How States Are Working to Address The Retirement Savings Challenge

An analysis of state-sponsored initiatives to help private sector workers save

© iStockphoto

© iStockphotoIf states weigh these factors carefully, they can make a meaningful improvement in the retirement security of many working Americans while minimizing costs to taxpayers.

Overview

Most Americans are not saving enough to pay for their retirement years. A majority of workers do not have a retirement savings plan through their employer, and less than 10 percent of all workers contribute to a plan outside of work.1

Not surprisingly, lower-income families are least likely to be saving. According to the U.S. Bureau of Labor Statistics, only 40 percent of private sector workers with wages in the lowest quarter of earners have access to retirement programs through their employers or unions.2

The failure to save enough—or save at all—has an impact on Americans in their working years and later in life. With life expectancy on the rise, workers’ efforts to prepare for retirement face threats from inadequate investment returns, large or unexpected expenses, and inflation. These risks affect all Americans, but those who have saved for retirement have a real advantage.

Government can play a role in helping Americans save for retirement. Policy tools range from offering incentives, such as tax breaks for contributions or for setting up a plan, to providing consumer protections for retirement plan participants. Congress and the Obama administration have proposed approaches to increase retirement savings, but no major federal legislation has passed on this issue since 2006.3 That inaction has led state policymakers to look for opportunities to fill the gap.

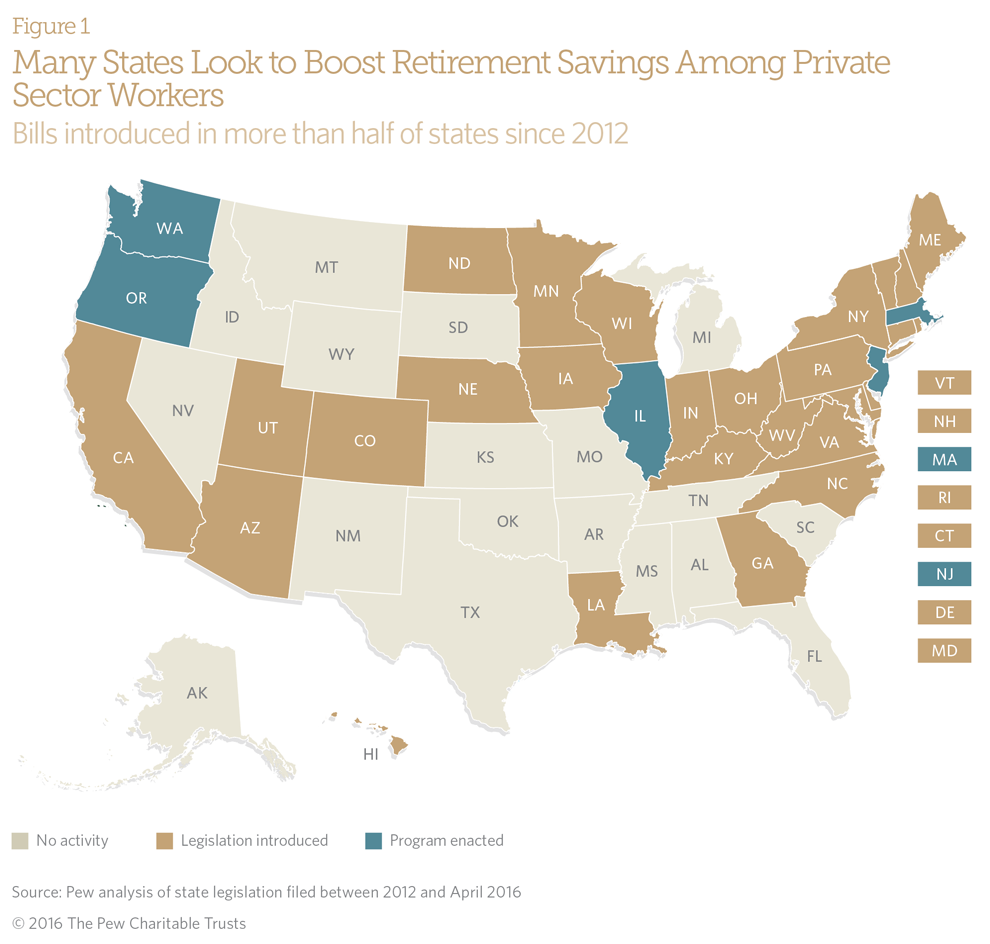

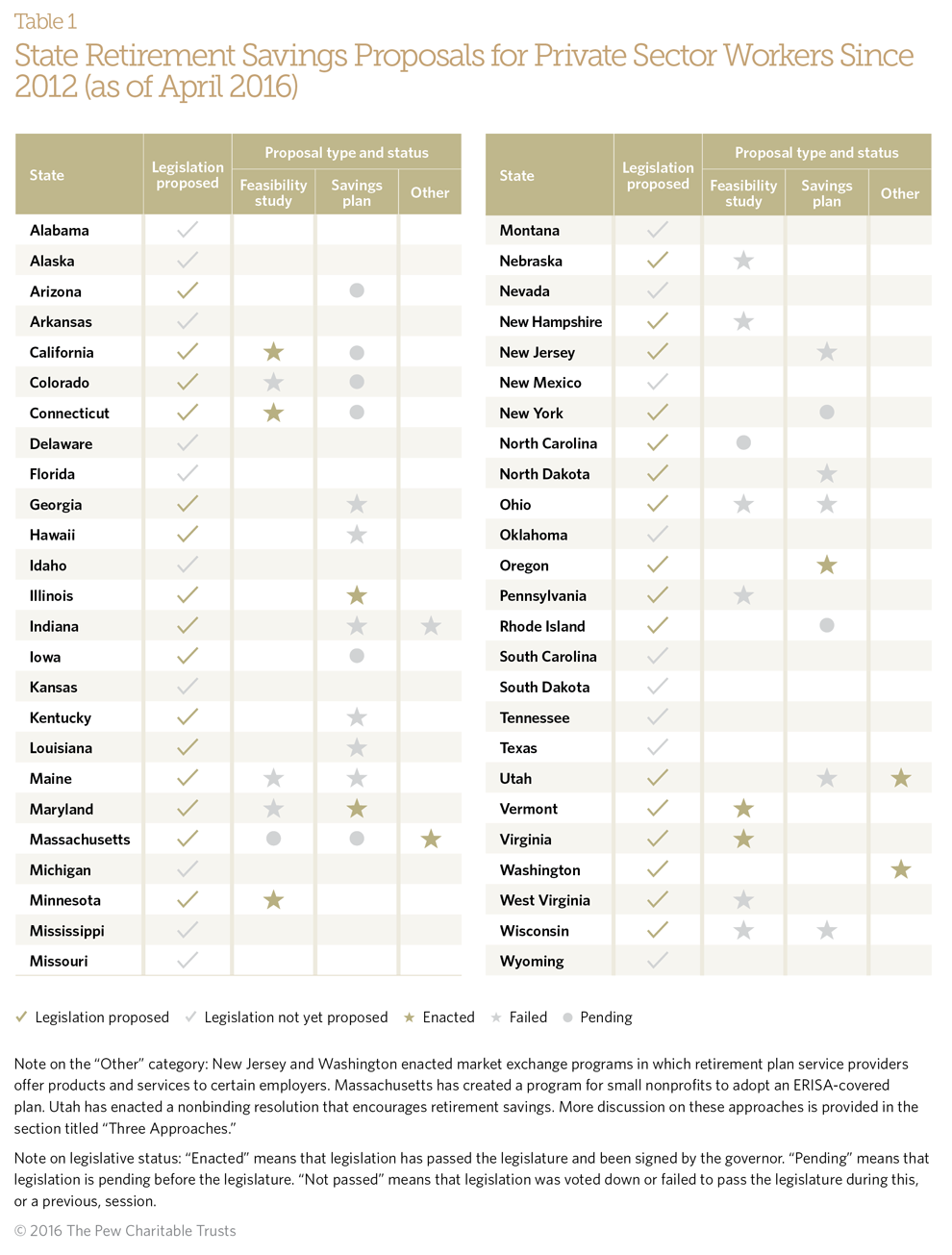

Since early 2012, over half of the states have introduced legislation to set up or study options for state-sponsored retirement savings programs for workers at private sector or nonprofit employers that do not offer plans.4 Illinois, Massachusetts, Oregon, New Jersey, and Washington have enacted state programs.

To help state policymakers craft effective policies, The Pew Charitable Trusts analyzed efforts in progress or under legislative consideration in 25 states. The states’ objectives are consistent: increase retirement savings and reduce poverty among retirees so they can support themselves without social assistance—spending that puts a strain on state budgets. Lawmakers also want to ensure that reforms are implemented successfully, impose minimal burdens on employers, build cost-effective and sustainable programs, and protect employee retirement savings.

These goals provide a framework for examination of the various state approaches. Lawmakers must explore how to maximize program effectiveness, minimize administrative and financial costs for employers, and manage their states’ legal and financial risks. These priorities can conflict and require consideration of difficult trade-offs, making the task of crafting proposals tougher. For example:

- The vast majority of workers would participate in a workplace retirement savings plan if given a chance. As a result, many state proposals require that employers of a certain size enroll all workers, though these employees can opt out. But small-business owners express concerns that mandating automatic enrollment could be an administrative burden, which could reduce the appeal of these proposals.

- States must carefully consider where to set the initial percentage of employee pay that will go into the accounts—known as the default contribution rate—because workers typically do not opt out of automatic enrollment or adjust this default rate once they are enrolled. Too low a rate could encourage employee participation but result in little savings, forcing the state to administer a large number of small account balances. Too high a rate could lead to higher balances but could also cause some workers to avoid taking part altogether.

- States must define employers’ role in communicating plan specifics. Many proposed laws seek to limit businesses’ responsibilities for implementation; however, unless a state makes a major effort to inform workers and employers about details in such cases, some targeted workers may opt out. Employers may have to engage in ongoing communications with workers about the program—and bear the economic and lost-time costs—if the state does not perform these outreach functions effectively.

