Millions Use Bank Overdrafts as Credit

New small installment loans could help many who need to borrow

More than 39 million American adults incurred at least one fee for overdrawing their bank account or having insufficient funds in the past 12 months, according to an analysis of survey data by The Pew Charitable Trusts. Most of these consumers, known as overdrafters, view bank overdraft programs as a way to ensure that payments will go through if checking account balances are low. But almost a third—representing more than 12 million people—said doing so is a way to borrow when short on cash.

Overdrafts used in this way are an expensive form of short-term, small-dollar credit when safer, more affordable approaches are available to make ends meet. For example, federal regulators have begun to encourage financial institutions to create new types of safe small installment loans.

More broadly, Pew’s analysis shows that most of those who are charged a fee for overdrawing their accounts do not understand their right to have transactions declined without a fee. Better communication and disclosures by banks could help many customers avoid penalties and give everyone a better sense of the costs they face because of negative account balances. (See ”Customers Can Avoid Overdraft Fees, but Most Don’t Know How”.)

Wide use of overdraft as credit not reflected in regulations

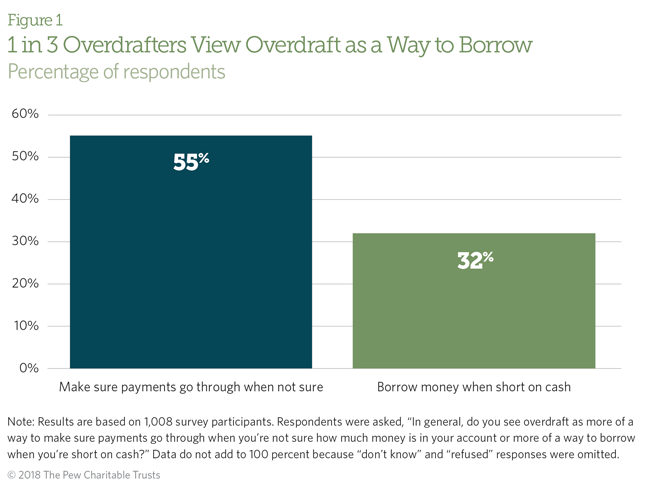

Most overdraft programs are marketed and regulated as fee-based services for occasional budgeting mishaps. Consumers typically use them that way, but this survey shows many use the programs as a form of credit. While 55 percent said overdrafts are a way to make sure payments go through when they aren’t sure they have enough money in their account, 32 percent see the programs as a way to borrow needed money.

The majority of those who overdraw and incur a fee said they experience budgeting issues at some point during the year: Three in 4 occasionally have trouble meeting monthly expenses. Heavy overdrafters—those who do so more than three times a year—are particularly vulnerable to shortfalls. These consumers were more than twice as likely to say they overdraft at an ATM, effectively taking an expensive cash loan—and demonstrating a clear interest in accessing credit.

Those who overdraw and want credit are often unable to access it. For example, more than half said they do not have enough available on a credit card to cover a $400 emergency expense. Four in 10 said they had applied for credit in the past year; of those, 30 percent were declined for the entire amount, and 10 percent were approved for only a fraction of the amount requested. These numbers do not include those who did not apply for credit because they believed they would not have been approved, an indication that the gap between demand and access may be even higher.

Household budgeting problems often intersect with a need for credit. Among those who applied for credit, 35 percent said that some or all of the request was denied and that they had difficulty meeting monthly expenses at some point during the past year. These circumstances help explain why so many use the programs as a form of credit.

Small installment loans can better meet consumer needs

Overdraft, when used for credit, is expensive and often poorly suited to consumers’ needs. Many overdraw using debit cards for small transactions and then face flat fees of around $35 for each transaction, an extremely high cost. Banks and their regulators never intended for overdrafts to become a form of credit, but survey data indicate that millions of adults use it for just that purpose. Doing so can lead to punitive fees, customer dissatisfaction, and account closures. Research by Pew in 2014, for example, found that more than a quarter of overdrafters had closed a bank account because of these fees. Further, reliance on overdrafts also can push some customers outside the banking system to costly nonbank services, such as payday loans. Pew research in 2013 showed that most payday loan borrowers also overdraw.

Policies that allow financial institutions to offer affordable small installment loans represent a sensible approach to meeting consumer needs. Last fall, the Consumer Financial Protection Bureau finalized a rule to limit the harms caused by short-term payday and auto title loans. The rule lays a strong foundation for banks and credit unions to provide lower-cost small installment loans, but doing so ultimately depends on decisions by federal and state bank regulators.

If regulators allowed banks to offer new small installment loans, consumers would have access to safe and affordable credit rather than payday loans or overdraft products—two expensive forms of credit. Safer, affordable small installment loans would also help keep more consumers in the banking system.

To read Pew’s recommendations for banks and credit unions developing small-dollar loan products, see “Standards Needed for Safe Small Installment Loans From Banks, Credit Unions.”

Nick Bourke is the director and Andrew Scott is a senior associate with The Pew Charitable Trusts’ consumer finance project.

FLIP TO FIND OUT

FLIP TO FIND OUT

Consumers Need Protection From Excessive Overdraft Costs

An evidence-based case for regulation to limit the number and amount of fees

Overdraft Does Not Meet the Needs of Most Consumers

Bank programs often function as costly, inefficient credit

Customers Can Avoid Overdraft Fees, but Most Don’t Know How

Bank disclosures and poor communication obscure options despite federal law