Pew's consumer banking project studied the accounts that Americans rely on every day to manage their finances, including checking accounts, prepaid cards, and mobile payments.

The initiative built partnerships with key stakeholders to advocate for effective consumer protections and a level playing field in the financial marketplace.

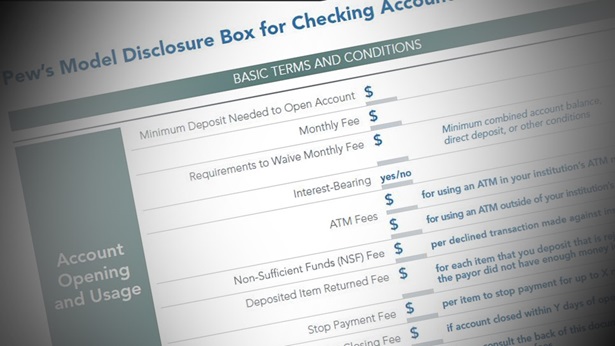

The Pew Charitable Trusts consumer banking project’s latest survey of checking accounts, Checks and Balances: 2015 Update, found the median length of disclosure materials for checking account agreements and fee schedules to be 40 pages, excluding addenda and other supplementary documents. Previous research has shown that few consumers read such lengthy information.

Mobile payments enable consumers to make financial transactions using their smartphones via a website, by sending a text message, or through an app. This technology, in turn, relies on many other consumer products and services, including credit, debit, and prepaid cards; wireless carriers; and nonbank providers such as Apple, Samsung, Google Wallet, and PayPal.

Every day, Americans use their smartphones to transfer money, pay for goods and services, and make donations. These transactions are collectively referred to as mobile payments. This infographic provides an overview of the many federal agencies that oversee the mobile payments marketplace, including payment processors and products.

Mobile payments technology allows customers to make online and point-of-sale purchases, pay bills, and send or receive money from their smartphones via Web browsers, apps, or text messages, and it has the potential to increase financial inclusion for consumers without bank accounts—the unbanked.

Ever use your smartphone to pay for parking or split the dinner bill with a friend? More people are using their phones as a mobile wallet and most mobile transactions work just fine. But with technology constantly evolving the rules that should protect consumers simply haven’t caught up.