Issuance of New Money Bonds Remains Low in Large U.S. Cities

© 2016 The Pew Charitable Trusts

© 2016 The Pew Charitable TrustsAn analysis by The Pew Charitable Trusts finds that borrowing in 30 large U.S. cities since the end of the Great Recession, which ran from late 2007 through mid-2009, was notably different from past recoveries.

Overview

Cities in the United States play a substantial role in funding critical infrastructure with investments in capital projects such as roads, bridges, schools, and libraries. For example, all local governments accounted for 35 percent of total highway and transit spending from 2008 through 2012.1 To pay for these projects, cities often sell bonds on the municipal market.

In the years following an economic downturn, governments commonly increase borrowing in order to take advantage of low interest rates and meet needs that may have been deferred because of tight budgets. However, an analysis by The Pew Charitable Trusts finds that borrowing in 30 large U.S. cities since the end of the Great Recession, which ran from late 2007 through mid-2009, was notably different from past recoveries. Through 2014—some five years after the national recession’s end—new money bond issuances across these cities dipped to their lowest point in over 20 years.

The large cities analyzed experienced significant drops in revenue during the recession, and the fiscal recovery that followed has proved uneven. Continuing strains on revenue may have led cities to move cautiously when considering new bond issuances and taking on additional debt service payments. Large funding gaps for pensions and what are known as Other Post-Employment Benefits, mostly retiree health benefits, also may have played a role in restraining borrowing in some local governments.

To understand borrowing activity in the 30 key cities, Pew analyzed inflation-adjusted calendar year data from the Thomson Reuters SDC Platinum database covering municipal issuances over the last three recessions and the recovery periods that followed. A review of the data finds that:

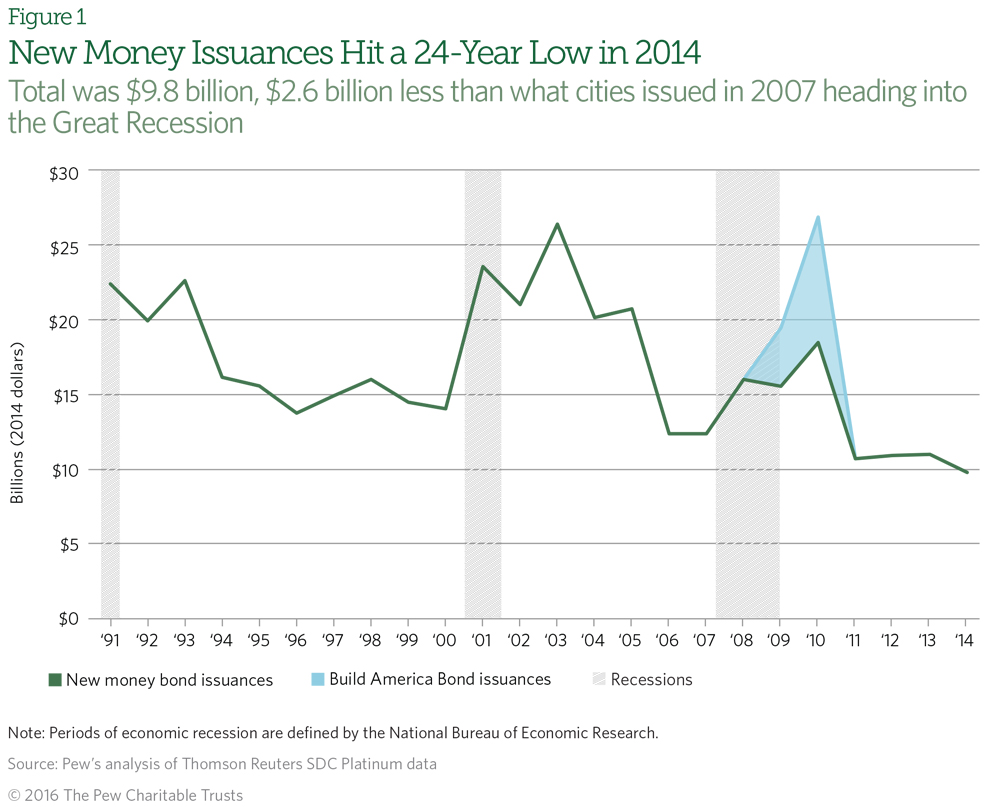

- In 2014, new money bond issuances in the 30 cities hit their lowest point in a 24-year period that started in 1991. This was contrary to usual borrowing patterns following economic downturns. Sales of new money bonds typically rise during a recovery as interest rates are often low, but from 2010 through 2014 total new money issuances for these cities averaged only $12.2 billion annually. These same cities issued an average of $17.6 billion a year in the five years following the 1990-91 recession and $20.1 billion a year in the five years after the 2001 recession.