- States face challenges in generating and protecting workers’ savings over the long run. Low-risk investments make losses less likely but also increase the chances that accounts won’t grow enough to meet retirees’ needs. Some states have looked at ways to guarantee certain rates of return, but that approach also brings possible risks and costs to the state.

Pew’s analysis identifies three approaches to increase retirement savings for private sector workers that states are considering. Under the first option, policymakers must decide whether the program will be set up under the federal Employee Retirement Income Security Act of 1974 (ERISA), the law that regulates pensions and sets a number of minimum standards. ERISA provides consumer protections for plan enrollees but can impose costly regulatory requirements on employers and increase a state’s administrative burden.

Under the second option, states can craft plans that do not fall under ERISA, such as the Secure Choice program in Illinois, which allows all workers in the state who do not have plans through their employers to make payroll contributions to individual retirement account plans. With the third option, states can help businesses voluntarily set up their own retirement savings plans, as is being done with the marketplace websites created for small employers by Washington and New Jersey.

Pew’s analysis identifies three approaches to increase retirement savings for private sector workers that states are considering.

This report also looks at the specific choices facing policymakers, including the range of approaches to regulating:

- Requirements for employers’ participation, responsibilities, and liabilities.

- Rules for employees’ enrollment, contributions, and withdrawals.

- How contributions will be invested and savings will be protected.

- How the programs will be governed and administered, including the likely costs and the potential state liabilities.

States must determine whether they have the administrative and financial capacity to manage large savings programs. Many already have experience running retirement plans for public employees, health exchanges under the Affordable Care Act, and 529 college savings plans. But creating viable state-run retirement programs for private sector workers can present different challenges in achieving both scale and efficiencies if they must manage many small account balances funded by the payroll systems of many small employers. States can learn from the experiences of one another as they consider the best paths forward.

States would be well served to make policy choices that balance competing objectives and take into consideration the specific economic and demographic characteristics of the workers who could participate in these plans.

The retirement savings challenge

Americans depend on three primary sources for income in old age: Social Security, individual savings or earnings, and workplace retirement plans. The state proposals studied in this report are meant to fill gaps in the employer-provided system.

Retirement plans come in two basic types: defined benefit plans, which include traditional pensions and cash balance plans, and defined contribution plans such as 401(k) plans and individual retirement accounts (IRAs). Most retirement savings occurs in the workplace through an employer-sponsored plan rather than an IRA.5 These plans often benefit from tax incentives for employers and employees, but they also take advantage of payroll systems to make saving easier. For example, workers can make smaller, regular contributions rather than waiting until the end of the year, when they may not remember or be able to make a personal IRA contribution. That helps make saving a habit.6

Defined benefit plans use a formula that usually provides a guaranteed lifetime benefit at a specified retirement age; these benefits typically are funded by employers. In defined contribution plans, benefits build over time with employee and often employer contributions. Long-term returns on investments are critical. These plans do not promise a specific benefit at retirement and are defined more by the accumulation of contributions over time.

Neither type of plan is risk-free. With a defined benefit plan, inflation can eat into the annuity if cost-of-living allowances are not included or if the company funding it fails or suspends the plan before a worker accumulates sufficient benefits.7

Defined contribution plans face their own risks, including the following:8

- Will workers outlive their retirement savings? Will the savings be enough to pay expenses for the rest of their lives? Will investment returns be high enough to reach an adequate level of assets? To what extent should workers be protected from investment volatility, high fees, and their own mistakes?

- Will sudden and unforeseen expenses, such as high medical costs, drain retirement funds too quickly?

- Will inflation erode the purchasing power of retirement funds, particularly if “safe” assets do not keep upwith the cost of living?

A critical factor in weighing the impact of these risks is who bears them. Workers shoulder all the market and longevity risks in a defined contribution plan, while the risks are shared by workers and employers in defined benefit plans.

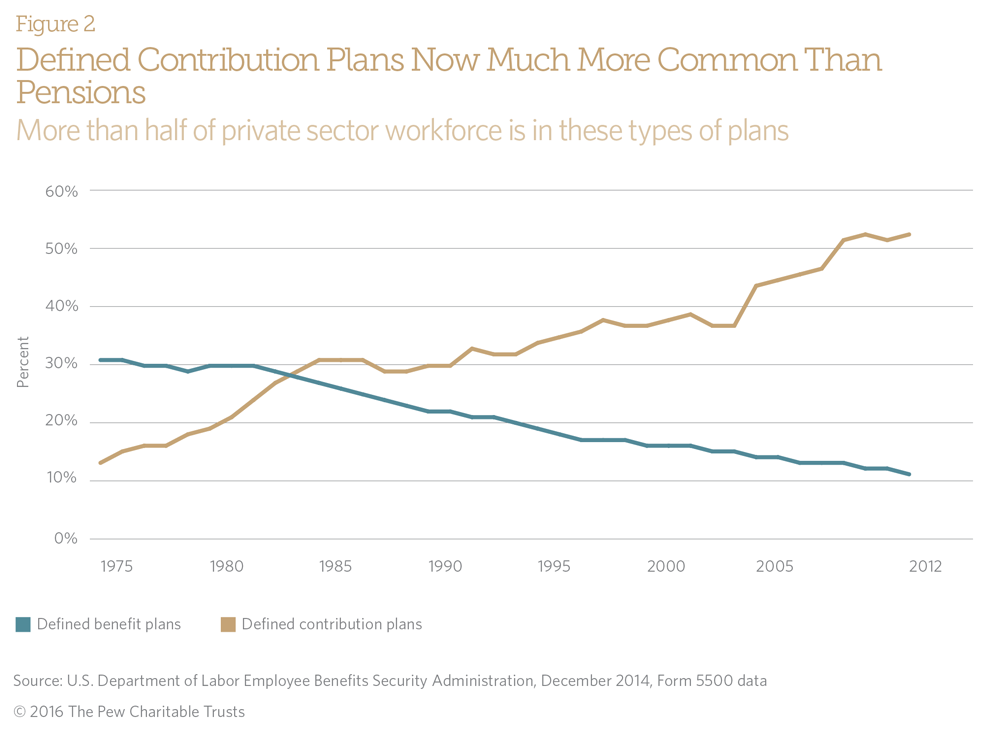

Defined contribution plans have become the dominant savings approach in the private sector in recent decades. In 1980, nearly 150,000 defined benefit plans covered 30 million active workers (30 percent of the workforce). By 2012, those numbers had shrunk: 43,601 defined benefit plans covered 16 million active U.S. workers (11 percent of the workforce). Over the same period, the number of defined contribution plans increased from about 340,800 to a peak of 686,900 plans in 2000 before decreasing slightly to 633,000 in 2012. Defined contribution plans covered 19 million workers (19 percent of the workforce) in 1980, but that number jumped to more than 75 million (53 percent of the workforce) by 2012. Although the number of defined contribution plans decreased after 2000, the number of active participants in such plans continued to rise, from 51 million to 75 million in 2012.9 Figure 2 shows these trends.

Overall, the growth of defined contribution plans has offset the decline of defined benefit plans in terms of the total number of Americans covered.10 But having access to a plan is not the whole story, particularly given the differences between the benefits offered by each type. For example, a recent report by the Center for Retirement Research found that total retirement wealth, which includes defined benefit accruals, defined contribution savings, and asset returns, has been relatively steady over time, despite the transition from traditional pensions to defined contribution plans. But employees in defined contribution plans bear all the investment risks.11 And because people are living considerably longer in retirement than they once did, the aggregate savings rate would have to increase to meet the greater expected need.

Key Terms: Access, Participation, and Coverage

Retirement policy often focuses on three major issues regarding workplace retirement plans: access, participation, and coverage. To provide access, an employer must offer a plan to workers, and workers must be eligible to participate under the terms of the plan. Participation refers to employees actually taking part in the plan, which typically requires making contributions. Depending on the employer, workers could make an active choice by signing up for a plan, or they could be enrolled automatically when they are hired, with the choice to opt out. Coverage refers to the number or proportion of workers covered by retirement plans and is a function of access and participation.

Although studies have reached different conclusions, many factors indicate that income will be inadequate for retired Americans in general.12 For example:

- A 2015 study from the Employee Benefit Research Institute estimated that the current American workforce will face an aggregate retirement savings shortfall of $4.13 trillion.13

- A 2012 study by the Urban Institute estimated that 30 to 40 percent of baby boomers (those born from 1946 through 1964) will not have enough income at age 70 to replace 75 percent of their pre-retirement earnings, a common standard for judging income adequacy in retirement.14

- The Center for Retirement Research’s National Retirement Risk Index provides a measure of the percentage of working-age American households at risk of being financially unprepared for retirement. The index indicates that the proportion of households facing a decline in their standard of living in retirement increased from 30 percent in 1989 to 52 percent in 2013.15

- Studies show that economic insecurity among older Americans of color is much higher than among white older Americans.16

Although there is no single accepted standard for assessing retirement savings readiness, many financial advisers say that retirees should be able to live off 4 percent of their assets per year or that they should accumulate an amount equal to 10 times their desired yearly income.17 For most workers, that is a formidable task.

