Borrowers With Certain Educational Experiences Appear More Likely to Default

As student loan payments resume, survey analysis highlights share of those who studied part time, online, or did not complete their programs and encountered repayment problems

This article is the third in a series looking at survey data to analyze which student loan borrowers are most likely to experience default.

Borrowers with at least one of three educational attributes are among those most likely to experience default on their student loans: those who did not complete the degree or certificate for which they took out the loans, those who attended school part time, and those who were enrolled exclusively online. These findings emerge from a survey of borrowers conducted for The Pew Charitable Trusts in the summer of 2021.

Millions of borrowers began making student loan payments again in October—many for the first time—after the three-and-a-half-year payment pause put in place in response to the COVID-19 pandemic. A late 2022 survey also indicates that many borrowers felt less financially secure at that point than one year earlier, suggesting that future repayment challenges could become widespread.

Understanding the connection between these risk factors and default can help policymakers and loan servicers to identify vulnerable borrowers before they begin repayment and offer targeted supports to increase the likelihood that these borrower groups stay on track. It also helps highlight areas in the higher education system where improvements to school quality and additional student supports may be needed. That’s because positive postsecondary outcomes tend to translate into repayment success.

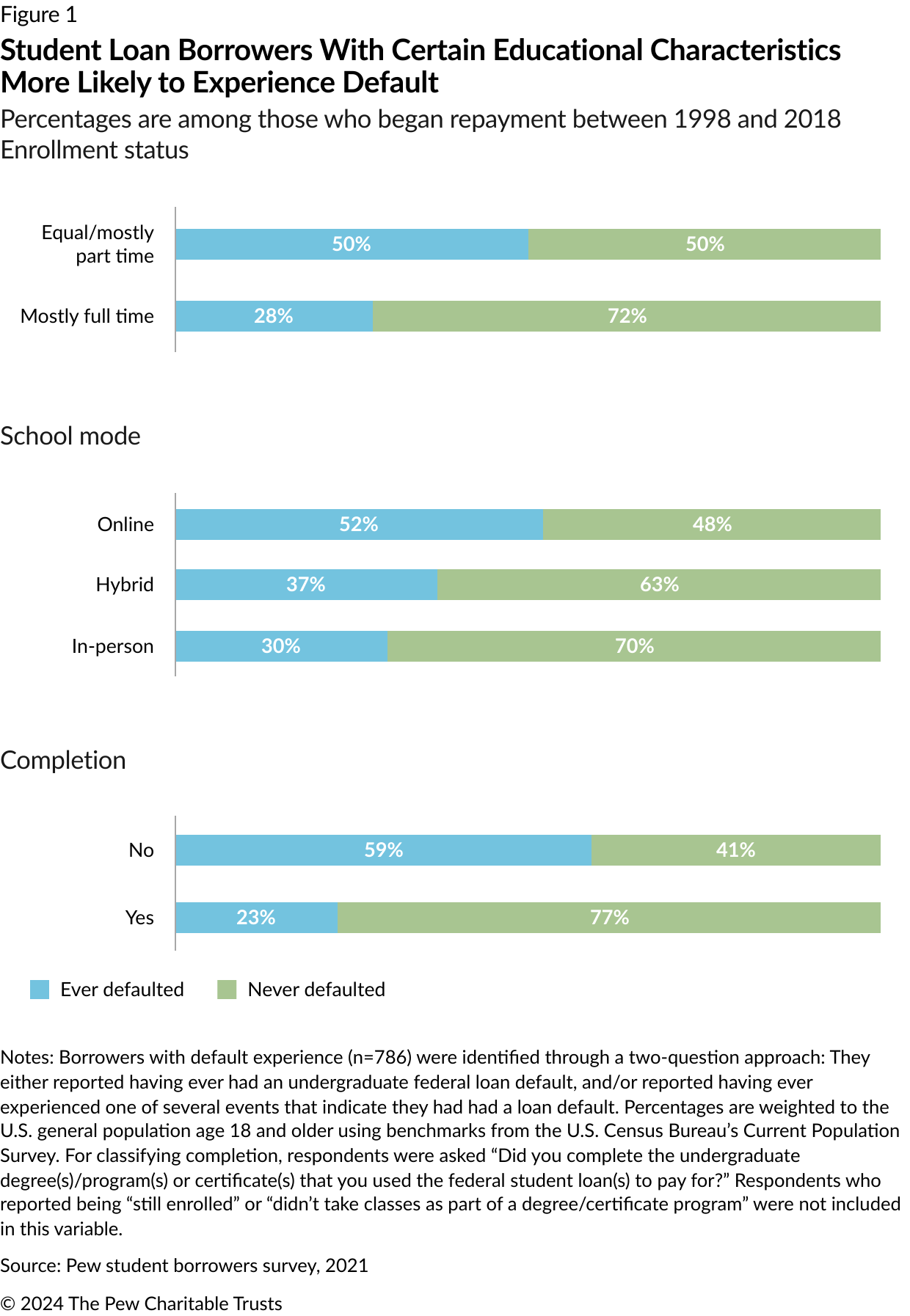

Although this descriptive analysis does not identify the causes of default, nor covers the full scope of risk factors that students or borrowers may face, it provides a first step in understanding why these three educational factors might foreshadow repayment struggles (see Figure 1):

- Part-time enrollment. Respondents who attended school part time for at least half of the time they were enrolled were much more likely to eventually experience default than those who attended school mostly full time (50% versus 28%, respectively). Research has shown that certain demographic groups are more likely to attend school part time, such as students of color and those who are 25 or older.

