Basic Legal Protections Vary Widely for Participants in Public Retirement Plans

States take differing approaches to setting core fiduciary standards

Overview

State and local pension plans hold over $3.6 trillion in retirement fund investments for participants and their beneficiaries, with returns on these investments accounting for an estimated 60 percent of the money paid out in pension benefits each year. In recent decades, public pension funds, in a bid to boost returns, have shifted funds away from low-risk, fixed-income investments—such as government and high-grade corporate bonds—to a greater reliance on equities and alternative investments. This strategy change can provide higher returns, but it increases the complexity of fund portfolios, as well as the risk of losses.

The rules governing plan trustees and administrators—those individuals, known as fiduciaries, with the authority to invest and manage these assets—have not always kept pace with this trend. Fiduciaries have a legal duty to exercise “great care” in managing plan assets. The origins of these duties date back centuries to what is known as the common law of trusts, which is widely recognized but uncodified law.

The common law of trusts provided adequate regulation when state and local pension funds were primarily invested in low-risk and fixed-income investments. But the increased complexity and risk associated with contemporary retirement system portfolios has created a need for clear standards governing the investment decisions made by those responsible for doing so.1 These more complex investments also require more expertise.

Research shows that when compared with private pension funds in the United States and all pension funds in Canada and Europe, U.S. public pension funds underperform by about 50 basis points per year, tend to invest more in risky assets, and use higher target rates for investment returns.2 Also, U.S. public pension plans— particularly those whose trustees have limited financial expertise—can be ill-equipped to make these types of investment decisions, which can have a negative impact on fund performance.3

For example, an independent audit in South Carolina showed that rapid diversification into alternative investments was difficult for a new, underresourced pension investment commission. In a study of the 73 largest state-sponsored plans across 50 states, The Pew Charitable Trusts found that the South Carolina Retirement System had a 10-year return of only 5 percent in 2015, compared with a 6.6 percent return for comparable funds. That ranked the state 40th out of the 41 similar-size funds. Below-average investment performance has accounted for nearly $4 billion of the state’s unfunded pension liability with losses that occurred during a period of heightened concern about fiduciary accountability. In response, lawmakers enacted reforms in April 2017 that streamline the state’s complex governance structure and create clearer lines of accountability.

Weak governance practices also played a key role in the serious fiscal distress facing the Dallas Police and Fire Pension System in recent years. In part because of failed local real estate investments, the pension fund is the lowest-performing of more than 100 city and state-sponsored pension funds studied. Investment underperformance, combined with the cost of a generous supplemental benefit plan, accounts for about $1.4 billion in unfunded liabilities—a deficit that will cost taxpayers more than $50 million annually for decades.

When states adopt accepted and common standards into written law, they can help ensure that plan fiduciaries act prudently in choosing investments. Clear statutory standards of fiduciary accountability can also boost confidence among participants and beneficiaries that fund assets will be carefully invested and administered.

Pension experts largely agree on what these fiduciary provisions should include, but codification varies widely from state to state, in contrast to the rules that govern employer-sponsored private sector retirement plans—rules for which are standardized under the federal Employee Retirement Income Security Act of 1974 (ERISA).4

Following the shift in the 1990s toward more complex pension investments, legal experts from all 50 states drafted several model laws, including the Uniform Management of Public Employee Retirement Systems Act of 1997 (Model Act). In 1997, the National Conference of Commissioners on Uniform State Laws recommended that every state adopt these measures. Some states followed the guidance, but many have proved slow to act.

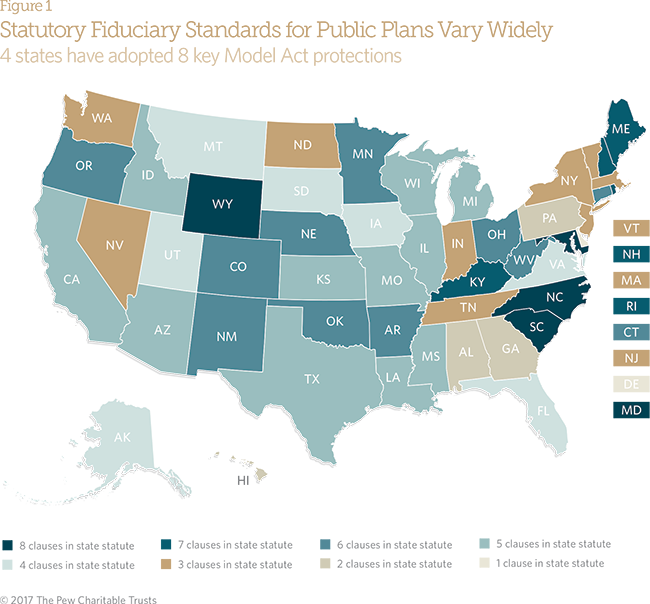

Pew identified eight key fiduciary duties and standards included in the Model Act that are particularly important to state and local pension plans.