- In 2014, the 30 cities analyzed issued $9.8 billion in new money bonds, compared with $12.4 billion in 2007 as the nation headed into the Great Recession. Not all issued new money bonds, but of those that did the amount sold varied widely, from $6.5 million in Tampa, Florida, to $1.5 billion in Chicago. Three cities alone, Chicago, Los Angeles, and Washington, accounted for over 40 percent of the total new money bond issuances in the 30 cities.

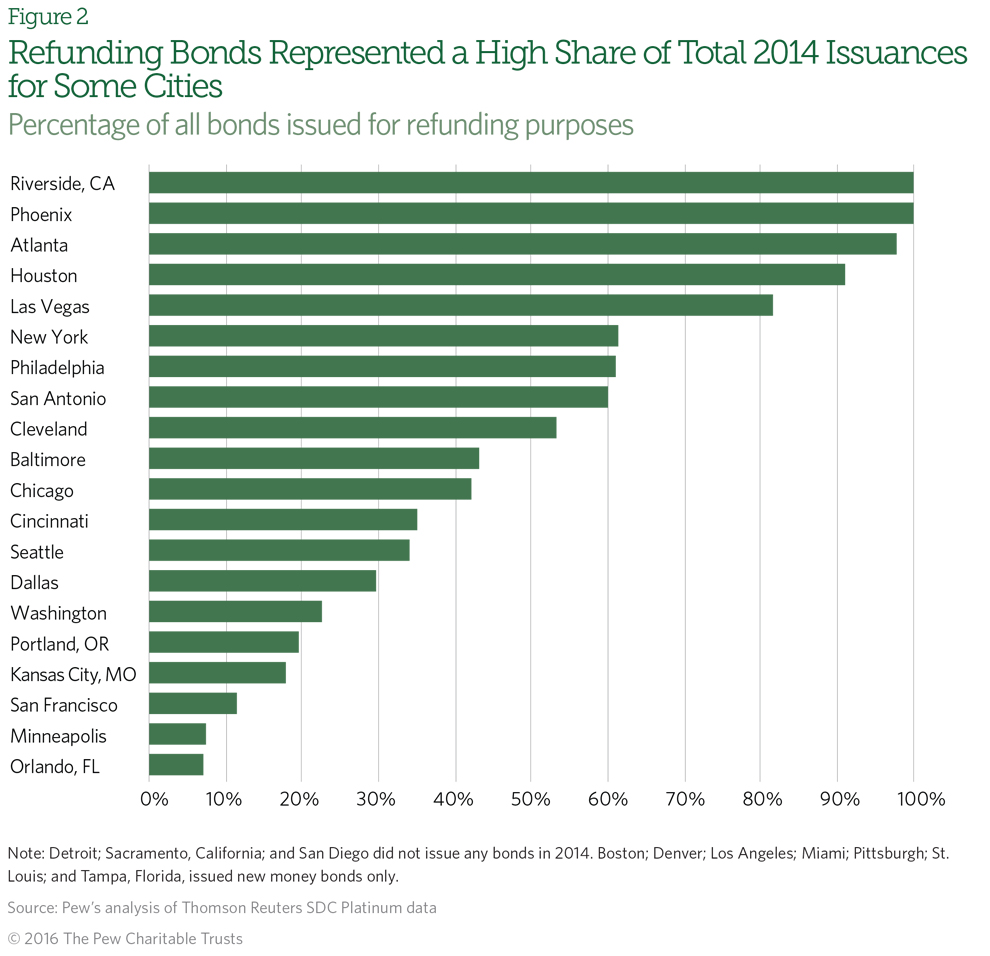

- Refinancing of bonds, known as refunding, totaled $9.2 billion in 2014—nearly half (49 percent) of total bonds issued.2 Since 2011, refunding has consistently exceeded 40 percent of bond issuances in the cities.