Students may decide to attend school part time for a variety of logical reasons. They might want or need to offset the cost of college by working while enrolled; one study from 2017 found that part-time students are more than twice as likely as full-time students to work full time. Yet, other studies have found that significant work commitments are associated with reduced academic performance and that students who attend part time are far less likely to complete their program than their full-time peers. That factor alone can add to the risk of experiencing student loan repayment challenges down the road.

- Online attendance. Those who enrolled in school exclusively online before the COVID-19 pandemic were also much more likely to later experience default than those who attended school in a hybrid format or completely in person (52%, 37%, and 30%, respectively). Students may decide to attend online programs for good reasons, such as the need for more course scheduling flexibility than an in-person program can offer. Some research, meanwhile, suggests that online education may expand access to higher education.

At the same time, studies show mixed results with student performance in online courses and indicate that they can lead students to lag in a virtual curriculum compared with in-person classes. Researchers need to better understand the impact of online postsecondary education on student outcomes, given the rapid increase in online enrollment, even before the pandemic.

This survey encompasses borrowers’ experiences with repayment that spans as far back as 1998, during which online education has developed and changed significantly, including a shift in the types of institutions that offer these programs. The impact of online education has also been difficult to study, in part because of limited data, but also because of the unique nature of online learning during the pandemic when many schools were forced to shift suddenly to virtual learning with limited time to plan and prepare. - Completion. Nearly 6 in 10 borrowers who reported not completing the degree or certificate for which they took out loans ended up experiencing default. Default was more than twice as likely among this group than among those who completed their degree or certificate (59% versus 23%, respectively). This is especially alarming given that only around 62% of students who entered school in the fall of 2016 earned a degree within six years. And these rates are significantly lower for certain groups, including Black, Hispanic, and Indigenous students; those who attend for-profit or public two-year schools; students who enroll part time; and those who are the first in their families to attend college. Earlier research has also linked noncompletion to default, with one study finding that 49% of borrowers who experienced default within a span of 12 years from entering their program had not completed their program.