The six core duties spelled out in the act require trustees or other fiduciaries to discharge their responsibilities with respect to a retirement system (bolding is added for emphasis):5

"(1) solely in the interest of [retirement system] participants and beneficiaries;

(2) for the exclusive purpose of providing benefits to participants and beneficiaries and paying reasonable expenses [for] administering the system;

(3) with the care, skill, and caution under the circumstances then prevailing which a prudent person acting in a like capacity and familiar with those matters would use in the conduct of an activity of like character and purpose;

(4) impartially, taking into account any different interests of participants and beneficiaries;

(5) incurring only costs that are appropriate and reasonable; and

(6) in accordance with a good-faith interpretation of the law governing the retirement program and system.”

The Model Act also identifies two other key responsibilities for trustees as they consider how to manage their systems’ assets. Among their duties, trustees:

- “Shall diversify the investments of each retirement program or appropriate grouping of programs unless the trustee reasonably determines that, because of special circumstances, it is clearly prudent not to do so.”

- “May consider benefits created by an investment in addition to investment return only if the trustee determines that the investment providing these collateral benefits would be prudent even without the collateral benefits (i.e., what are known as economically targeted investments or ETIs).”6

This brief reviews the laws of the 50 states to see how many have codified the Model Act’s core fiduciary standards for pension funds. The extent to which these provisions have been incorporated in state law is one measure of the strength of a state’s governance of state and local pension funds. State law should also provide explicit protections for both beneficiaries and taxpayers. And the absence of clear governing standards can lead to problems for retirement funds.

Pew’s review of the eight Model Act standards in place across the country finds that:

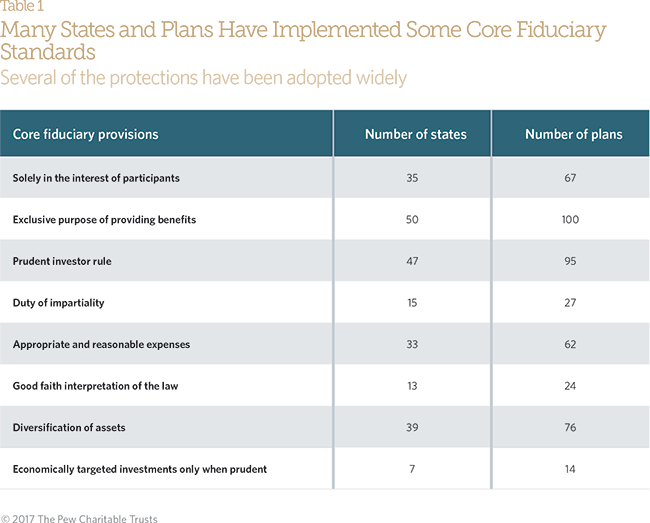

- Three of the most basic and general fiduciary standards and duties described above have been incorporated in the laws of most states.

- Every state requires fiduciaries to act for the exclusive purpose of providing benefits to beneficiaries.

- Only Delaware, Georgia, and Hawaii do not specifically require that investments be managed in a prudent manner.

- Thirty-nine states require that pension fund investments be diversified to protect beneficiaries and to reduce the likelihood of significant losses.

- Codification of the five other duties and standards varies widely. For example:

- Although many states require that certain types of investments be made in-state, the guidance for selecting among these investments is inconsistent and wide-ranging.

- Just seven states explicitly require that all economically targeted investments be held to a standard of care, skill, and caution under the circumstances then prevailing that a prudent person acting in a like capacity and familiar with those matters would use even without collateral benefits.

Pension investment practices and varieties have become increasingly complex, and fiduciary law is only one component of effective plan governance and management. Others include pension funding policies, investment expertise, and plan transparency. Adoption of fiduciary standards does not guarantee profitable investments, but failure to incorporate the core standards in states’ regulatory frameworks disregards long-established expert recommendations and could put plans and their participants at risk.