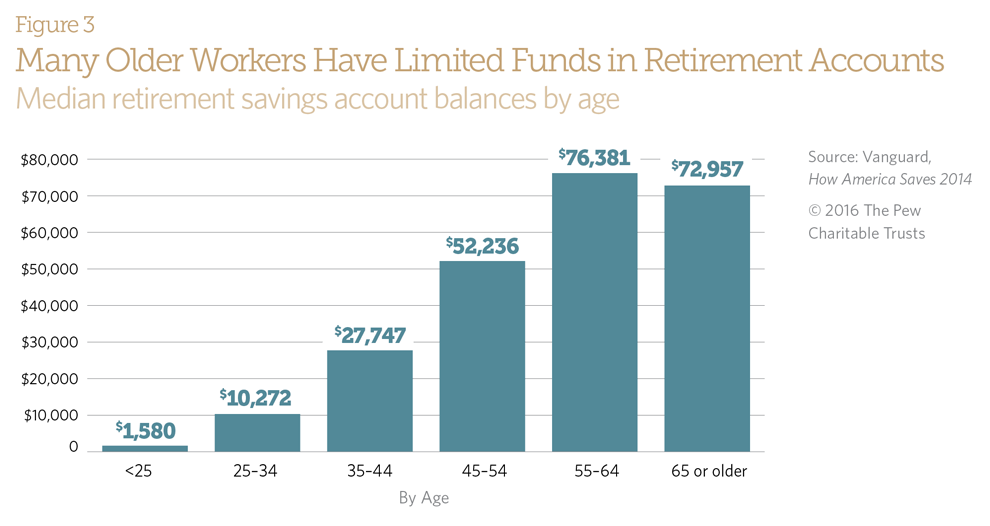

Figure 3 shows that the median defined contribution retirement account balance for those ages 55 to 64 is about $76,000.18 Median household income for that age group is $56,575. The numbers suggest troublesome retirement prospects for many older Americans.

Most of the defined contribution savings come from 401(k) plans, which use pretax deductions from paychecks to accumulate savings tax-free until the money is withdrawn. The average balance in 401(k) plans in 2013 for all ages was $72,383, while the median balance was $18,433.19

In addition to these low levels of savings, many older Americans are entering retirement with higher amounts of debt. Pew’s research has found that among retirees born between 1928 and 1945, the so-called silent generation, more than half (56 percent) have debt, and 80 percent of baby boomers, many now entering retirement, have debt.20 Perhaps it is not surprising that half of elderly people who are single and one-third of elderly people in relationships die with less than $10,000 in assets.21 Analysts debate whether retirement prospects are as bad as these factors indicate,22 but the weight of the evidence points to significant problems for many Americans.

The average balance in 401(k) plans in 2013 for all ages was $72,383, while the median balance was $18,433.

State policymaker objectives

Pew analyzed all state legislation on retirement savings introduced from 2012 through 2015. The proposals to promote retirement savings for private sector employees generally share certain goals. Supporters want the state-sponsored programs for these employees to increase access to retirement savings opportunities for workers whose employers do not offer retirement plans. In addition, many proposals would bolster participation among workers who are unlikely to save enough on their own to ensure a financially secure retirement.23 For example, the Connecticut legislation that launched a study of retirement savings options states that a goal of the program would be to achieve an “increase in access to and enrollment in quality retirement plans.”

Sponsors of legislation also seek to reduce poverty among retirees so that they can support themselves without needing public assistance—spending that strains government budgets. The California Secure Choice statute, enacted in 2012, says that the “lack of sufficient retirement savings poses a significant threat to the state’s already strained social safety net programs and also threatens to undermine California’s fiscal stability and ongoing economic recovery.”24

Reforms also must be feasible and work in practice, so states should focus on operational details to ensure that the programs accomplish legislative objectives. That is particularly true for key elements of program design, such as ensuring that the processes for enrolling employees and transferring contributions are workable. State-sponsored programs also must be cost-effective and self-sustaining.25

In addition to limiting state legal liability, some laws have made clear that the state is not liable for any contracts or commitments made by the program,26 for the performance of investments, or for paying benefits to participants.27 For example, the Illinois Secure Choice legislation says that the state will provide investment options that generate returns on contributions and convert account balances to secure retirement “without incurring debt or liabilities to the State.”28

Finally, under some proposals, the state program would provide certain protections for workers and their assets. For example, Connecticut’s study legislation suggested setting a predetermined and guaranteed rate of return on assets, as well as an annuitized benefit, but the study commission did not recommend such a guarantee.29 Several states also say their programs should “ensure the portability of benefits.”30

Three approaches

States generally have taken one of three approaches to bolstering retirement savings by private sector workers. Each approach reflects a major structural choice for policymakers. A state can sponsor and administer a plan within the structure of ERISA, the federal law that governs pensions; it can work within the current voluntary employer-based system without sponsoring a state plan; or it can create a state-based plan that may not be subject to the federal pension law.

Option 1: State-sponsored ERISA plan

Legislators designing a state retirement program for private sector employees need to decide whether it will be governed by ERISA. (See Appendix for more on ERISA.) In general, ERISA provides important protections for those who participate in private sector plans and their beneficiaries, but it also imposes regulatory requirements and responsibilities on employers. These include reporting and disclosure rules as well as fiduciary responsibilities that require plan sponsors and providers who have control over plan assets to act in the best interests of plan participants. ERISA also sets limitations on the amount of benefits that owners or highly compensated employees can receive from the plan.

Plans for public sector employees are exempt from ERISA. IRAs typically are not subject to ERISA when they are set up, funded, and controlled by an individual and not the employer. But a state law that requires participating employers to set up an employee retirement plan might be subject to or pre-empted by ERISA, depending on how courts interpret the plan design, although states may be able to provide incentives for employer and employee contributions.

Prototype and multiple employer plans

Recent guidance from the U.S. Department of Labor made clear that states can operate ERISA-governed plans that cover many private sector employers.31 These can be either prototype plans or multiple employer plans (MEPs). With a prototype plan, a state would offer a standard plan design for a 401(k) or other retirement plan to employers, which would choose among options, such as contribution rates, according to their needs.

Each employer that adopts the prototype is sponsoring an ERISA plan. Individual employers would assume the same fiduciary obligations associated with sponsorship of any ERISA-covered plan, but a state or a designated third party would assume responsibility for most administrative and asset management functions.

As a single plan that covers a group of unrelated employers, a MEP also falls under ERISA. A state that sponsors a MEP would be the plan fiduciary in terms of operating the plan, communicating with employees, selecting service providers, paying benefits, and performing other plan services.32

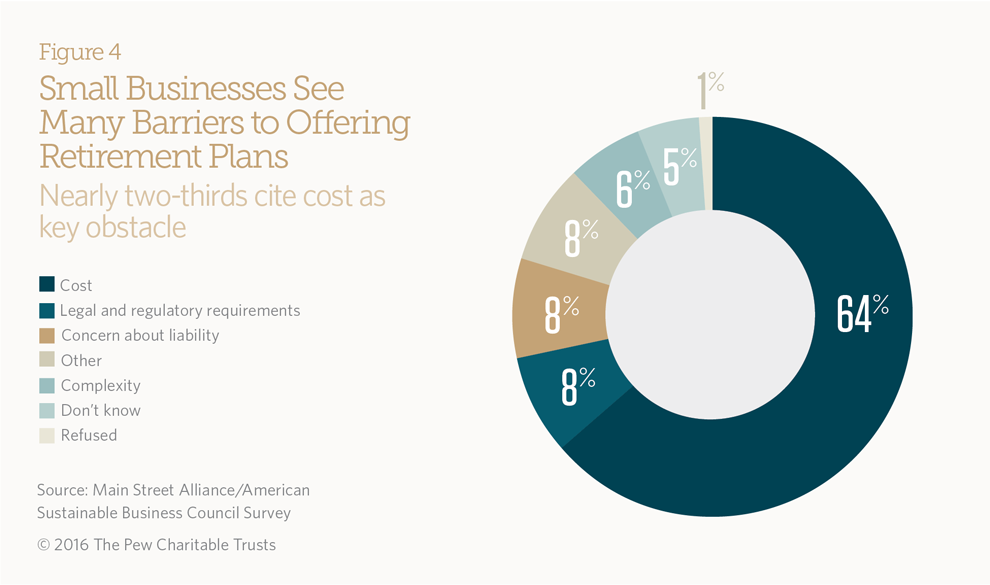

Prototype plans and MEPs can both achieve efficiencies and economies of scale that help reduce costs. Employers that do not offer retirement savings plans to their employees often cite concerns about costs, legal and regulatory requirements, and liability issues. In a 2013 survey of small businesses with and without retirement plans conducted by the Main Street Alliance/American Sustainable Business Council, 64 percent cited cost as the largest barrier to offering a retirement savings plan. (Figure 4 provides the range of responses.)33 Another survey, conducted in 2014 by the Small Business Majority in Illinois, found that of the 70 percent of small businesses that do not offer plans, 27 percent cited a lack of administrative capacity and 14 percent cited cost as reasons for doing so.34

MEPs can benefit employers and employees because they combine contributions from many workplaces and investment returns in a single asset pool, although participants have individual accounts. While ERISA applies to MEPs, only one ERISA-required annual report must be filed for the whole plan, instead of multiple reports on behalf of each participating employer. In addition, the fiduciary duty is greatly reduced for employers.35 As part of its effort to facilitate state consideration of MEPs, the Department of Labor has advised that state-sponsored MEPs can be exempted from some of the requirements that apply to similar private sector multi-employer plans.36

Prototype Example: Massachusetts CORE

The Massachusetts Connecting Organizations to Retirement (CORE) program was designed to be a voluntary defined contribution program for small nonprofit organizations. In 2012, Massachusetts enacted legislation that authorized creation of a voluntary qualified retirement plan that could be used by nonprofit organizations with a maximum of 20 workers.37 Each participating employer maintains an ERISA-covered defined contribution plan that is made more affordable because the state treasurer administers contributions and investments.38 Employers that participate must operate their plans in compliance with the Internal Revenue Code and ERISA. The state treasurer can contract with individuals or companies to help design, administer, and provide investment options. The legislation also created a “not-for-profit defined contribution committee” to help the treasurer develop general program policy and to provide technical advice.39

Option 2: Non-ERISA state plan

Some legislators fear that ERISA would require the state, the plan, or participating employers to take on too many responsibilities or be subjected to unwanted liability. Many employers that do not offer retirement plans find it too expensive to do so under ERISA or find ERISA to be overly burdensome.

