{kind=link}

Click the figure to expand.

The challenges of managing growing public pension costs while recruiting and retaining a strong workforce have prompted policymakers across the country to take a closer look at the way they deliver retirement benefits to employees. Ten states have adopted hybrid pension plans that combine smaller, defined benefit pensions with defined contribution plans. When designing a retirement plan, there is no one-size-fits-all solution. The purpose of this brief is to explain the elements of a well-designed hybrid plan to help those interested in such plans make a more informed evaluation. Like a well-designed defined benefit or defined contribution plan, a well-designed hybrid plan can be part of an attractive compensation package that includes the elements necessary to promote retirement security for workers:

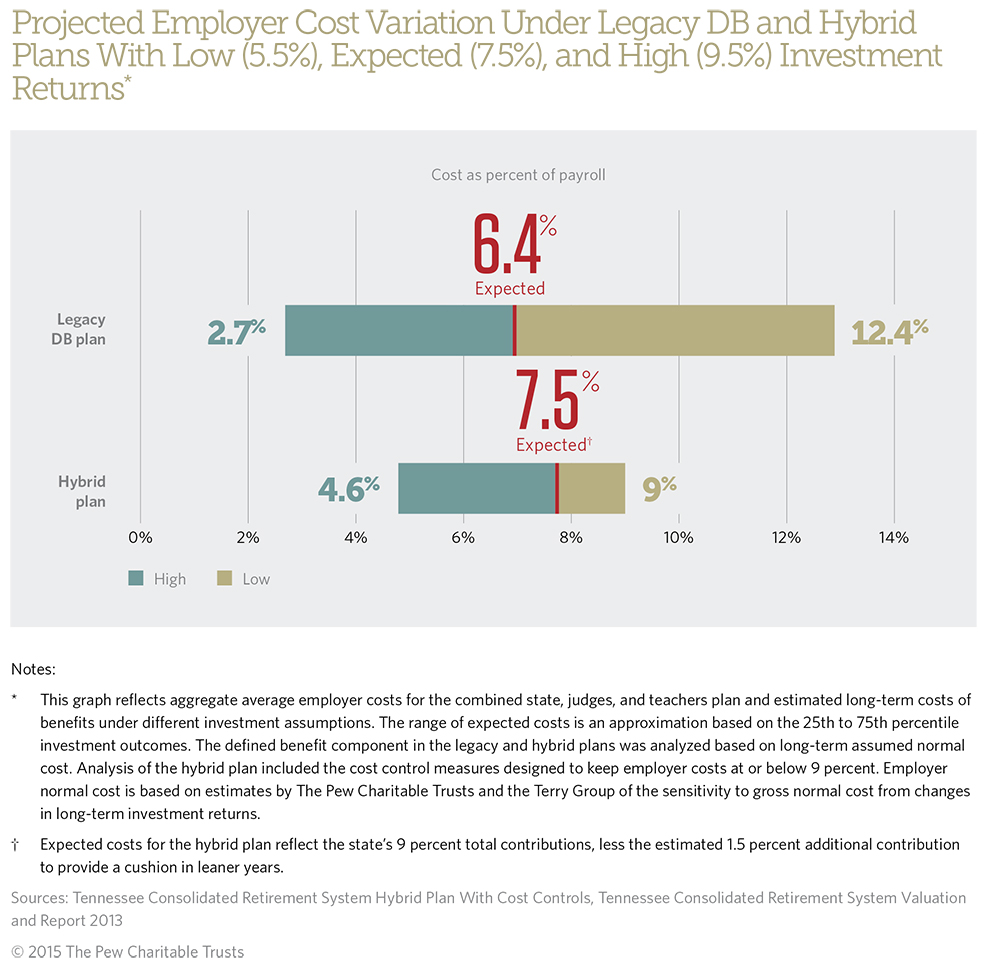

All workers need access to a secure retirement, and government employers need retirement systems that are financially sustainable over time. By combining a smaller, defined benefit plan with a defined contribution component, hybrid plans allow employers to improve the predictability of their costs. Moreover, there are specific cases in which a well-designed hybrid plan can be expected to provide a better benefit than a traditional pension for the large number of workers who change jobs during their working lives—while also providing career employees with substantial retirement benefits.

This brief reviews 12 hybrid plans in 10 states and includes a limited examination of the Federal Employees Retirement System’s hybrid plan. It describes the major features of the plans and specific aspects that policymakers should pay particular attention to if they are considering hybrid systems.

“Hybrid” is often used to refer to any retirement plan that combines some elements of a traditional defined benefit pension plan and a defined contribution plan with an individual retirement savings account to which the employee and employer contribute money. In this brief, we focus on the plan design known as a side-by-side hybrid, which combines a defined benefit (DB) based on the employee’s final average salary with a separate defined contribution (DC) savings account.1 Typically, the separate DB and DC portions in a hybrid plan provide a smaller benefit than they would in a stand-alone DB or DC plan, but when combined, they can provide a comparable level of total benefits.