Responsibilities of Trustees and Fiduciaries

State and local pension plans are usually run by a board of trustees, which invests and manages the assets. Many states allow the trustees to delegate certain day-to-day fund operations and investment oversight to plan administrators or others. In most states and under the Model Act, trustees and those individuals with discretion to manage public employee retirement systems or plans, or to invest their assets, are fiduciaries. In those cases where others have decision-making responsibility and serve as fiduciaries, the trustees usually remain fiduciaries responsible for monitoring delegated decisions.7

Public and private plans: Different legal standards and protections

Private sector retirement plans must follow federal standards set under ERISA, but the rules covering public sector plans are far less consistent. The provisions in the Model Act were intended to provide guidance for pension plans for local and state workers.

Congress enacted ERISA in 1974 in response to concerns that private pension plan funds were being mismanaged and abused. ERISA makes clear that the fiduciary has an obligation to diversify plan investments to minimize the chance of significant losses. Lawmakers sought this provision to respond to the long-running shift from predominately fixed-income holdings to a more diverse range of investments—such as equities, real estate, and commodities—that began in the 1960s. The ERISA standards reflect what is often described as modern portfolio theory, the widely accepted body of empirical and theoretical knowledge about the behavior of capital markets.8

Standards in the Model Act—such as the one requiring funds to diversify their investments—are intended to incorporate modern portfolio theory. Diversification requirements have been adopted by 39 states as part of laws regulating state and local employee retirement plans.

8 standards of fiduciary responsibility

The Model Act reflects a consensus among experts and builds on existing practices and traditions. Because of its wide acceptance, Pew uses it as the base for identifying key fiduciary responsibilities that should apply to all public pension plan trustees and fiduciaries.9 Of course, the absence of a fiduciary standard does not necessarily mean that those individuals responsible will not exercise good judgment. At the same time, these core standards play an important role in helping to guide these decisions, and there are situations where the absence of such standards is a problem.

General fiduciary duties

Solely in the interests rule

The solely in the interest provision reflects what is known as the trust duty of loyalty to the participants and beneficiaries of a pension plan. Trustees must place their duty to plan participants and beneficiaries above any other duties to anyone else, whether or not those other duties are related to the plan.

This rule means that the trustee or fiduciary cannot serve as an “agent” of the state, a labor union, or any other entity that might be responsible for the trustee’s appointment to a board of trustees. Even when fiduciaries are elected public officials, they cannot put the needs of taxpayers above the interests of plan participants and beneficiaries. If investment actions are taken to benefit the state and only incidentally benefit plan participants and beneficiaries (because they are residents or taxpayers), the fiduciary has not met this loyalty duty.10

Currently, 35 states include the solely in the interest provision in statute or their constitutions. In the private sector, this standard is clearly spelled out in ERISA rules and has been validated in federal court rulings.

Case study

Dallas Mayor Mike Rawlings (D) referred to the solely in the interest standard in Texas law when he sued the Dallas Police and Fire Pension System in December 2016.11 By that point, poor investment results, including failed investments in local real estate, had helped bring the city’s public safety pension fund shortfall to about $8 billion.12 At 2.7 percent a year through 2015, the fund’s 10-year performance had proved well below the fund’s target rate and ranked last out of the 105 state and city funds that Pew tracks. Worse than expected returns accounted for about half of the plan’s unfunded liability. Belowaverage returns, combined with costly benefit enhancements, account for nearly $1.5 billion of the plan’s unfunded liability. City taxpayers face an estimated cost of over $50 million annually to close that gap.13

More recently, the system faced possible insolvency because so many retirees had made optional lump sum withdrawals using what is known as a deferred retirement option plan (DROP). City attorneys argued in the lawsuit that each time plan members made those withdrawals “every other member, pensioner, and beneficiary is being deprived of a constitutionally protected benefit.” The mayor argued that plan trustees have a duty to manage the system solely in the interest of the beneficiaries as well as a responsibility to deal impartially with all beneficiaries.14 In January 2017, the mayor withdrew his request for a temporary restraining order after the system’s board voided all outstanding DROP withdrawals. Officials in Dallas and the Texas Legislature made major modifications that included reductions in benefits for future retirees and more limited access to DROP funds to put the system on a sustainable financial footing.

Exclusive purpose of providing benefits rule

The exclusive benefit rule is meant to focus the fiduciary’s attention on the reason for the plan or trust. Those responsible for management should not be influenced by motives other than accomplishing the plan’s purpose. The rule allows fiduciaries to pay reasonable administrative expenses from a plan when necessary to benefit participants and beneficiaries. Any extravagant administrative expenses, payments in the fiduciaries’ interest, or payments in the interest of any other party would violate this rule.