Methodology

For this brief, Pew examined 1991-2014 calendar year data from the Thomson Reuters SDC Platinum database on municipal bonds issued by the central city in the nation’s 30 largest metro areas according to the 2010 decennial census. Interest rates were collected from the Bond Buyer Indexes. The primary sources for revenue and spending data in this brief are Comprehensive Annual Financial Reports (CAFRs) for fiscal year 2007 through 2013. Pew researchers collected data from the statement of revenues and expenditures and the statistical section of each city’s CAFR for every year in the study period.

(For more information on the fiscal and economic health of large U.S. cities and to view previous research, visit Pew’s American cities project.)

2014 saw record low issuances

The market for new money bonds has been sluggish despite the economic recovery. In 2014, all municipal bond issuances nationwide totaled $337.5 billion, down $91.6 billion from 2007, the year the Great Recession started.3 The largest U.S. cities were no exception to this trend. In 2014, 30 of these cities issued only $9.8 billion in new debt, about 21 percent lower than issuances in 2007, and a record low for a 24-year period starting in 1991. Annual bond sales for 2011 through 2013 had been only marginally higher, reflecting a persistent trend.

Though new money issuances were low overall in 2014, there was considerable variation among cities that issued these bonds, reflecting their differing fiscal conditions, state contexts, and local priorities. For example:

- Chicago issued $1.5 billion in debt, the highest amount of any of the 30 cities. About half—$784 million—of the total was in airport revenue bonds for improvements to Chicago Midway International Airport.4 The remainder was distributed across a range of projects, including infrastructure and transportation improvements, grants to nonprofit organizations, and assistance for other governmental units and school districts.5

- Los Angeles issued $1.4 billion in new money bonds, the second-highest amount of the cities examined. Most of this new debt came from a single $1.36 billion tax and revenue anticipation note.6 Rather than borrowing for infrastructure or other capital improvements, the city used proceeds from this bond to smooth its revenue and prepay some pension contributions, resulting in $35 million in savings.7

- The third-highest issuer, Washington, borrowed $1.2 billion. Among the bonds issued were $350 million in 100-year maturity “century bonds” for improvements to outdated storm water and sewage infrastructure to reduce pollution of area waterways and improve water quality.8

- Several other cities made smaller issuances. For example, St. Louis sold $65 million in tax and revenue anticipation notes in order to improve city cash flow.9 In Pittsburgh’s first new money issuance since 2003, the city received $50 million in net proceeds to fund future capital projects such as roads and bridges.10

Five cities issued no new money bonds: Detroit; Sacramento, California; San Diego; Phoenix; and Riverside, California. Detroit had no bond sales in 2014 and was still in bankruptcy until December of that year.

Although bond sales from the 30 cities reached a historical low in 2014, increased issuances in the first part of 2015 by all state and local governments may indicate a growing confidence in their finances.11 Several of the cities analyzed in this brief represent examples of this increased willingness to borrow. In March 2015, Atlanta voters approved a $250 million bond sale to fund over 200 transportation and building improvement projects.12

By comparison, Atlanta issued only $50 million in new money bonds in 2013, and even less—just $21 million—in 2014. San Francisco voters also approved a bond, with nearly 75 percent voting in favor of issuing $310 million for affordable housing. This was the city’s first successful housing bond measure since 1996.13 Even Detroit, having just emerged from bankruptcy in December 2014, issued $245 million in bonds in August 2015. The city directed the funds to a number of projects, including upgrades to public safety vehicle fleets.14

A big year for bond refunding

Consistent with the trends since the Great Recession ended in July 2009, some of the cities analyzed continued to rely on refunding bonds, or essentially refinancing, in 2014. (See “Refunding Bonds.”) For example, refunding accounted for all of the issuances in Riverside, California, and Phoenix, and over 90 percent of the total issuances in Atlanta and Houston.