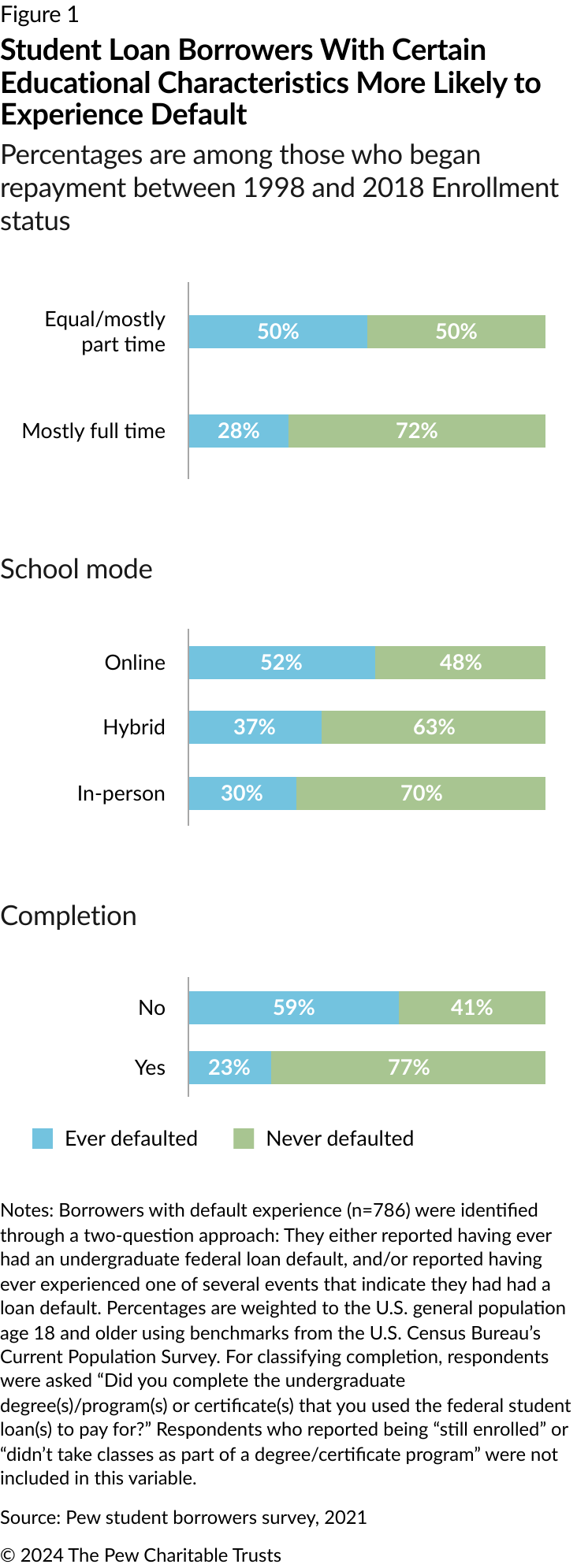

Affordability barriers to completion foreshadow default experience

In addition to measuring postsecondary completion among borrowers, the survey asked borrowers who left school before completion why they were unable to earn their degree or certificate. (See Figure 2.) From the responses, affordability stands out as both a leading reason for noncompletion and a reason much more likely to apply to borrowers who ultimately experienced default than to those who did not (37% and 21%, respectively).

This suggests that borrowers who end up with defaulted loans often face major financial challenges before they leave school. It further implies that the financial hardship these borrowers face can be both a cause and an effect of noncompletion. They can’t afford to complete their programs and then leave school with debt—but without a credential that boosts their earning potential.

Policymakers and servicers will need to monitor these educational risk factors alongside other demographic and financial characteristics that have been linked to default as borrowers continue the transition back into repayment in the coming months. They will also need to keep an eye on the status of borrowers who are leaving school and entering repayment for the first time.

This analysis is based on data from an online survey conducted by NORC using its AmeriSpeak probability panel on behalf of The Pew Charitable Trusts. This nationally representative survey, conducted from June 18 to July 28, 2021, studied borrowers’ experiences in and perceptions of the repayment system with a focus on those who had ever had a loan in default. Conducted after the federal student loan payment pause was announced in March 2020, the survey asked respondents to think specifically about their experiences with repayment and default before the start of the pause. Data collection was among a sample of 1,600 respondents. The margin of error for all respondents was +/-3.5 percentage points at the 95% confidence level.

Ilan Levine is a senior associate, Ama Takyi-Laryea is a senior manager, Phillip Oliff is a senior officer, and Lexi West is a principal associate with The Pew Charitable Trusts’ student loan initiative.

ADDITIONAL RESOURCES

Issue Brief

Article