The exclusive purpose standard overlaps with the solely in the interest rule, but emphasizes different goals. The latter says that trustees must always put the benefit of participants and beneficiaries above their own interests or those of others parties. The exclusive purpose rule focuses on the trustee’s role, which is to provide benefits to the participants and their beneficiaries and to limit trust expenses. Together these rules comprise the trustee’s most basic duty—loyalty to plan participants and their beneficiaries.

Pew found that all states have adopted the exclusive benefit rule in statutes, constitutions, or regulations. The federal Internal Revenue Code requires this rule for tax qualification, which affords tax-favored status to the plan.

Case study

The exclusive benefit standard proved to be a factor in a Detroit municipal corruption case. According to court records, Mayor Kwame Kilpatrick (D) and City Treasurer Jeffrey Beasley in 2006 and 2007 solicited and received $125,000 in secret gifts from Chauncey Mayfield, an investment adviser who wanted the city’s pension fund to invest $117 million in his company’s real estate projects. As pension fund trustees, Kilpatrick and Beasley voted to approve the investment. The fund suffered losses of $97 million on these and related pension deals occurring mostly between 2007 and 2010.

In 2013, the three were convicted of various crimes, including conspiracy to defraud retirees through bribery and kickbacks. Each served prison time.15 In the criminal charges, the Securities and Exchange Commission noted that Michigan state law defined the trustees and the realty firm as investment fiduciaries. The General Retirement System of Detroit also had an ethics policy on conflicts of interest that focused on the exclusive purpose duty, a duty the former officials had failed to meet:

“A pension board must discharge all its duties solely in the interest of the participants and beneficiaries for the exclusive purpose of (1) providing benefits to participants and beneficiaries; and (2) defraying reasonable expenses of administering the retirement system or pension fund.”16

Prudent person or prudent investor rule

The prudent person rule plays a central role in administering state and local government plans. It is also one of the oldest fiduciary rules, dating back to an 1830 U.S. Supreme Court case.17 The prudent person rule requires fiduciaries to make investment decisions similar to those that would be made by someone acting in a similar capacity and familiar with pension issues, as opposed to what is known as a prudent amateur.

Pew found that every state except Delaware, Georgia, and Hawaii incorporates the prudent person rule in its statutes or constitutional provisions governing public retirement funds.

Case study

Seeking higher returns, some public pension funds invest heavily in more volatile investments—known as alternative investments—such as hedge funds and private equity. These types of investments can be complex and risky, and often carry more expensive fees.

Between 2010 and 2014, the Kentucky Retirement System (KRS) invested $24 million with the Camelot Group, which ran a private equity fund. In 2014, Camelot’s founder and manager was indicted for fraud for allegedly stealing millions from the fund and sent to prison the following year. In 2009, the KRS had invested $100 million in Arrowhawk Capital Partners, a new fund that failed and closed in 2012.

In a case still pending in mid-2017, the Kentucky city of Fort Wright sued the retirement system for making “illegal and imprudent investments” involving hundreds of millions of dollars. The lawsuit filed in state court alleges that Kentucky statutes prohibit the investment of some of these assets in unregistered hedge funds or private equity funds.18

The city’s suit highlights the prudent person rule, noting that in selecting the type of investments permitted for pension fund investments, the board, as a fiduciary, must use the care, skill, and caution a prudent person would use in light of the circumstances.19

Although no clear relationship exists between the use of alternatives and total fund performance, there are examples of top-performing funds that have long-standing alternative investment programs. Conversely, funds with recent and rapid entries into alternative markets—including significant allocations to hedge funds—were among those with the weakest 10-year yields.20

Impartiality

The duty of impartiality acknowledges that even though a fiduciary for a retirement plan must be loyal to all plan participants and beneficiaries, different groups covered by the plan may at times have different interests. The plan fiduciary must be able to impartially consider potentially differing interests of participants and beneficiaries, such as those that may arise between retirees and working members, younger and older participants, or longterm and short-term employees. Although fiduciaries are required to consider the interests of various groups in making decisions regarding pension plans, they are not bound to make decisions that ensure absolute equality among competing interests.

The duty of impartiality is incorporated in the statutes, constitutions, or regulations of 15 states. The Texas lawsuit involving the Dallas Police and Fire Pension System, referred to earlier in reference to the solely in the interest standard, also highlights the impartiality standard because the case raises questions about balancing the needs of different groups of plan beneficiaries. “If a trust has two or more beneficiaries, the trustee shall act impartially in investing and managing the trust assets, taking into account any differing interests of the beneficiaries,” according to the suit. The case is still pending, but the district court granted an emergency temporary restraining order to stop withdrawals that could harm the overall health of the fund.

