neighborhood in which they live, with the most dramatic differences occurring among low-income households: Those in high-poverty neighborhoods have only $800 in accumulated wealth, compared with $35,000 for those in low-poverty communities. Figure 4 showed that residents of low-poverty areas are more likely to own homes, but homeownership does not explain this pronounced difference in net worth, which holds true regardless of home equity.

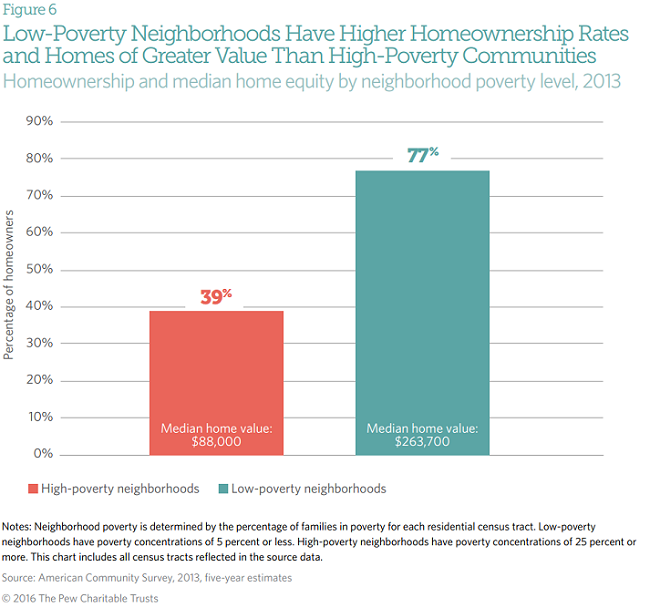

Residents of low-poverty neighborhoods are almost twice as likely to own a home as those in communities with high poverty. Median home values are also greater in low-poverty neighborhoods.

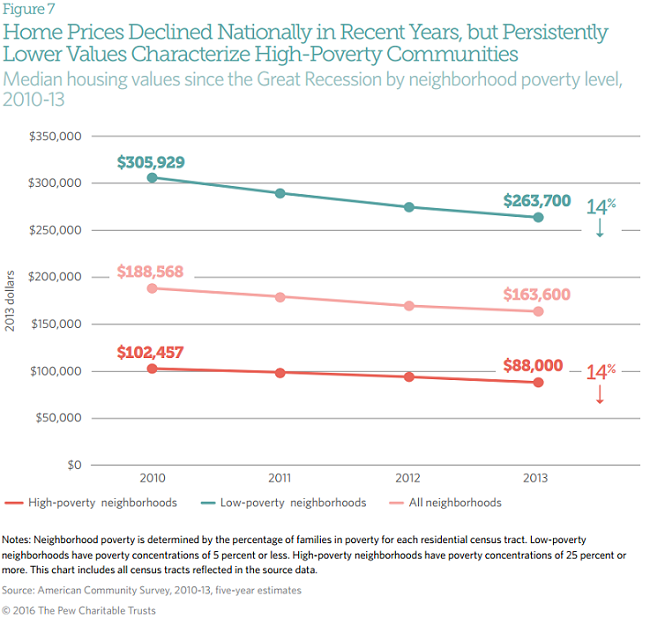

Following the Great Recession, housing prices declined in all neighborhood types while homeownership rates remained relatively stable. (Between 2010 and 2013, homeownership rates declined by 1.5 percentage points in low-poverty neighborhoods and by 2.3 percentage points in high-poverty communities.) Although home values fell 14 percent in both neighborhood types, low-poverty neighborhoods experienced a greater decline—$42,229 compared with $14,457 in high-poverty neighborhoods—in real dollar terms. Nevertheless, home prices remained much higher in low-poverty neighborhoods, suggesting that homeowners in these areas have maintained more equity in their homes.