Cities realized significant savings through refunding and slower issuances of new debt. An examination of debt service payments from CAFRs (which are produced for fiscal years) shows that in fiscal 2013, 18 of 29 cities analyzed reduced their debt service spending. (Cincinnati could not be included in the spending and revenue analyses because the city changed its fiscal calendar in 2013, which made full-year comparisons difficult.) For example, Riverside cut its debt service spending by 41 percent from $110 million in fiscal 2012 to $65 million in fiscal 2013. These savings were important to Riverside’s bottom line, because the city’s revenue had yet to return to its pre-recession peak.

Refunding Bonds

Much like homeowners, cities can refinance their debt. They may do so in order to take advantage of low interest rates, to restructure their obligations in ways that reduce near-term debt service payments, or to remove restrictive covenants from old debt.* When cities want to refinance, they issue refunding bonds. The proceeds from these bond sales are used to retire existing debt, and the city then pays debt service on the new bond. By federal statute, a city generally can issue a refunding bond and maintain that bond’s tax exempt status only one time over the life of a debt.

*Tima T. Moldogaziev and Martin J. Luby, “State and Local Government Bond Refinancing and the Factors Associated With the Refunding Decision,” Public Finance Review 40, no. 5 (2012): 614–42, doi:10.1177/1091142111430954.

Cities continue to face revenue challenges

Many of the 30 cities continue to struggle with the effects of the Great Recession and face ongoing revenue challenges, a likely factor influencing slow sales of new debt. “There isn’t much political support for ambitious new projects or infrastructure,” Matt Fabian, a partner at Municipal Market Analytics, said in 2015.15

As of fiscal 2013, the latest year for which complete, audited financial data are available, nearly half of the cities studied (14 of the 29 with comparable data) had not yet experienced a single year since the end of the recession during which revenue returned to pre-recession peak levels. Even in cities where revenue had recovered, fiscal stability remained uncertain. Six cities that had already rebounded above their pre-downturn revenue peaks fell below those levels in 2012 or 2013: Atlanta, Chicago, Dallas, and Pittsburgh did so in 2012, and Minneapolis and St. Louis joined them the next year.

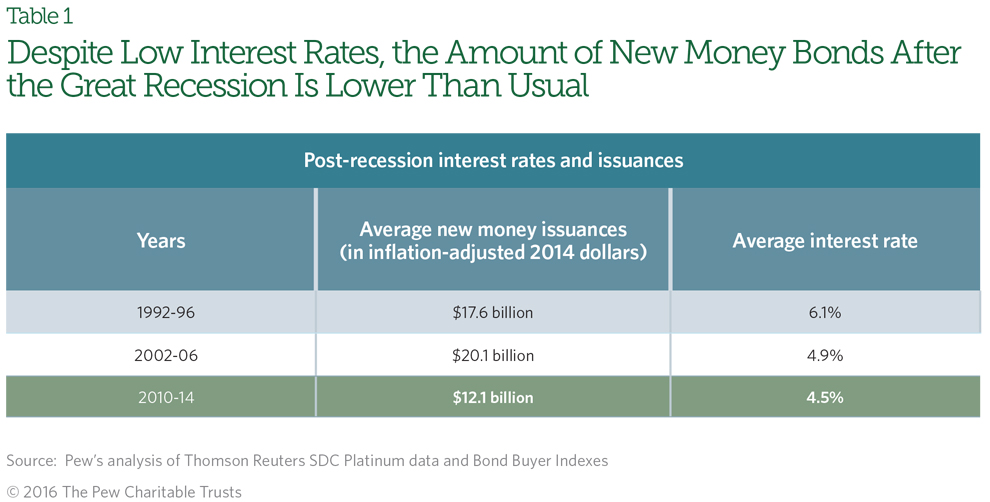

Persistently low revenue and uncertain futures may be two reasons that cities have responded to the Great Recession differently from previous downturns—when, generally, cities took advantage of the low interest rates that follow recessions to finance delayed maintenance and construction of new infrastructure. The period since 2008 has adhered to the pattern of low interest rates, but in recent years the 30 cities analyzed have been slow to issue new money bonds. Bond interest rates between 2010 and 2014 averaged just 4.5 percent, compared with 6.1 percent between 1992 and 1996 (the five years following the 1990-91 recession) and 4.9 percent between 2002 and 2006 (the five years after the 2001 recession).