Case study

In 2006, the Oregon Public Employees Retirement Board (PERB) sought to recover overpayments from certain retirees after determining that they had received benefits beyond what they were entitled to. The Oregon Supreme Court held that the PERB was within its authority to recover the excess amounts, but found that one of the recovery mechanisms chosen by the board violated the impartiality rule.

The PERB had decided to treat the overpayments as an administrative expense, which effectively spread the burden of the costs among current employees without recovering any of the overpayments from retirees. Because this approach favored retirees over other beneficiaries, it violated certain well-established trust principles. The court found that trustees have a duty of impartiality and must administer the trust “impartially and with due regard for the diverse beneficial interests created by the terms of the trust.”21

Appropriate and reasonable costs

Thirty-three states include in their statutes, constitutions, or regulations the explicit duty to pay only expenses that are appropriate and reasonable under the circumstances. Whether administrative expenses are reasonable depends on many factors, including an assessment of the fiduciary’s knowledge about the tasks that must be performed. For example, a fiduciary who has no experience with actuarial calculations may take more time asking questions of an actuary about a study focused on those calculations. Even if an actuary were to charge reasonable hourly rates, the cost of the time spent with the fiduciary would be higher than the cost if the fiduciary had been an actuary. Still, this cost probably would be reasonable under the circumstances.

Case study

In 2015, Robert Rust, the executive director of the Louisiana Municipal Employee Retirement System, resigned after a state audit found that he and the board of trustees had improperly spent more than $300,000 on conferences, expensive dinners, cocktail parties, and travel between January 2010 and December 2014.22

After investigating the spending, the Louisiana legislative auditor found that “our research failed to reveal any legal authority for operating funds to be used in a manner inconsistent with the mandate that a trustee ‘discharge his fiduciary duties solely in the interest of the system’s members and beneficiaries and for the exclusive purpose of providing benefits to the members and their beneficiaries, and defraying reasonable expenses of administering the system.’”23

The auditor found these expenditures appeared to violate the appropriate and reasonable costs standard.

Good faith interpretation of the law

When it comes to understanding the law, fiduciaries must exercise their best judgment but are not required to be infallible. For example, a fiduciary who acted prudently—with a good faith belief that his or her actions were in compliance with the law—would not necessarily violate this duty if actions taken were based on a misunderstanding of a fine point of law. This means that technical legal violations made in good faith are not necessarily considered imprudent.

Thirteen states have language in state law or regulations that require pension fund trustees or other fiduciaries to discharge their duties using a good faith interpretation of the laws governing the retirement program or system.

Case study

In 1987, the Wisconsin Department of Employee Trust Funds and the Employee Trust Fund Board used Wisconsin Retirement System (WRS) trust funds to pay a “special investment performance dividend” to those who had retired before 1974 who were receiving payments from an annuity reserve account that held investment earnings for all system retirees. However, the formula for the distribution of the payments resulted in three-quarters of annuitants receiving nothing from the dividend distribution. Before implementing the special dividend, the WRS obtained the state attorney general’s advice that the act authorizing the dividend did not violate the contracts clause of the Wisconsin Constitution.

In response to a request from a state legislator, the state attorney general also found that the act did not violate a clause of the state constitution prohibiting the payment of extra compensation. However, the state Supreme Court later determined that the act did violate the state constitution provision prohibiting a taking of property without due process of law. The court determined that the annuitants who did not benefit from the dividend distribution had what is known as a property right to the account’s investment earnings. That meant they were entitled to have annuity reserves equitably distributed in a manner consistent with law.

Still, the court found that the trustees had not violated their fiduciary duties when they implemented a law based on legal advice offered in good faith.24 They had therefore made a good faith interpretation of the law, even though that was later found to be incorrect.

Investment fiduciary duties

Diversification

The rule of diversification stems from the prudent investor rule, because today’s prudent and knowledgeable investors generally invest based on “modern portfolio theory.” In the context of a public retirement system, this typically means that the system should invest in assets with a range of risks to balance the potential for gains and losses.

Typically, an investment with a higher expected rate of return has a greater risk of not meeting its target objectives. In addition, investing a high percentage of funds in a single investment may make a retirement fund too vulnerable to that entity’s success or failure. The diversification rule ensures that a portfolio’s potential for gains and losses is balanced—so that while the portfolio may not earn the highest possible return during an economic boom, the impact of catastrophic losses will be minimized during an economic downturn.