Most legislation on state-sponsored retirement plans for the private sector is being designed to avoid ERISA. For a state plan to avoid falling under ERISA, the employer’s role must be minimal. The federal Department of Labor provides legal guidance to employers describing the specific arrangements needed to keep a plan from falling under ERISA as well as the tasks an employer can perform without converting the arrangement to an ERISA- covered plan.40

For example, the Labor Department has long provided a safe harbor in which an IRA program funded by payroll deductions is not an ERISA plan if the following conditions are met:

- The employer does not make any contributions.

- Employee participation is “completely voluntary.”

- Employer involvement is minimal and limited to providing information about the program to employees without endorsing the program.

- The employer is not paid for offering the program.41

In response to a directive from President Barack Obama, the Labor Department proposed modifying this safe harbor somewhat when an employer is participating in a state-sponsored IRA plan.42 To create a state-sponsored retirement program with automatic enrollment that is not subject to ERISA, state legislators must make sure that employer responsibilities fall within the original Labor Department safe harbor43 or the newly proposed safe harbor for state-sponsored IRA plans.44

Example: Illinois Secure Choice

In January 2015, Illinois enacted the Illinois Secure Choice Saving Programs Act.45 The program will use automatic enrollment and payroll deduction contributions to fund Roth IRAs46 and is slated to be implemented by June 1, 2017.47

Illinois has made clear it will have no liability for payment of retirement savings benefits, and the program is required to become self-sufficient. The law says that members of the Illinois Secure Choice Board and those they hire have the fiduciary duty to act solely in the interest of plan participants and beneficiaries.48 They face no liability for losses from investments selected, unless the liability arises out of a breach of fiduciary duty.49

Once the law is implemented, businesses and nonprofit employers in operation for at least two years with at least 25 qualified employees and no retirement plans will be required to participate.50 The Illinois legislation would let other small employers that do not offer a retirement plan participate voluntarily, but the Labor Department’s proposed rule would prohibit voluntary employer participation in order to keep employer involvement to a minimum and to avoid triggering ERISA coverage.51 Meanwhile, Illinois law would permit workers at nonparticipating employers to enroll in the program, but guidance from the Labor Department may not permit such participation.52

Eligible employees will be enrolled in the plan unless they sign a document opting out. Participating employees can set the amount to be contributed from each paycheck and can change that level at any time.53 If a worker does not select an amount to contribute, the program sets the level at 3 percent of wages.54 The program will maintain individual Roth IRA accounts for accounting purposes,55 but contributions will be pooled to obtain economies of scale.56 Participating employers have no liability for program design, administration, investments, investment performance, or benefits paid to employees participating in the plan.57

Option 3: Work within the voluntary employer-based system

The third broad approach involves the state working within the existing private sector retirement system as a facilitator and educator to encourage—but not require—businesses to adopt ERISA-covered retirement plans. Many business owners and executives may not be familiar with retirement plan options, and providers often find it difficult to reach small businesses with product offerings. In a 2014 survey of Illinois businesses conducted by the Small Business Majority, 10 percent of the business owners cited concerns over how to choose a plan provider as a reason for not offering a plan.58 In addition, surveys show that many employees have not done much retirement planning and often do not have high levels of financial literacy. A state could help bridge these gaps by conducting education campaigns and by using websites and other communication technologies to bring together employers, financial service providers, and employees.

Example: Washington State Marketplace

In 2015, Washington created the state’s Small Business Retirement Marketplace,59 which will be designed and managed through the state Department of Commerce.60 Employers with fewer than 100 workers, as well as the self-employed and sole proprietors,61 will be eligible, though participation will be voluntary for employers and workers. The director will promote the program through a website and electronic marketing materials.62

Under the legislation, the marketplace must offer a variety of investment options and determine whether financial services firms are qualified to take part in the system. Such firms must offer a minimum of two choices: a balanced fund and a fund with asset allocations and maturities that coincide with a worker’s expected date of retirement, known as a target date fund. The marketplace also must offer the federal myRA, a new savings program for workers without a plan at their workplace. (See the Appendix for a more detailed discussion of the myRA.) Approved plans must comply with federal law for retirement plans.63

The director must identify incentives for employer and employee participation. This includes highlighting federal and state tax credits and benefits for employers and employees who participate in retirement plans. In addition, the director may use public and private funds to provide incentive payments to eligible employers to enroll in the marketplace if those funds are devoted to that purpose.64

Plan design considerations

State policymakers can use a variety of tools—either in the enabling legislation or in the program implementation—for incorporating their objectives into the design of a state-sponsored retirement program for private sector employees. For example, they must decide the requirements for employer participation, worker enrollment, investment and protection of contributions, program administration, and the obligations that will be taken on by the state. This plan design discussion covers three broad topics: critical issues for employers, issues affecting employees, and state concerns and overall management.

Critical issues for employers

Employer participation: Voluntary or required?

Several states have considered legislation that would create state-sponsored retirement programs for private sector workers while allowing employers to choose whether to participate in the programs. The Massachusetts and Washington programs encourage but do not require employers to adopt an employee retirement plan covered by ERISA. Either type of voluntary program might appeal to employers that have not previously offered retirement plans because of the cost to create or maintain them.

A critical question is whether a voluntary state-sponsored retirement program will increase retirement savings. Employers in the private sector are not required to provide retirement plans, and the data show that many choose not to. Nationally, 58 percent of full-time, full-year private sector workers have access to a retirement plan at their workplace. That drops to just 22 percent at firms with fewer than 10 employees.65

These numbers suggest that although some employers might participate in a voluntary program like a marketplace exchange, there may not be enough participation to generate significant increases in coverage. While it is unclear whether a marketplace exchange would work, a well-publicized and accessible web-based platform for employers to connect with service providers could encourage some businesses to adopt retirement savings plans.

Nationally, 58 percent of full-time, full- year private sector workers have access to a retirement plan at their workplace. That drops to just 22 percent at firms with fewer than 10 employees.

In addition, state policymakers will want to consider whether adoption of a program such as the Massachusetts plan for nonprofit organizations could encourage employers that have retirement plans to drop them to participate in the state program. A switch from an employer-sponsored plan to a state plan could result in reduced benefits for employees and possible additional costs for the state program. Some proposals and laws that require a market analysis or study—including those that require mandatory participation by employers—direct those conducting the studies to consider ways to encourage employers to keep or adopt their own plans.66

Requiring some level of employer participation—through the automatic enrollment of employees and payroll deductions with the ability to opt out, for example—is recognized as an effective way to increase both access and participation.

Consequently, most legislative proposals require or contemplate mandatory participation by employers of a specific size that do not offer retirement savings plans.67 Legislators who prefer not to require employer participation will probably want to assess how to design a program that employers and workers in the state would willingly join. Apart from tax or other incentives, the program would need to demonstrate that it would be cost-effective for employers and provide superior service for employees.

Lawmakers must determine which employers are subject to the program. For example, the Illinois law requires employers with at least 25 workers to participate in the state-sponsored retirement program if they do not offer their own plan or payroll deduction program. In contrast, the California Secure Choice legislation requires participation by private sector employers with at least five employees.

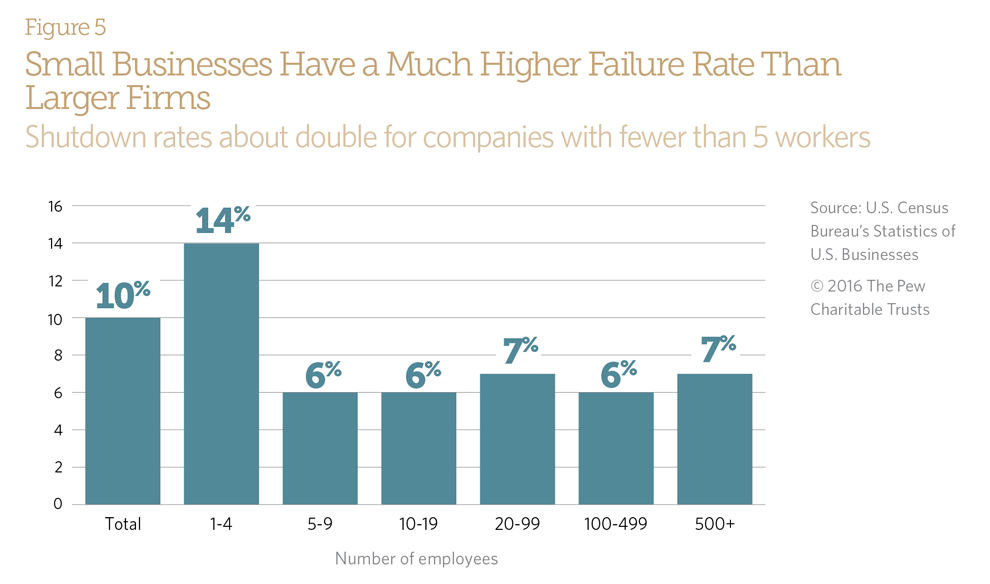

These thresholds for participation may reflect the fear that the costs of participation in a state-run retirement savings program could harm the profitability or viability of the smallest firms. According to the Census Bureau’s Statistics of U.S. Businesses, 14 percent of businesses with one to four employees did not survive over a two-year period. That’s more than double the 6 to 7 percent exit rate for larger entities.68 Figure 5 shows the shutdown rates for firms by employment size.

In addition, any law should clearly identify which employees are covered and how the law applies to them. For example, it should be explicit as to whether part-time workers who cannot participate in an employer plan would be eligible for the state plan.