Although interest rates were higher between 1992 and 1996 than after the Great Recession, the 30 cities examined for this brief collectively issued an average of $17.6 billion in new money bonds during each of these five years. Following the 2001 recession, these same cities issued an average of $20.1 billion in new money bonds per year from 2002 through 2006. During the recovery from the Great Recession, which ended in mid-2009, new money issuances averaged just $12.2 billion a year. What’s more, that figure is probably inflated somewhat by the availability in 2010 of Build America Bonds, the federal program launched in 2009 to encourage new investments.

New financing methods

The bond issuance totals may understate the amount of borrowing that cities engaged in over the past few years. Some may be turning to bank loans to finance capital investments; in addition, the federal bond program that became available in the two years immediately following the recession also may have been a factor in capital investment decision-making.

Bank loans

Although bonds are the traditional method used by municipalities to finance large expenditures such as infrastructure projects, governments also can turn to banks to secure direct loans. Because the Governmental Accounting Standards Board and the Municipal Securities Rulemaking Board have not yet developed rules for reporting these loans, it is difficult to measure the extent of this type of borrowing.16 Standard & Poor’s Ratings Services estimates that direct loans could have represented as much as 20 percent of all municipal issuances from 2011 through February 2014.17 In 2014, the 30 cities examined could have used bank loans to finance more capital projects than the bond data alone suggest. However, according to Municipal Market Analytics, the majority of bank lending to localities has been used to restructure existing debt, rather than for new money issuances.18

Build America Bonds

Aid from the federal government also may have changed the timing of capital investments made by the 30 cities. Build America Bonds offered incentives for cities to issue bonds in 2009 and 2010 through tax subsidies on interest rates. Pew’s analysis found that many cities responded to these incentives and moved up projects planned for later years.19 The amount of investment made through Build America Bonds was significant—accounting for 16 percent of total issuances made in 2009. However, this factor does not fully explain the low issuances seen since 2010 because not all cities took advantage of the program. Of the 30 key cities, 11 issued no Build America Bonds.20

Conclusion

The data for the cities analyzed show that bond issuances following the Great Recession have been lower than in two previous post-recession recovery periods, though the availability of bank loans probably means that the numbers do not fully capture the extent of the cities’ borrowing. Even though the national recovery began in 2009, many cities continued to face revenue challenges as of fiscal 2013—only nine of the 29 for which Pew had complete financial data returned to or exceeded their highest level of revenue since the downturn began. These fiscal pressures may have led cities to be wary of issuing new bonds as part of a broader strategy to fund infrastructure and of taking on additional debt service payments.

Endnotes

- The Pew Charitable Trusts, “Funding Challenges in Highway and Transit” (February 2015), http://www.pewtrusts.org/en/research-and-analysis/ analysis/2015/02/24/funding-challenges-in-highway-and-transit-a-federal-state-local-analysis.

- Because of incomplete data reporting by the cities, some bonds are reported in the Thomson Reuters SDC Platinum database as new money but were in fact used for refunding purposes. Owing to these errors, the amount of new money bonds could be lower than reported here, and the amount of refunding bonds higher.

- Securities Industry and Financial Markets Association, “Issuance in the U.S. Bond Markets,” accessed May 20, 2015, http://www.sifma.org/uploadedFiles/Research/Statistics/StatisticsFiles/CM-US-Bond-Market-SIFMA.xls?n=29653.

- Elizabeth Campbell, “Chicago Plans $784 Million Bond Sale for Midway Airport Projects,” Bloomberg, May 23, 2014, http://www.bloomberg.com/news/articles/2014-05-23/chicago-plans-784-million-bond-sale-for-midway-airport-projects.

- Chicago Department of Finance, City of Chicago Comprehensive Annual Financial Report for the Year Ended December 31, 2014 (2015), http://www.cityofchicago.org/content/dam/city/depts/fin/supp_info/CAFR/2014CAFR/ CAFR_2014.pdf.

- California Debt and Investment Advisory Commission, “Searchable Database for Bonds/Other Public Debt Issued by Governmental Entities in California,” accessed May 5, 2015, http://www.treasurer.ca.gov/cdiac/debtdata/entity.asp.