Most states make their preference for diversification of investments clear: Thirty-nine have provisions in statutes or regulations requiring that pension fund investments be diversified.

Case study

By 2015, the Retirement Systems of Alabama (RSA) had invested about 10 percent of its assets in two state-based multimedia companies, Raycom Media and Community Newspaper Holdings Inc. The RSA had founded Raycom, a privately held company, in 1996 and has been its primary financing source.25 Such a high proportion of assets in two entities meant significant pension fund vulnerability linked to the financial health of the companies, their products, and the markets in which they operate. If the company or media sector more generally were to flounder—even if other sectors of the economy were booming— low returns on this investment could significantly decrease the value of Alabama’s retirement fund and make it harder to make promised payments to plan members.

In addition, privately held and private equity holdings typically do not represent such a significant percentage of an investment portfolio. Such media investments would ordinarily be part of a more diversified portfolio.

Alabama, however, does not have a statutory provision requiring diversification of assets. That leaves the retirement system potentially facing greater risk than a more varied portfolio.

Economically targeted investments

The U.S. Department of Labor defines “economically targeted investments’’ (ETIs) by private sector pension funds as investments selected for the economic benefits they create, apart from the investment return to the employee benefit plan.26 The same definition holds true for public sector plans not covered by ERISA. These can include job creation and savings, business development, and an increased stock of affordable housing. These investments can sometimes result in conflicting objectives between the needs of plan participants, who benefit from maximizing returns, and the sponsoring state or locality, which may benefit from lowered costs, additional tax revenue, or new economic development. State statutes sometimes direct that governmental pension plans invest within their states or in certain specific offerings, such as residential mortgages, despite the possibility that they will bring a substandard rate of return.

Case study

In 2015, the Retirement Systems of Alabama had about 16 percent of its assets invested in-state—in private equity or private placement investments and real estate, such as golf courses, office buildings, condominiums, hotels, and resorts. This included an investment of 9 percent of the total portfolio in a single privately held media company. That’s one of the highest percentages of in-state investments of the 73 largest state pension funds in Pew’s investment database.

Investments in Alabama real estate over the past decade or so have lagged behind median public plan returns on real estate investments: Ten-year returns for RSA real estate investments as of Sept. 30, 2014, were 2.32 percent, compared with Wilshire Trust Universe Comparison Service median public plan real estate returns of 8.78 percent (both gross of fees).

The RSA’s in-state investments also have raised questions about whether they were made solely in the interest of participants or beneficiaries.27 Alabama does not have a provision requiring that such economically targeted investments be made solely in the interest of participants or beneficiaries.

The U.S. Labor Department says that private plan fiduciaries that are considering ETIs must evaluate them from the viewpoint of the risk-adjusted rate of return for participants and beneficiaries. Fiduciaries evaluating these investments may consider community benefits beyond returns only if they determine that the investment makes sense on its own—without the benefits to the state or taxpayers.

Professional associations also have called for states to adopt specific fiduciary provisions governing investments in ETIs. For example, the National Association of State Retirement Administrators and the Government Finance Officers Association have both issued best practice recommendations on ETIs.28 The National Conference of Commissioners on Uniform State Laws made its stand on ETIs clear in the Model Act, which calls for the same general approach for public plans. Under that standard, fiduciaries can consider what are known as collateral benefits of an investment only if the investment would be prudent without those additional benefits.

Still, many states require public employee retirement plans to make economically targeted or in-state investments. Some have adopted standards that follow the Model Act guidelines. Others have laws that set limits on ETIs ranging from 2 to 3 percent of assets in Florida and Montana to 10 percent in Arkansas. Some states provide no guidance at all.

Pew’s review of state laws found that seven have statutes or regulations that permit consideration of collateral benefits, such as in-state development, only when fiduciaries determine that the investments would be prudent even without the additional benefits.

Reviewing state practices and requirements

Pew’s examination of state laws, constitutions, and court cases found that key standards, such as the exclusive benefit and the prudent person rule, were incorporated in the written laws governing pension plans in most states. But states took a wide range of approaches to incorporating the more specific standards.

In some instances, states provide plan decision-makers with limited guidance on how to select among investment options. In addition, many legislatures have set statutory preferences for certain types of in-state investments by pension plans.

