Saving For Retirement Varies By State and Region

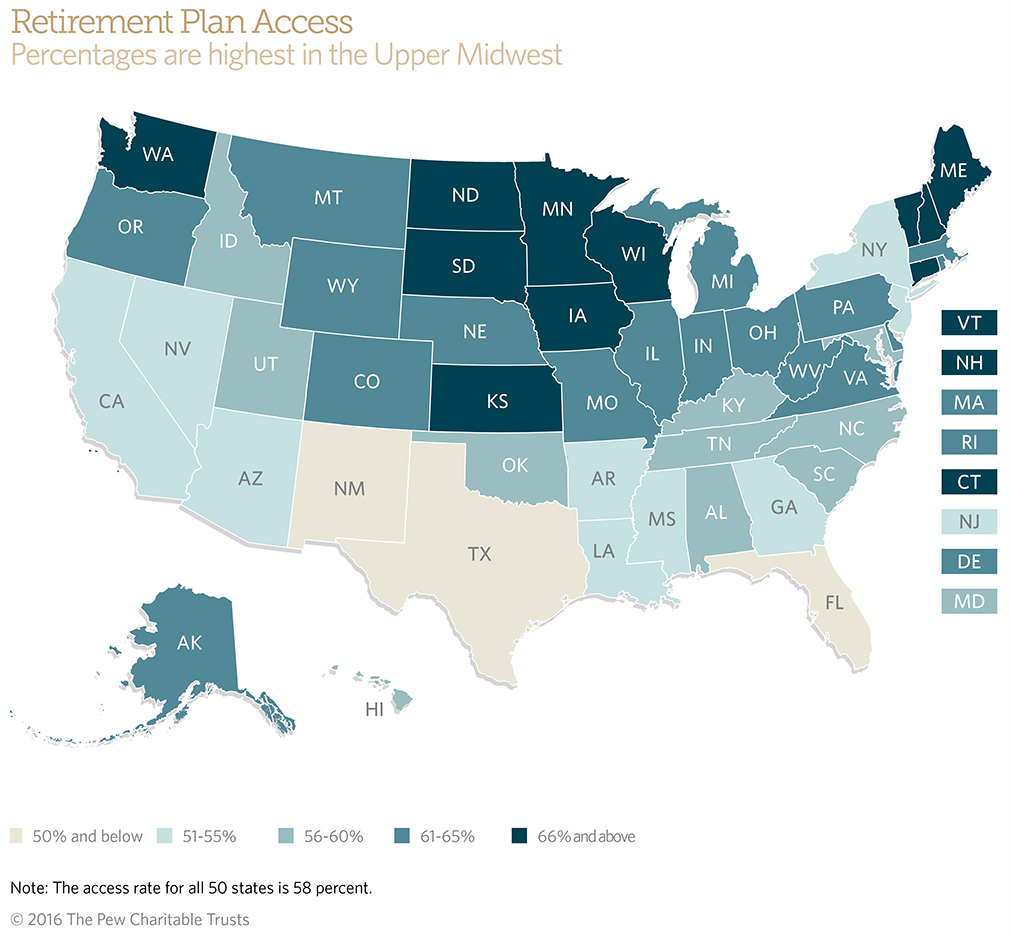

Rates of participation in employer-sponsored plans highest in Midwestern states

With the aging of the nation’s population, a continued decline in the availability of traditional pensions, and concerns about the future of Social Security, many Americans worry that they won’t be able to save enough to pay for their retirements.

Today, workers in the United States accumulate the vast majority of their retirement savings through employer-based plans such as 401(k)s, but many don’t have that opportunity.

Only about half of full-time private-sector workers—49 percent—participate in a workplace retirement plan, according to an analysis of data compiled by The Pew Charitable Trusts. Overall, 58 percent of workers have access to such a plan.

Looking at the numbers in a different way, more than 30 million full-time, full-year private-sector workers ages 18 to 64 lack access to an employer-based retirement plan.

The analysis also shows that:

- Access and participation rates vary widely across states and regions. For example, 61 percent of workers in Wisconsin and Minnesota participate in an employer-based pension or retirement savings plan, compared with 38 percent in Florida. Access and participation are higher in the Midwest, New England, and parts of the Pacific Northwest and lower in the South and West.

- Retirement plan access and participation vary based on employer size and industry type: Only 22 percent of workers at firms with fewer than 10 employees report having access to a workplace savings plan or pension, compared with 74 percent at firms with 500 or more. Certain industries, such as leisure and hospitality or construction, have much lower levels of access and participation than others.

- Access and participation differ substantially by employee income. Nationally, only 32 percent of workers with wage and salary incomes of less than $25,000 have access to a retirement plan at the workplace; the rate rises to 75 percent for workers with incomes above $100,000. Just 20 percent of those in the lower-income group participate in a plan, compared with 72 percent of more affluent workers.

- Younger workers and workers with less formal education are less likely to have access to a plan. Younger workers also are less likely to participate even if they have the option.

- Some of the largest differences are by race and ethnicity. Among Hispanic workers, access to a plan is around 25 percentage points below that for white non-Hispanic workers. Black and Asian workers also report lower rates of access than white workers.

Pew released a data visualization that shows how employer-based retirement plan access and participation vary among states and by characteristics such as employer size, industry, and wage and salary income. Users can click through the various tabs to obtain information of interest.

What states can do

The report also looks at numerous efforts at the state and federal levels to boost retirement savings. Illinois, for instance, adopted the Secure Choice Savings Program in 2015, which will start enrolling certain private-sector workers in new payroll-deduction retirement accounts by 2017.

In Washington, the state has created a marketplace in which small employers and the self-employed can shop for retirement plans. And the federal government has rolled out the “myRA,” a new national savings program that is geared toward low-income savers.

The report’s authors make clear that because of the wide differences in access and participation across the country, state lawmakers should consider the unique social and economic features of their states. For example, certain states have more workers at small businesses or in industries with relatively high turnover.

Other states have higher shares of minority workers who may benefit from targeted outreach materials to expand participation in new or existing plans.

Taking into account the characteristics of a state’s labor force can help policymakers improve retirement security while balancing the needs of both workers and employers.