- City of Los Angeles, “Mayor Garcetti Announces L.A. Earns Highest Ratings From S&P, Fitch, and Moody’s,” news release, June 16, 2014, http://www.lamayor.org/ mayor_garcetti_announces_l_a_earns_highest_ratings_from_s_p_fitch_and_moody_s.

- D.C. Water and Sewer Authority, “DC Water Announces Successful Sale of $350 Million Green Century Bonds,” “MarketWatch,” July 10, 2014, http://www.marketwatch.com/story/dc-water-announces-successful-sale-of-350-million-green-century-bonds-2014-07-10.

- City of St. Louis, “Tax and Revenue Anticipation Notes Payable From the General Revenue Fund Series 2014,” Municipal Securities Rulemaking Board, Electronic Municipal Market Access System, CUSIP:79164MAU1 (June 19, 2014), http://emma.msrb.org/ER784127-ER609167- ER1011261.pdf.

- Office of City Controller, City of Pittsburgh, Comprehensive Annual Financial Report for the Year Ended December 31, 2014 (2015), http://apps.pittsburghpa.gov/co/ CAFR_December_31_2014.pdf; and Robert Zullo, “Pittsburgh to Get Lowest Interest Rate Ever for Bonds, Director Says,” Pittsburgh Post-Gazette, Aug. 27, 2014, http://www.post-gazette.com/local/2014/08/27/City-to-get-lowest-interest-rate-ever-forbonds-director-says/stories/201408270059.

- Bloomberg Data News, “Municipal Bond Sales to Rise in January After 23% Jump in 2015,” Dec. 28, 2015, http://www.bloomberg.com/news/articles/2015-12-28/municipal-bond-sales-to-rise-in-january-after-23-jump-in-2015. Last year, total bond sales from state and local issuers increased nearly 25 percent over 2014 issuances and reached the highest amount since 2010, when over $400 billion in bonds were sold, according to Bloomberg.

- Carla Caldwell, “Atlanta Voters Approve $250M Bond Referendum for Transportation, Construction Projects,” Atlanta Business Chronicle, March 18, 2015, http://www.bizjournals.com/atlanta/morning_call/2015/03/atlanta-voters-approve-250k-for-transportation.html.

- Cory Weinberg, “Prop. A’s Passage Unlocks Stream of Cash for Affordable Housing,” San Francisco Business Times, Nov. 3, 2015, http:// www.bizjournals.com/sanfrancisco/morning_call/2015/11/prop-a-affordable-housing-bond-sf-ed-lee-crisis.html.

- Bloomberg, “Detroit Sells $245 Million in Bonds, First Offering Since Emerging From Bankruptcy Court,” Crain’s Detroit Business, Aug. 19, 2015, http://www.crainsdetroit.com/article/20150819/NEWS01/150819835/detroit-sells-245-million-in-bonds-first-offering-sinceemerging.

- Matt Fabian (partner, Municipal Market Analytics), interview by The Pew Charitable Trusts, May 6, 2015.

- The Governmental Accounting Standards Board is an independent organization that establishes accounting and financial reporting principles for U.S. state and local governments. It sets the generally accepted accounting principles (GAAP) for these entities. Although the board is not a government body, compliance with its rules is maintained in some states through statute and also through auditors who judge financial statements based on GAAP compliance. The Municipal Securities Rulemaking Board establishes rules for the sale of municipal bonds. By doing so, it aims to protect investors, governments, and the public interest by ensuring a fair and transparent market. It was chartered by Congress and is overseen by the Securities and Exchange Commission.

- Standard & Poor’s Ratings Services, Alternative Financing: Disclosure Is Critical to Credit Analysis in Public Finance (2014), http://www.treasurer.ca.gov/cdiac/seminars/2014/20140205/sp.pdf.

- Fabian, interview.

- The Pew Charitable Trusts, Understanding the Great Recession’s Impact on City Bond Issuances (August 2013), http://www.pewtrusts.org/~/ media/assets/2013/08/02/municipal_bonds_report_final.pdf.

- These cities were Atlanta; Detroit; Kansas City, Missouri; Miami; Minneapolis; Philadelphia; Pittsburgh; Portland, Oregon; Sacramento, California; San Diego; and St. Louis.

ADDITIONAL RESOURCES

Article