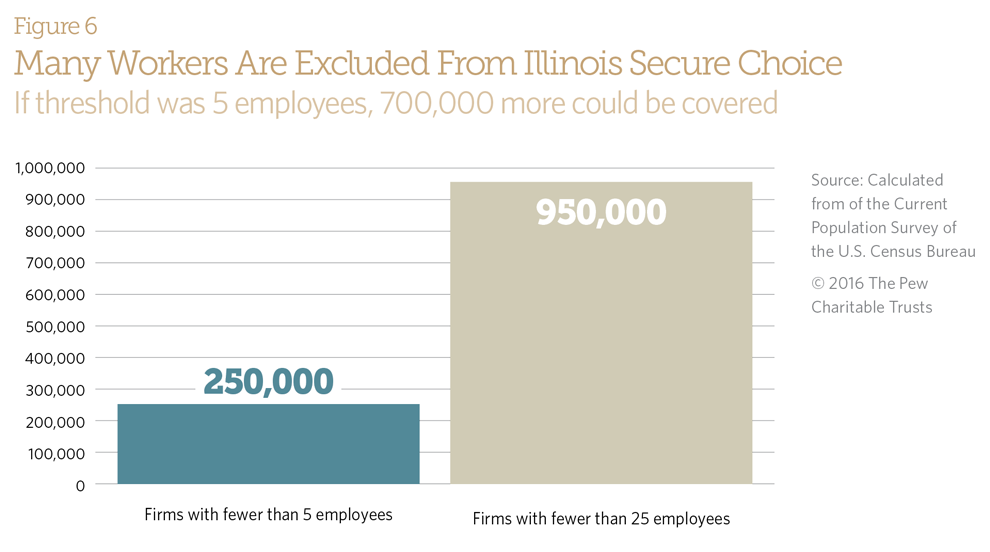

The size threshold has a significant impact on the overall number of workers covered, as shown in Figure 6. The Illinois legislation will not affect the roughly 950,000 people who work for firms with 24 or fewer employees. If the California threshold of at least five workers were applied in Illinois, an additional 700,000 people could be covered, although some may already be eligible for existing plans.69

Employer responsibilities

Under many of these reforms, employers are responsible for enrolling their workers. When crafting programs, state policymakers must set rules for the length and frequency of enrollment periods. Should enrollment last for one week or one month or be open-ended? Should open enrollment occur every year or every other? These are important questions for employers, who must provide communication materials and deal with changes in employee decisions. They will likely need to respond to questions from their workers.

Some legislative proposals would require participating employers to hold periodic open enrollment periods for new hires and employees who previously opted out of the plan.70 Under the Illinois law, the open enrollment will occur once a year, permitting employees who might not have enrolled earlier to do so. The California law says that once the Secure Choice program is fully implemented, employers must hold an open enrollment period at least once every two years, during which they must automatically re-enroll employees who previously opted out or ended their participation. The workers then must opt out again.71

Policymakers should consider the cost and administrative impact of an open enrollment period on employers, especially small businesses, and whether other approaches would be more cost-effective or less burdensome to administer. For example, they might limit the duration or frequency of enrollment periods after initial implementation or use web-based or mobile tools to allow participants to make changes without involving their employer.

Employers probably will communicate informally with employees about the programs and their options. For example, the Illinois law calls for employers to distribute materials developed by the state’s retirement security board to workers.72 Employers are often the point of contact for benefits-related questions, so they can expect employees to ask additional questions about the program, such as contributions, investments, and distributions. States might consider how best to ensure communication between the program and participating employees to balance the efficiency of a workplace-based program with the burdens placed on the employer.

Employer liability

Proposals to establish state-sponsored retirement programs that require employer participation strictly limit the liability of participating employers. In general, policymakers eliminate employer liability for an employee’s decision whether to participate, as well as investment performance, plan design, and retirement income paid to participants.73 These provisions reflect the fact that employers in state-sponsored payroll-deduction-only programs have no control over such matters. These liability limitations would not apply to employers who set up a traditional ERISA-qualified employee retirement plan, because they would be subject to the liability described in the federal law.

Beyond ERISA liability concerns, most state initiatives do not provide explicit sanctions for employers that do not perform their duties under the program, although other state laws, such as those dealing with wage theft, may provide protections.74 In contrast, Connecticut’s study legislation envisions allowing the state to take action

against employers that do not meet their obligations.75 Under the Illinois law, employers can face penalties if they fail to enroll their employees in the program.76 The law does not set penalties for failing to perform other duties, such as forwarding payroll deduction contributions to the program, although existing state labor law may allow penalties in these cases. Still, the state board administering the program appears to have enforcement authority.77

Issues affecting employees

Enrollment rules

The legislative proposals uniformly say that employee participation in a state-sponsored retirement program should be voluntary. Still, proponents intend these programs to significantly increase the number of private sector employees saving for financially secure retirements.

Research in behavioral economics has consistently shown that even minor obligations, such as making a phone call or filling in a form, can keep workers from enrolling in a retirement plan.78 Consequently, research and industry experience show that automatic enrollment—with the ability to complete a form to opt out—will increase the number of employees who participate in a retirement plan.79 For example, data from Vanguard’s database of 4,700 plan sponsors and 3.9 million participants show that plans with automatic enrollment have a participation rate of 89 percent, compared with 61 percent for plans without automatic enrollment. These effects, though, are somewhat weaker for lower-income workers and workers in small firms, both of which are the focus of state retirement savings proposals.80

Because of these findings, most legislation on state-sponsored plans for private sector employees, including the California, Connecticut, Oregon, and Illinois laws, require employers to automatically enroll employees who do not opt out.81 Whether automatic enrollment would work as well in the state programs is unknown. Many employers that would be covered under these programs are relatively small, with lower-income workforces that may be more likely to opt out. Research also suggests that contribution levels are lower for participants who are enrolled automatically than for those who join a plan voluntarily.82

Types of employees covered

States considering legislation must decide which employees would be covered. Most proposals do not have detailed standards, such as full- or part-time status, for determining eligibility of employees to participate in state plans. State legislation typically defines eligible employees as those 18 or older who work for an eligible employer. A few states define eligible employees as workers who earn wages subject to state income taxes.83

Still, some legislation includes qualifiers that limit the definition of an eligible employee. For example:

- A number of states exclude those covered by certain federal labor laws or labor contracts or who are otherwise not subject to state legislative power under federal law.84

- Two proposals in Massachusetts suggest different approaches to defining employees eligible to enroll in a state-run retirement savings plan other than the CORE program for nonprofit organizations. One bill (H. 924) defines eligible employees as those who work 750 hours in a calendar year;85 the other (H. 939) requires an employee to have wages subject to state taxation.86

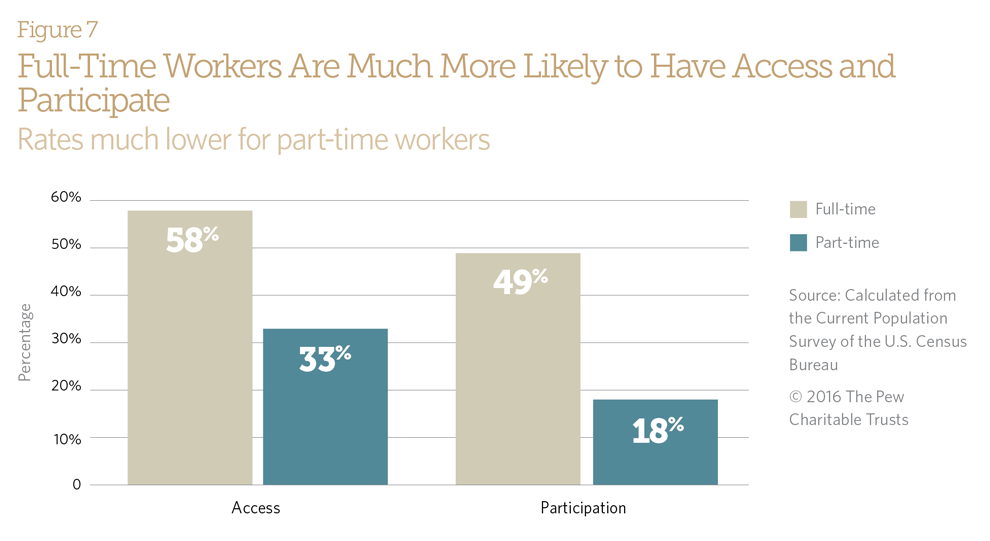

How an employee is defined in these programs would have significant effects on access and participation. According to the Labor Department’s Bureau of Labor Statistics, 33 percent of the workforce is part time, part year, or a combination of both. Another 19 percent of workers are considered part time, part year, because they work less than 35 hours a week.87 Figure 7 provides retirement access and participation by full-time or part-time status: Just 33 percent of part-time, full-year workers have access to a workplace retirement plan, and 17 percent participate in such a plan. This is much lower than the rates for full-time workers. (See Figure 7.)88

In addition, more than 10 million people work as independent contractors, according to the Labor Department,89 and would not be covered by state retirement savings proposals.

Contributions

Most statewide retirement savings legislation requires employers to withhold employee contributions from pay at a default rate.90 Employees can choose to make contributions higher or lower than the default rate or opt out altogether.

