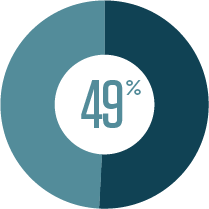

Workers in the United States accumulate the vast majority of their retirement savings through employer-based plans, but large gaps in coverage exist. Pew’s analysis shows that more than 30 million workers report they do not have access to an employer-based retirement plan.

The data, drawn from federal sources, show significant differences in access and participation across the states. For example, the share of workers in Wisconsin participating in employer-based plans, such as pensions or 401(k)s, was more than 20 percentage points higher than in Florida.

This data visualization shows how employer-based retirement plan access and participation vary among states and by characteristics such as employer size, industry, and wage and salary. The analysis focuses on full-time, full-year, private sector wage and salary workers, ages 18 to 64. Users can click through the various tabs to obtain information of interest and create printable state-level summaries.