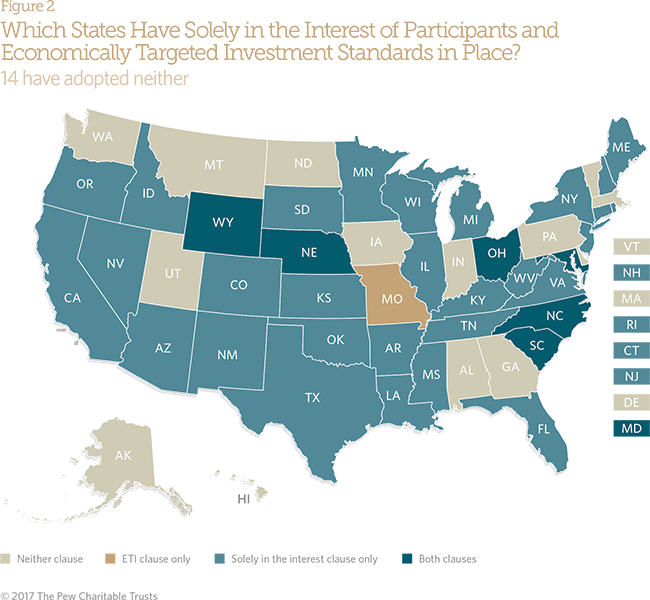

Fiduciary standards can help trustees and administrators better handle political pressures for certain types of investments, such as those made in-state. First, fiduciaries must place their duty to plan participants and beneficiaries above any other duties—the solely in the interest rule. Second, any economically targeted investments under consideration must be deemed prudent before factoring in any potential benefits to the state. Currently, Missouri is the only state that requires or allows ETIs that does not have specific provisions requiring that investments either be made solely in the interest of plan participants or that they first be prudent for the plan.

Conclusion

Spelling out basic fiduciary duties in state statute or regulation helps establish core standards for managing a public employee pension system. Pew reviewed the principles governing retirement systems in all 50 states that hold over 95 percent of state and local plan assets. The research found a wide range of adherence to the generally accepted, clear, and explicit fiduciary standards in the Model Act.

Experts in plan governance recommend incorporating these standards into a state’s regulatory framework. Failure to do so could put plans and their participants at risk. While more states appear to be strengthening these protections, all should address these fiduciary issues to establish greater accountability for plan administration and investment. Incorporating these rules helps form a basis for decision-making and effective operational practices.

Endnotes

- Congress recognized this need, and consequently the Employee Retirement Income Security Act of 1974 (ERISA), as amended, includes uniform written standards to protect employees of private plans and plan members. See ERISA, 29 U.S.C. chap. 18 at §1001et. seq. (1974).

- Aleksandar Andonov, Rob Bauer, and Martijn Cremers, “Pension Fund Asset Allocation and Liability Discount Rates,” accessed Feb. 28, 2017, https://papers.ssrn.com/sol3/Papers.cfm?abstract_id=2070054.

- Aleksandar Andonov, Yael Hochberg, and Josh Rauh, “Political Representation and Governance: Evidence from the Investment Decisions of Public Funds,” accessed Feb. 28, 2017, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2754820.

- ERISA §1002 (21)(A) states in part: “… a person is a fiduciary with respect to a plan to the extent (i) he exercises any discretionary authority or discretionary control respecting management of such plan or exercises any authority or control respecting management or disposition of its assets, (ii) he renders investment advice for a fee or other compensation, direct or indirect, with respect to any moneys or other property of such plan, or has any authority or responsibility to do so, or (iii) he has any discretionary authority or discretionary responsibility in the administration of such plan.” Courts often look to ERISA practice and court decisions in interpreting provisions of the Model Act and state laws.

- Uniform Law Commission, “Uniform Management of Public Employee Retirement Systems Act (UMPERSA)” (1997), §7, http://www.uniformlaws.org/shared/docs/ management_public_employee_retirement_systems/mpersa_final_97.pdf.

- UMPERSA §§ 8(a)(2) and (5).

- Liss v. Smith, 991 F. Supp. 278, 311 (S.D.N.Y. 1998): “The power to appoint and remove trustees carries with it the concomitant duty to monitor those trustees’ performance. … The duty to monitor carries with it … the duty to take action upon discovery that the appointed fiduciaries are not performing properly.”

- UMPERSA §8 Comments.

- Many states also incorporate other provisions from the Model Act, such as “conflict of interest” and “disclosure” provisions, which are proving to be of importance to public plans.