The California and Illinois laws provide for a default contribution rate of 3 percent if an employee does not choose a percentage.91 California also requires its governing board to determine a minimum and a maximum rate of contribution.92 The Oregon and Connecticut laws recommend that their boards consider a default rate of contribution; the Connecticut feasibility study, however, proposed a 6 percent contribution rate.93 California and Oregon both recommend that the default rate be changed over time.94 California, Connecticut, Oregon, and Illinois would all allow participants to determine or change their contribution rates.95

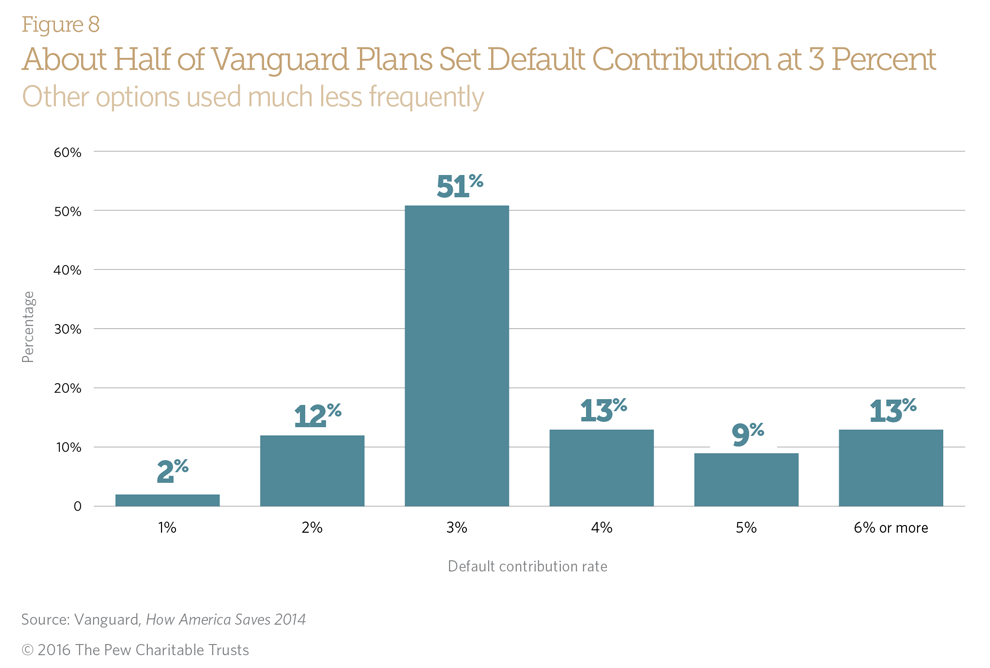

The federal Pension Protection Act of 2006 allowed workers to be automatically enrolled and to contribute at a default rate unless they changed that percentage or opted out. Data collected from private sector plans since the law took effect provide insight into the decisions about default contribution rates. In a 2014 report about its automatic enrollment plans, Vanguard found that about half of all company plans that use automatic enrollment—51 percent—have a default rate of 3 percent of pay. Fourteen percent set the default at 1 or 2 percent, while 35 percent set the default rate at 4 percent or more.96 Figure 8 below shows the range of default rates.

The level of the default contributions plays a role in how much a worker can save for retirement. According to an actuarial analysis, workers who saved 3 to 6 percent throughout their careers—with no employer match—would not have enough retirement income for their expected lifetimes.97 Still, these assets would supplement Social Security benefits for most Americans, and they would probably provide a cushion for financial shocks in old age.

States also have considered allowing voluntary employer contributions,98 which would be a good way to encourage more employees to participate and build their savings for retirement. However, the November 2015 Department of Labor proposed rule makes clear that employers could not voluntarily contribute to a state- sponsored payroll deduction IRA program. Voluntary employer contributions could be made to a state-sponsored MEP or prototype plan. Minnesota, for example, would permit employers to contribute to an ERISA-covered portion of their retirement savings program.99

Investing contributions and protecting savings

In typical defined contribution plans, individuals invest their retirement plan contributions in a range of options, or the contributions are pooled and managed by investment professionals for the participants. The California, Minnesota, and Oregon programs would pool the contributions so they can be invested by professionals.100 Illinois’ program will offer low-risk investment choices to participants and include design elements meant to preserve the safety of the contributions and provide a stable and low-risk rate of return.101

In participant-directed plans, participants get their own accounts and are responsible for managing their investments. Pooled investment plans have a single trust account in which contributions are commingled and are usually managed by a third-party administrator. Participants in pooled investment plans do not manage their accounts or direct their investments, so costly enrollment meetings, participant education, and individualized advice are not normally provided.

Pooled investment plans generally cost less to manage and maintain because fewer participant services are needed. Investment management in such plans can be offered at a reduced fee, and because the money is in a single account, the cost of managing assets is lower than in participant-directed plans.102

Moreover, a pooled investment plan with a professionally managed investment portfolio may achieve better investment results. Even with the best advice, those in participant-directed plans still have to follow through and make the right choices.

States also must consider how best to oversee the operation of the plans. In Illinois, the enabling legislation requires the Secure Choice Board to conduct a review of the performance of the investment funds, including fees and customer performance, every four years.103 Fund management professionals suggest reviewing investment returns and expense ratios at least every two to three years, however.104

Some proposals try to minimize participants’ financial risk and safeguard their investments and returns.105 California, for example, will provide a guaranteed annual rate of return set by the Secure Choice Board if it is financially feasible. A gain and loss account would be established to smooth out interest contributions when plan investments do not generate the returns sufficient to meet the stated interest rate.106 Although such guarantee provisions provide important protections against investment risk and volatility, they can be controversial because of the state’s involvement in mandating a return and can create new complications. They also can be expensive and difficult to understand. States must consider the potential effect on public finances. Perhaps reflecting these concerns, most state proposals do not include provisions regarding guarantees.

Tax and financial impacts

Most state proposals seek to ensure that savings will be tax deferred under the Internal Revenue Code. However, many participants probably would be lower-income workers who would not benefit much from deferring taxes on the contributions. In addition, many programs do not explicitly provide financial incentives to participate, such as employer matching contributions or refundable tax credits.

Some states, such as Illinois,107 are using Roth IRAs to allow workers to contribute after-tax money. That could help those who might have a higher tax rate in the future. Moreover, withdrawals of contributions from a Roth IRA are tax-free in certain circumstances, which could appeal to lower-income workers. Earnings on contributions would still be taxable. One complicating factor is that participants cannot roll over Roth IRA accounts into employer-provided retirement plans if they change jobs.

Employee withdrawals

Of the laws already enacted, California’s provides the most information on possible withdrawals. Workers would receive an information packet that describes the process for withdrawal of retirement savings.108 The board conducting the feasibility studies required by the legislation recommended in its report, released in February 2016, that the program limit pre-retirement withdrawals to hardship requests and suggested that the board consider an annuity (lifetime income) option as the plan developed.109

The Illinois law requires the state board to set rules for withdrawals that maximize participants’ financial security in retirement.110 Under the Connecticut program, workers can receive annuitized benefits, lump sum payouts on retirement, spousal benefits, and death benefits for designated beneficiaries. Many of the proposals do not discuss pre- or post-retirement withdrawals.

The Labor Department’s proposed rule on payroll deduction IRA plans would not allow state programs to limit withdrawals otherwise permitted under federal law, but this exclusion could be changed when the rule is finalized.111

As a point of reference, participants in private sector ERISA-covered plans have several options for withdrawing their savings, depending on the timing of or reason for the withdrawal. For example:

- In 2010, more than 25 percent of households with defined contribution plans collectively withdrew more than $70 billion from retirement plan balances for nonretirement spending, according to an analysis of data from the Federal Reserve’s Survey of Consumer Finances and the Survey of Income and Program Participation by HelloWallet, a web and mobile application that provides benefits information to workers.112

- Participants in some plans can take loans from their accounts. In 2011, 59 percent of 401(k) plans offered a loan plan, 89 percent of plan participants were eligible to take a loan, and 21 percent of those eligible to take loans had an outstanding loan balance.113 The average loan balance was $7,027, with a median balance of $3,785.114

- Based on 2013 data from Vanguard’s client base, about 4 percent of participants withdrew about 1 percent of total assets, even though they did not leave their jobs or retire.115

- About 30 percent of assets withdrawn were considered hardship withdrawals, such as medical emergencies, while the remaining withdrawals were for other purposes.116

Typically, when participants leave their employer or retire, they withdraw plan funds to use in any way they see fit, roll their account to a new plan or IRA, or leave their account where it is. How they handle these changes before retirement will have tax consequences. Vanguard’s analysis of the plans it manages shows that 49 percent of those who left jobs kept the accounts in their plans, 22 percent took lump sum payments, and 22 percent rolled their accounts into a new plan or IRA.117

Portability of benefits

Most state proposals refer to the portability of savings generally, but this vague concept usually needs to be clarified by state boards or study committees. Most bills provide no guidance. Portability usually refers to the ability of workers to continue to save in a single account even if they change jobs. That is hard to do with benefits from a defined benefit plan, except when they are converted into a lump sum. On the other hand,

defined contribution balances can be transferred to a new employer plan or an IRA when a worker changes jobs.

In state-level retirement savings programs, workers could presumably maintain their accounts with the state if they changed jobs, but it is not clear if portability would mean that savings accounts could be transferred to a different state, to an IRA, or to an ERISA plan sponsored by a new employer. As noted above, however, for tax reasons participants cannot roll over their Roth IRA accounts into an employer-provided retirement plan if they change jobs.

State concerns and overall management

Program administration and governance

Many statewide retirement savings proposals are designed so that the plans will not be regulated by ERISA or be considered public sector retirement plans. And that raises important governance issues. Still, the rules for administering plans for either the public or private sectors include requirements for ensuring the integrity of funds and investments, meeting reporting and disclosure responsibilities, and ensuring transparency and accountability.

Regardless of whether they are covered by ERISA, state proposals have many governance provisions in common. Most would appoint a state officer or agency to run the program. For example, the Massachusetts CORE program is run by the state treasurer, and a “not-for-profit defined contribution committee” in the treasurer’s office helps develop general policy and provides technical advice.118 Typically, a state creates a board with appointed members representing different branches of government or sectors of society. Under the California law, the Secure Choice board is part of the state government; it has administrative and managerial duties and acts as trustee for the state’s plan.119 The Illinois board is a state agency made up of legislative and executive appointees who will oversee the program.120

The powers given to the boards differ and are typically spelled out in the legislation. In California, the legislation says that the board will be the ultimate plan administrator, though it can hire a third-party administrator. The board must approve an investment management entity but retains certain management duties. For example, every year the board must prepare and adopt a written statement of investment policy.121

In Illinois, board members and the investment managers they hire or contract with must carry out their duties only in the interest of the plan participants and beneficiaries.122 In California, the board has to submit an annual audited financial report that has been prepared by an independent certified public accountant. The board also must disclose full details about program operations and provide periodic reports to participating employers and employees as well.123 More generally, states can require service providers such as investment managers to issue regular reports so they can properly oversee management.124

Paying for the program

State proposals typically require state-affiliated retirement savings programs to be cost-effective and sustainable. In some cases, states provide money for feasibility studies and startup costs, but virtually all programs are meant to be self-sustaining.