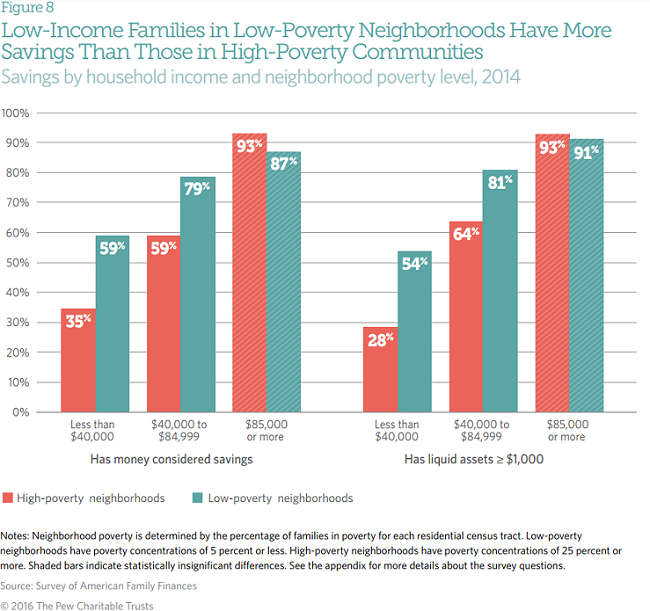

Residents of low-poverty neighborhoods are more likely to have savings and to have higher total savings than those in high-poverty neighborhoods. The savings discrepancy is especially notable among low-income households: Fifty-nine percent of low-income families living in low-poverty neighborhoods have money they consider to be savings, and 54 percent have at least $1,000 in liquid assets, compared with just 35 percent and 28 percent, respectively, among residents with the same income who reside in high-poverty areas. Even when controlling for household income, net worth, homeownership, race, age cohort, household composition, and presence of children, families living in high-poverty communities have lower savings than those living in low-poverty neighborhoods.

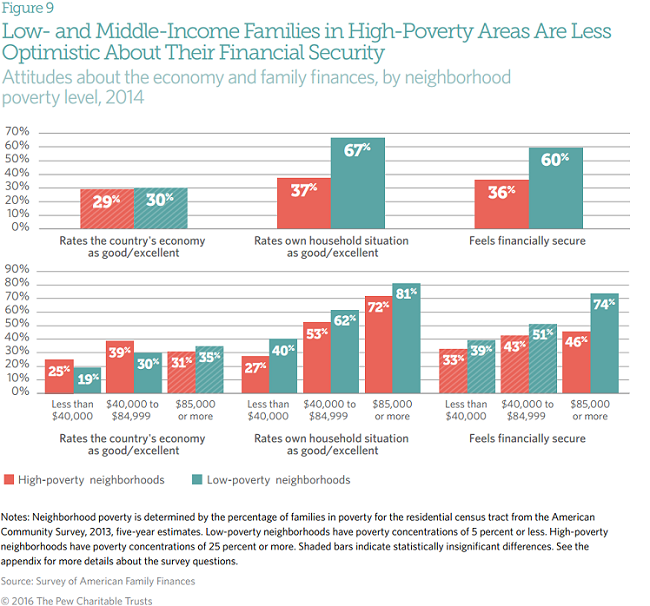

Overall, households in high- and low-poverty neighborhoods rate the country’s economy similarly. However, dividing the residents by income category shows that those at the bottom and in the middle of the income distribution are more likely to perceive the country’s economy as good or excellent if they live in a high-poverty rather than a low-poverty neighborhood.

Residents of low-poverty neighborhoods across income levels are much more optimistic about their own financial situations than those in high-poverty communities. Households in low-poverty areas not only rate their own financial situations as good or excellent more often than their counterparts in high-poverty neighborhoods, but they also feel more financially secure.

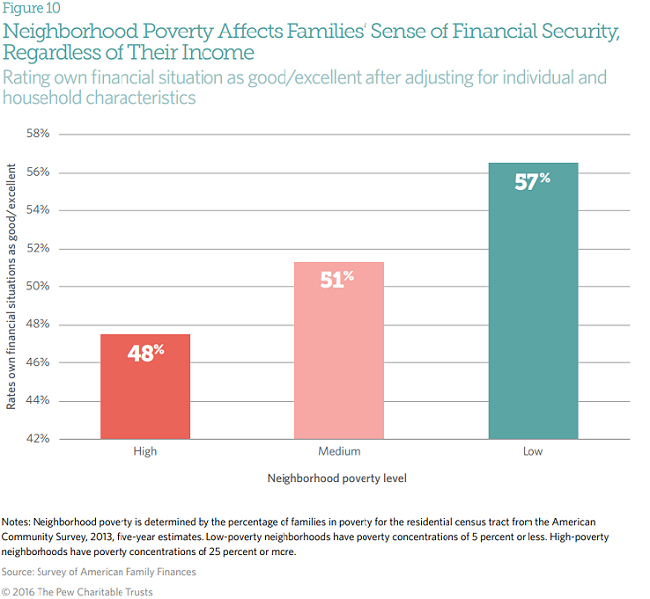

Even when holding constant household income, net worth, homeownership, race, age cohort, household composition, and the presence of children, families in high-poverty neighborhoods rate their own financial situations lower than those in low- and medium-poverty communities. Nearly 6 in 10 households in low poverty neighborhoods say their own financial situations are good or excellent, while only 48 percent of families in high-poverty areas give their economic situations the same rating.

ADDITIONAL RESOURCES