Standards Needed for Safe Small Installment Loans From Banks, Credit Unions

Millions of borrowers could save billions of dollars annually

Overview

Several recent developments have raised the possibility of banks and credit unions offering small installment loans and lines of credit—which would provide a far better option for Americans, who currently spend more than $30 billion annually to borrow small amounts of money from payday, auto title, pawn, rent-to-own, and other small-dollar lenders outside the banking system. Consumers use these high-cost loans to pay bills; cope with income volatility; and avoid outcomes such as eviction or foreclosure, having utilities disconnected, seeing their cars repossessed, or going without necessities. Many of these loans end up harming consumers because of their unaffordable payments and extremely high prices; in the payday and auto title loan markets, for example, most borrowers pay more in fees than they originally received in credit.

Millions of households could benefit if banks and credit unions were to offer small installment loans and lines of credit with standards strong enough to protect consumers, clear enough to avoid confusion or abuse, and streamlined enough to enable automated low-cost origination.

Many credit unions and community banks already offer some small installment loans and lines of credit. But because regulators have not yet issued guidance for how banks and credit unions should offer small-dollar installment loans, or granted specific regulatory approvals for offering a high volume of such loans, these programs have not achieved a scale to rival the 100 million or so payday loans issued annually—let alone the rest of the nonbank small-dollar loan market. So, with most banks and credit unions either not offering small loans, or only offering them to people with relatively high credit scores, consumers with low or no credit scores looking to borrow small amounts of money often turn to alternative lenders in the nonbank market. Yet three-quarters of all households that use these alternative financial services already have accounts at banks or credit unions, and borrowers who take out payday loans in particular must have both an income and an active checking account to serve as collateral when their payments are due.

Now, the Consumer Financial Protection Bureau’s (CFPB’s) final small-loan regulation, issued in October 2017, permits providers to offer small installment loans and lines of credit with few restrictions—and adds strong consumer safeguards for loans with terms up to 45 days. Banks and credit unions have stated their interest in offering small installment loans and lines of credit, and some policymakers have expressed support for the idea. But while finalizing this rule was a necessary step for banks and credit unions to be able to offer such loans, it is not sufficient. In order for these loans to reach market, banks and credit unions will need to develop small-loan products, and their primary regulators—the Office of the Comptroller of the Currency (OCC), the Federal Reserve Board of Governors, the Federal Deposit Insurance Corp. (FDIC), and the National Credit Union Administration (NCUA)—will need to approve the products.

The opportunity for more banks and credit unions to enter the small installment loan market is not without its challenges. In order for these traditional lending institutions to seriously compete with the large number of payday and other nonbank small-dollar lenders that market aggressively, many banks and credit unions— especially large ones—would need not only to offer small-dollar loans but to make sure that consumers are aware that they offer such loans. And banks and credit unions would need to compete with nonbank lenders on speed, likelihood of approval, and ease of application, because small-dollar loan borrowers usually seek credit when they are in financial distress.

But banks and credit unions would also enter the market with large comparative advantages over nonbank lenders, with their lower costs of doing business allowing them to offer loans profitably to many of the same borrowers at prices six times lower than those of payday and other similar lenders. The banks and credit unions would be lending in a largely automated fashion to known customers who already make regular deposits, so both their acquisition costs and automated underwriting costs would be lower than those of nonbank lenders. The cost of capital for banks and credit unions is the lowest of any provider, and their overhead costs are spread among the multiple products they sell.

The idea of banks offering small-dollar loans is not entirely new, and experience is instructive. Until regulators largely put a stop to the practice in late 2013, a small number of banks offered costly “deposit advances” that were due back in a lump sum on the borrower’s next payday, at a fee most often of 10 percent per pay period—or roughly 260 percent annual percentage rate (APR). Regulators should not permit banks to reintroduce deposit advance loans; for consumers, it is also vital that any small-dollar loans from banks and credit unions not replicate the three key harms that characterized the deposit advance market: excessive pricing, unaffordable payments, and insufficient time to repay.