For example, under Illinois law, the state can pay administrative costs associated with creation and management of the program until it becomes self-sufficient. The law calls for the program to repay the state for startup costs. The state also requires that maximum annual administrative expenses not exceed 0.75 percent of the total trust balance.125 Administrative fees pay board expenses and are used to repay the state for any startup costs.

States that are studying options to encourage private sector retirement savings are looking at the costs of various plan designs. The Minnesota law, for example, says its report should include the projected expenses of different plan designs and the fees that would be needed to cover these costs as a percentage of average daily assets.126

State liability

Most of the legislation enacted makes clear that states cannot be held liable for investment earnings or plan losses. The Oregon law says that that the state task force cannot recommend a plan or use of an investment product that could create any state liability or obligation for payment.127 The Connecticut law says the state has no liability for any obligation incurred by the plan.128 California’s law also prohibits state liability and takes an additional step to ensure that the state will not be required to financially support the program by requiring the state to carry insurance or some other funding mechanism to protect the value of individual accounts.129 In

Minnesota, the expected retirement savings plan report must examine options to protect the state from liability and to manage risk to the principal.130

Policy implications and trade-offs

Many Americans are not saving enough for a secure retirement, and this savings shortfall could have significant impacts on future retirees and state budgets. To address this, several states have enacted legislation to start state-sponsored retirement plans for private sector employees; others are considering similar actions. Lawmakers who support these plans believe that state-sponsored retirement programs for private sector employees are necessary and feasible.131

To date, the most common approach is a savings program in which many employers that do not currently offer retirement savings plans are required to automatically enroll their employees.

States approach the issue of retirement savings differently, reflecting that there are many policy choices. Still, the state proposals generally have three goals in common:

- Increasing retirement savings and security for workers.

- Minimizing administrative and cost burdens for small employers.

- Managing legal and financial risk for the state.

Each policy choice can create conflict among these broad goals and require trade-offs. For example:

- Employee retirement security and employer burden.

- States considering legislation primarily want to boost retirement savings to ensure that residents have enough money for their post-work years. Increasing access to retirement savings plans has proved to be one of the most effective ways to achieve that goal. The vast majority of workers will participate if given a chance, so many state proposals require that most employers automatically enroll their employees. But some employers and advocates have raised concerns that steps such as automatic enrollment will put too much of a burden on small employers, hurt these businesses, and reduce jobs. Burdens on small employers could be reduced by technology or by making exceptions for very small employers, as was done in California.

- Most proposals require that employees be automatically enrolled, because data show that workers usually do not opt out and will save more than if they had to actively sign up for the plan. The administrative burden on employers can be reduced by requiring them to do no more than distribute state-produced communication materials and to set up and run the payroll process. Still, many workers naturally look to their employers for answers to pay and benefits questions, and employers may feel obligated to respond. Effective outreach campaigns and ongoing communications by the states would address worker questions and probably reduce the number opting out, as well as the burden on employers.

- State risks and employee retirement security

- Because research shows that employees do not usually opt out or change the default savings rate, states must carefully consider the level at which that rate should be set. Setting it too low could encourage employee participation but result in little savings for retirement. Small account balances also make plan administration less efficient. On the other hand, too high a rate could cause many workers with little discretionary income to opt out altogether. To address these concerns, states could set a modest default contribution rate, such as 3 percent of pay, with a gradual escalation until a maximum level is reached.

- ERISA, the federal law that governs pensions, provides protections against incompetence or outright malfeasance by employers or service providers. But such protections can be costly and burdensome for a plan sponsor. For proposals to establish and operate state-level retirement savings programs outside ERISA, program designers must balance these costs against the benefits of appropriate protections for workers. Although proposals often aim to limit employer liability, programs still need employer participation to collect contributions and distribute information. When states take on administrative duties such as processing contributions and withdrawals, concerns about malfeasance are reduced. Still, program governance must be designed to address possible malfeasance by state officials.

- States must also balance how much risk to take with investments while ensuring adequate returns. Low-risk investments protect the savings of participants who often have little financial sophistication, but savings may not grow sufficiently over time. For this reason, states have considered using a mix of low-risk and growth investments, such as a balanced or target date fund. Other proposals would provide some guarantee of return through insurance, a stated rate of interest, or some other method. However, most state proposals explicitly aim to keep costs down to protect taxpayers and do not require a guaranteed return. Added protections, in the form of a guaranteed return backed by the state or an insurance contract, could be costly for the state and could reduce investment returns.132

- To keep costs down, state-run retirement programs will need to achieve both scale and efficiencies in administering many small account balances. Many of the likely participants will be low- to moderate- income workers who, even with features such as automatic enrollment and escalation of contributions, will generate small balances. Managing hundreds of thousands or even millions of account balances could prove expensive. Still, the aggregate assets may generate sufficient returns to offset the administration costs. At the same time, a program that permits participants to choose among investment options can incur higher administrative costs, possibly without returns as good as if the investments were pooled. The federal Thrift Savings Plan (TSP) offers a hybrid approach that combines scale with limited investment offerings in order to achieve cost efficiencies, but such efficiencies may not be transferable to smaller investment pools at the state level.133

- State risks in general.

- A key question is whether states have the administrative and fiscal capacity to manage large savings programs, especially when existing federal savings options are considered. Is the federal government, which already regulates private sector and nonprofit employee benefit plans, better suited to create a program? Could MEPs within the ERISA framework be the right approach? Alternatively, states could craft their own statewide retirement savings programs by taking into account their experiences with employee benefit plans for public employees, with health care exchanges under the federal Affordable Care Act, or with 529 college savings plans.

Conclusion

Many Americans face the prospect of inadequate retirement savings, mainly because they lack access to an employer-sponsored retirement savings program. To address this issue, states are proposing a variety of reforms, and early indications are that they can feasibly implement retirement savings programs. Given the range of possible approaches, policymakers will have to identify and set priorities that balance competing risks and trade- offs. They also will need to consider the specific demographics of their states as they consider how to boost the retirement savings of their constituents. The states are arriving at individual conclusions on key issues, which will probably produce a range of approaches and program designs.

APPENDIX & TABLE

Appendix: Summary of federal regulation of retirement savings

Federal tax law

Individuals who participate in a tax-qualified employer retirement plan or a traditional individual retirement account (IRA)134 generally do not pay federal income tax on contributions until they are withdrawn. Investment earnings are not taxed as they accumulate in the account.135 Instead, individuals pay income tax on withdrawals in the year the funds are taken from the account. Those who withdraw money before what are known as permissible events such as retirement generally must pay a penalty, unless the withdrawal is for a reason permitted by federal tax law. These types of retirement savings accounts benefit those who expect that their tax rate will be lower after they retire.

Federal law sets different contribution limits for various types of plans. For example, 401(k) plan participants could contribute up to $18,000 in 2015, while IRA contributions were capped at $5,500 for the year (participants ages 50 and older can make additional contributions).136 However, federal law includes additional restrictions to prevent retirement plans from being used as tax shelters for upper-income people. Under federal law, administrators must ensure that contributions and account levels for upper-income participants and key personnel, such as managers and owners, are not disproportionately higher than for rank-and-file workers.

The tax law treats contributions and withdrawals from a Roth IRA differently. Contributions to these funds are taxed in the year they are made, but they can be withdrawn tax free at any time.137 Investment earnings accumulate in the Roth IRA tax free and are not taxed at all under certain conditions.138 If money is withdrawn early, in most cases the individual must pay taxes on the earnings and a penalty. Roth IRAs benefit those who may need to withdraw money tax free before they retire.

Federal law also provides incentives to save. Workers with modest incomes who participate in a retirement plan can receive a tax credit of up to $2,000. The amount depends on the individual’s income and tax filing status.139 Eligible workers can receive this credit even if they contributed to a traditional IRA and if the contributions were excluded from their taxable income.140

The Employee Retirement Income Security Act

The Employee Retirement Income Security Act (ERISA) is the federal law that regulates most private sector employee benefit plans, including retirement and health plans. ERISA protects plan participants through reporting and disclosure requirements. It also sets rules for certain transactions to avoid improper use of plan assets by plan sponsors or service providers.141 It requires plans to establish claims and appeal processes for participants and gives them the right, within limits, to sue for benefits or breaches of fiduciary duties. These rules generally are administered and enforced by the U.S. Department of Labor.142

ERISA sets standards for the behavior of individuals and companies responsible for managing the plan or its assets. It requires fiduciaries to perform their duties exclusively in the interests of the plan, its participants, and their beneficiaries. ERISA requires fiduciaries to act with the same level of care and diligence that knowledgeable, prudent people would use to manage their own financial affairs. Those responsible must avoid even the appearance of conflicts of interest that could benefit them or harm the plan.143

ERISA generally prevents or pre-empts states from creating laws that are “related to employee benefit plans, unless the plans are for public employees.”144 But states can make laws about arrangements that are not considered “employee benefit plans.” The Labor Department has interpreted the law to say that arrangements that permit payroll deduction and prompt transfer of voluntary employee contributions to IRA accounts are not “employee benefit plans” as long as the employer’s role remains minimal. The agency also says that role remains minimal even if the employer sets up the arrangement with a financial institution, encourages employees to save, and distributes information from the IRA provider. All materials distributed, however, must “clearly and prominently state, in language reasonably calculated to be understood by the average employee, that the IRA payroll deduction program is completely voluntary.”145

New federal proposals: The myRA initiative

In January 2014, President Barack Obama used his executive authority to direct the Treasury Department to create the myRA option to help Americans start saving for retirement.146 That December, the agency announced a program that will offer Roth IRAs invested in a risk-free Treasury security to workers whose employers do not sponsor plans. The Labor Department determined that myRA accounts were not “employee benefit plans” covered by ERISA.147

The myRA program will be voluntary for employers and employees. The accounts can have maximum balances of $15,000 and cannot be maintained for more than 30 years. When either of these limits is reached, savings will be transferred to a private sector Roth IRA, which has no maximum balance. On Nov. 4, 2015, the Treasury began offering myRAs on a nationwide basis.148

With its cap on savings, the myRA program is not designed to allow people to save enough for a financially secure retirement, but rather to start on that path. Although investment in myRA may be risk free from an investment risk perspective, state policymakers may want a program that offers eligible workers investment choices that could encourage greater participation in their program.