- See ERISA § 1104(a) (1), UMPERSA § 7(1), and comments citing NLRB v. Amax Coal Co., 453 U.S. 322 (1981) and City of Sacramento v. Public Employees Retirement Sys, 280 Cal. Rptr. 847 (Cal. Ct. App. 1991). The comments after UMPERSA § 7(1) are clear that “a trustee, must act solely in the interests of participants and beneficiaries, and set aside any interests of a party responsible for the trustee’s appointment, such as an employer or union.” This statement suggests that this would include the interests of the state, too.

- Alan Greenblatt, “Deficit in Dallas: How One of the Fastest-Growing U.S. Cities Ended Up With Billions in Debt,” Governing, April 2017, http://www.governing.com/topics/finance/gov-deficit-dallas.html.

- Ibid.

- Pew analysis of the Dallas Police and Fire Pension System.

- Rawlings v. Board of Trustees of the Dallas Police and Fire System (Pl. Orig. Pet. at 49, DC Case No DC-16-1541 Dallas Cnty. 2016), https://www.justice.gov/usao-edmi/pr/former-detroit-city-treasurer-sentenced-eleven-years-prison-taking-bribes-exchange-tens.

- U.S. Attorney’s Office, “Former Detroit City Treasurer Sentenced to Eleven Years in Prison for Taking Bribes in Exchange for Tens of Millions in Detroit Pension Assets,” Sept., 21, 2015, https://www.justice.gov/usao-edmi/pr/former-detroit-city-treasurer-sentenced-eleven-years-prison-taking-bribes-exchange-tens; U.S. Attorney’s Office, “Former Detroit Mayor Kwame Kilpatrick, His Father Bernard Kilpatrick, and City Contractor Bobby Ferguson Were Convicted on Racketeering, Extortion, Bribery, Fraud, and Tax Charges,” March 11, 2013. https://www.justice.gov/usao-edmi/pr/former-detroit-mayor-kwame-kilpatrick-his-father-bernard-kilpatrick-and-city-contractor.

- S.E.C. v. Kilpatrick, Civil Action No. 12-12109 (Compl. at Page 9, filed 05/09/12, E.D. Mich. 2012), https://www.sec.gov/litigation/complaints/2012/comp-pr2012-88.pdf.

- Harvard College v. Amory, 26 Pick. 446, 1830 Mass. Lexis 38 (1830).

- John Cheeves, “N. Ky. City Sues Kentucky Retirement Systems, Alleging ‘Illegal and Imprudent Investments,’” Lexington Herald Leader, June 3, 2014, http://www.kentucky.com/news/politics-government/article44491728.html.

- City of Fort Wright, Kentucky v. Board of Trustees of the Kentucky Retirement System, Case No. 14-Cl-1085, Kenton Circuit Court Division III, filed June 2, 2014.

- See The Pew Charitable Trusts, State Public Pension Funds Increase Use of Complex Investments (April 2017), p. 23, http://www.pewtrusts.org/~/media/assets/2017/04/ psrs_state_public_pension_funds_increase_use_of_complex_investments.pdf.

- Arken v. City of Portland, 51 Ore. 113 at 118, 263 P.3d 975, at 982.

- Rebekah Allen, “After $300,000 Spent on Parties, Travel, Meals, Auditor Questions Ex-Louisiana Retirement System Director,” The Advocate, Dec. 11, 2015, http://theadvocate.com/news/14216487-123/after-300000-spent-on-parties-travel-meals-auditor-questions-ex-louisiana-retirement-system-director.

- Louisiana Legislative Auditor, “Investigative Audit: The Municipal Employees’ Retirement System of Louisiana” (Dec. 2, 2015), https://app.lla.state.la.us/PublicReports.nsf/ 629F21AB90308A4B86257F0F00538CFF/$FILE/0000B63E.pdf.

- Wisconsin Retired Teachers Assn. v. Wisconsin Education Assn. Counsel, 207 Wis.2d 1 (WI. 1997).

- Securities and Exchange Commission, “Report of Investigation Pursuant to Section 21(a) of the Securities Exchange Act of 1934: The Retirement Systems of Alabama,” Release No. 57446, last modified March 6, 2008, https://www.sec.gov/litigation/investreport/34-57446.htm.

- Interpretive Bulletin 29 CFR § 2509.2015-01.

- Ex Parte Bronner, 171 So. 3d 614, 622-623 and 625 (AL 2014).

- National Association of State Retirement Administrators, “Resolution 1996-06—Retirement System Fiduciary Investment Standard,” Aug. 7, 1996, http://www.nasra.org/resolutions; Government Finance Officers Association, “Public Employee Retirement System Investments,” October 2009, http://gfoa.org/public-employee-retirement-system-investments.

ADDITIONAL RESOURCES

Opinion