ENDNOTES

- Howard Iams, Irena Dushi, and Jules Lichtenstein, “Retirement Plan Coverage by Firm Size: An Update,” Social Security Bulletin 75, no. 2 (2015): 41–55, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2604116.

- Bureau of Labor Statistics, “Employee Benefits in the United States–March 2015” (July 25, 2015), http://www.bls.gov/news.release/pdf/ebs2.pdf, Table 1, 5–6.

- Since at least fiscal year 2011, the administration’s budget proposal has included provisions that would establish automatic workplace pensions that would require all but the smallest employers who do not offer retirement plans to enroll their employees in a direct deposit IRA account. See, for example, Office of Management and Budget, Budget of the U.S. Government Fiscal Year 2011, 99–103, https://www.gpo.gov/fdsys/pkg/BUDGET-2011-PER/pdf/BUDGET-2011-PER.pdf; and Office of Management and Budget, Fiscal Year 2016 Budget of the U.S. Government, 38, https://www.gpo.gov/fdsys/pkg/BUDGET-2016-BUD/pdf/BUDGET-2016-BUD.pdf.

- Jeffrey Stinson, “Offering State-Sponsored IRAs to Private-Sector Workers,” Stateline, The Pew Charitable Trusts (July 13, 2014), 3–5, http://www.pewtrusts.org/en/research-and-analysis/blogs/stateline/2014/07/18/offering-state-sponsored-iras-to-private-sector-workers; Elizabeth Olson, “Some States Look to Fill a Retirement Savings Gap,” The New York Times (July 4, 2014), http://www.nytimes.com/2014/07/05/your-money/some-states-look-to-fill-a-retirement-savings-gap.html?_r=0.

- Employee Benefits Research Institute, “Individual Retirement Account Balances, Contributions, and Rollovers, 2013; With Longitudinal Results 2010–2013: The EBRI IRA Database” (May 2015), EBRI issue brief no. 414, http://www.ebri.org/pdf/briefspdf/EBRI_IB_414.May15.IRAs.pdf.

- U.S. Government Accountability Office, “Federal Action Could Help State Efforts to Expand Private Sector Coverage,” GAO-15-556 (September 2015), http://www.gao.gov/products/GAO-15-556. A person is not legally required to wait until the end of the year to make an IRA contribution. Also, a number of financial service providers offer payroll deduction IRAs that permit periodic contributions throughout the year.

- The Pension Benefit Guaranty Corporation (PBGC) can help provide benefits when sponsoring employers cannot meet their plan obligations, but the benefits provided through the PBGC are usually lower than promised benefits.

- For a general overview, see Ethan Kra and Lane West, “Pension Risk and Your Retirement,” American Academy of Actuaries, (April 4, 2011), http://www.actuary.org/pdf/Hill_Briefing_Pension_Risk_and_Your_Retirement_April percent204_2011.pdf.

- U.S. Department of Labor, Private Pension Plan Bulletin Historical Tables and Graphs, Tables E1 and E8 (November 2012), http://www.dol.gov/ebsa/pdf/historicaltables.pdf. These figures refer to active employed and unemployed private sector workers. The same trends are seen using a different set of individuals. In terms of active workers, retirees, and beneficiaries, defined benefit plans covered 33 million Americans in 1975, and by 2012 they covered 39.8 million. The number of workers and beneficiaries covered by defined contribution plans increased from nearly 11.5 million in 1975 to more than 90 million in 2012 (Table E5). Total employment data and employment level of the civilian labor force are from the U.S. Department of Labor’s Bureau of Labor Statistics website, data series id LNS12000000, at http://www.bls.gov/data/#employment.

- Edward N. Wolff, The Transformation of the American Pension System (Kalamazoo, Michigan: W.E. Upjohn Institute for Employment Research, 2011), 89–102, http://research.upjohn.org/up_press/214.

- Alicia H. Munnell, Jean-Pierre Aubry, and Caroline V. Crawford, “How Has Shift to Defined Contribution Plans Affected Saving?” Center for Retirement Research at Boston College, no. 15-16 (September 2015), accessed Oct. 5, 2015, http://crr.bc.edu/wp-content/uploads/2015/09/IB_15-16.pdf.

- Wolff, The Transformation of the American Pension System, 57–70 and 211–253.

- Employee Benefit Research Institute, “Retirement Savings Shortfalls: Evidence from EBRI’s Retirement Security Projection Model,” issue brief no. 410 (February 2015), https://www.ebri.org/publications/ib/index.cfm?fa=ibDisp&content_id=5487. The results are for all U.S. households with a head 35 to 64 years old. Similarly, the National Institute on Retirement Security finds that the retirement savings deficit is between $6.8 trillion and $14.0 trillion. Nari Rhee, The Retirement Savings Crisis: Is It Worse Than We Think? National Institute on Retirement Security (June 2013), https://www.nirsonline.org/wp-content/uploads/2017/06/retirementsavingscrisis_final.pdf.

- Melissa M. Favreault, Richard W. Johnson, Karen E. Smith, and Sheila R. Zedlewski, “Boomers’ Retirement Income Prospects,” brief no. 34, Urban Institute (February 2012), http://www.urban.org/uploadedpdf/412490-boomers-retirement-income-prospects.pdf.

- Alicia H. Munnell, WenLiang Hou, and Anthony Webb, “NRRI Update Shows Half Still Falling Short,” issue brief no. 14-20, Center for Retirement Research at Boston College (December 2014), http://crr.bc.edu/wp-content/uploads/2014/12/IB_14-20-508.pdf. To produce the NRRI, a replacement rate, which is the projected retirement income as a percent of pre-retirement earnings, is calculated from the Survey of Consumer Finances, and that rate is compared against a benchmark rate defined as adequate. If households do not fall within 10 percent of the benchmark, they are classified as “at risk.”

- Tatjana Meschede, Laura Sullivan, and Thomas Shapiro, “The Crisis of Economic Insecurity for African-American and Latino Seniors,” Demos and the Institute on Assets & Social Policy (September 2011), http://www.demos.org/sites/default/files/publications/IASP%20Demos%20Senior%20of%20Color%20Brief%20September%202011.pdf.

- There are many such rules of thumb, including one from the MintLife website: Jim Drury, “How Can You Be Sure You Have Enough to Retire?” (Nov. 11, 2008), (http://www.mint.com/blog/finance-core/how-can-you-be-sure-you-have-enough-to-retire/). See also this blog post by Dan Ariely on the problems of such rules of thumb: “Asking the Right and Wrong Questions” (Aug. 30, 2011), http://danariely.com/2011/08/30/asking-the-right-and-wrong-questions/.

- EBRI presents 401(k) account balance data based on its EBRI/ICI 401(k) database, finding that in 2013 the average 401(k) plan in its database had a balance of $72,383 with a median account balance of $18,433. EBRI also finds higher account balances for older age groups. Fifty-two percent of accounts with less than $10,000 belong to participants in their 20s and 30s, while 60 percent of accounts with more than $100,000 belong to those in their 50s and 60s. Employee Benefits Research Institute, “401(k) Plan Asset Allocation, Account Balances, and Loan Activity in 2013,” issue brief no. 408 (December 2014), http://www.ebri.org/pdf/briefspdf/EBRI_IB_408_Dec14.401(k)-update.pdf. Vanguard’s analysis of its plans conducted in 2013 found the average account balance for defined contribution plans to be $101,650 with a median balance of $31,396. Those near retirement had larger account balances. Those ages 55-64 had an average account balance of $180,771. The median account balance for this age group was $76,381. Vanguard Group Inc., How America Saves 2014: A Report on Vanguard 2013 Defined Contribution Plan Data (June 2014), https://institutional.vanguard.com/iam/pdf/HAS14.pdf.

- Employee Employee Benefits Research Institute, “401(k) Plan Asset Allocation, Account Balances, and Loan Activity in 2013.” Employer-sponsored plans are but one possible source of retirement income. Nearly all older individuals receive Social Security benefits, and the average annual benefit is $15,400. Social Security Administration, “Monthly Statistical Snapshot, April 2015,” Table 2, https://www.ssa.gov/policy/docs/quickfacts/stat_snapshot/2015-04.html#table2

- The Pew Charitable Trusts, The Complex Story of American Debt (July 2015), http://www.pewtrusts.org/~/media/assets/2015/07/reach-of-debt-report_artfinal.pdf?la=en. In addition, the level of debt held by people in their 60s, as a share of their assets, increased from 10 percent in 1998 to 18 percent in 2010. Squared Away Blog, “More Carrying Debt Into Retirement,” Center for Retirement Research at Boston College (Aug. 22, 2013), http://squaredawayblog.bc.edu/squared-away/more-carrying-debt-into-retirement/.

- James M. Poterba, Steven F. Venti, and David A. Wise, “Were They Prepared for Retirement? Financial Status at Advanced Ages in the HRS and AHEAD Cohorts,” National Bureau of Economic Research working paper no. 17824 (February 2012), http://www.nber.org/papers/w17824.

- Michael D. Hurd and Susan Rohwedder, “Economic Preparation for Retirement,” National Bureau of Economic Research working paper no. 17203 (July 2011), http://www.nber.org/papers/w17203.

- Connecticut General Statutes, Chapter 574, Connecticut Retirement Security Board Public Retirement Plan, Section 31-414 (a) (2) (A) and (B), http://www.cga.ct.gov/2015/pub/chap_574.htm; Vermont Act No. 179, Section C. 108 (c) (1) (a) (i)-(vi), http://legislature.vermont.gov/assets/Documents/2014/Docs/ACTS/ACT179/ACT179%20As%20Enacted.pdf; and 2014 Minnesota Session Laws, Chapter 239, article 2, s10 (b) (1), (3), (7), and (d), https://www.revisor.mn.gov/laws/?year=2014&type=0&doctype=Chapter&id=239&format=.