This brief includes guidelines for banks and credit unions to follow as they develop new small-dollar loan programs. The guidelines are designed to protect consumers and enable sustainability and scale for providers, who should offer small installment loans or lines of credit with the following features:

- Affordable installment payments of no more than 5 percent of each paycheck or 6 percent of deposits into a checking account.

- Double-digit APRs that decline as loan sizes increase.

- Total costs that are no more than half of loan principal.

- Loan payments that cannot trigger overdraft or nonsufficient funds fees.

- Online or mobile application, with automated loan approval, so that loan funds can be quickly deposited into a borrower’s checking account.

- Credit bureau reporting of loan terms and repayment.

The status quo

The nonbank options for credit are often poor, with high-cost loans dominating the landscape. Twelve million Americans use payday loans annually, and many others use different forms of high-cost credit.1 The FDIC has found that 20 percent of all American households are underbanked, meaning that they use alternative financial services in addition to using banks and credit unions.2

The bulk of research on payday lending has focused on whether consumers fare better with access to loans with unaffordable payments that carry APRs of around 400 percent, or whether, instead, these loans should be banned and small-dollar credit made mostly unavailable. But such research incorrectly assumes that these are the only two possibilities, especially since other studies have shown that consumers fare better than they do with payday loans when they gain access to alternatives featuring affordable installment payments and lower costs.3

Payday lenders’ products are so expensive because they operate retail storefronts that serve an average of only 500 unique borrowers a year and cover their overhead selling few financial products to a small number of customers. Two-thirds of revenue goes to handle operating expenses, such as paying employees and rent, while one-sixth of revenue covers losses.4 They have higher costs of capital than do banks or credit unions, they do not have a depository account relationship with their borrowers, and they often do not have other products to which borrowers can graduate. Their customer acquisition costs are high, and because storefront lending requires human interaction, they make limited use of automation. The online payday loan market, while it avoids the costs that come with maintaining retail storefronts, has higher acquisition costs and losses than do retail payday loan stores.5

Banks and credit unions do not face these challenges on the cost side—and, because of customers’ regular deposits into their checking accounts and pre-existing relationships with providers, the losses from small-loan programs run by banks and credit unions have been low.

Giving consumers a better option

Many customers use high-cost loans, pay bills late, pay overdraft penalty fees as a way to borrow, or otherwise lack access to affordable credit. Being able to borrow from their bank or credit union could improve these consumers’ suite of options and financial health, and keep them in the financial mainstream: The average payday loan customer borrows $375 over five months of the year and pays $520 in fees,6 while banks and credit unions could profitably offer that same $375 over five months for less than $100.

Yet while 81 percent of payday loan customers would prefer to borrow from their bank or credit union if small- dollar installment loans were available to them there,7 banks and credit unions do not offer such loans at scale today primarily because regulators have not issued guidance or granted specific regulatory approvals for how banks and credit unions should offer the loans. The CFPB appropriately issued strong final rules in October 2017 for loans lasting 45 days or less, removing some of the regulatory uncertainty that discouraged banks and credit unions from offering installment loans and lines of credit.8 Because of the investment involved in launching a new product, and concern on the part of banks and credit unions about enforcement actions or negative reports from examiners, these traditional banking institutions will need clear guidance or approvals from their primary regulators—the OCC, the Federal Reserve, the FDIC, and the NCUA—before they develop small-loan products.

Experience with small-dollar loan programs suggests losses will be low. For example, over the past decade, certain banks and credit unions offered small-dollar loans under three regulated programs—the NCUA Payday Alternative Loan program, the FDIC small-dollar loan pilot, and the National Federation of Community Development Credit Unions pilot—and collectively they charged off just 2 to 4 percent of those loans.9 Several providers, including Rio Grande Valley Multibank, Spring Bank, Kinecta Federal Credit Union, and St. Louis Community Credit Union’s nonprofit partner Red Dough, have already adopted Pew’s recommendation to set individual payments at no more than 5 percent of each paycheck, and all have found charge-off rates to be manageable.10

The following attributes distinguish safe loans from those that put borrowers at risk and should be used to evaluate bank and credit union small-loan offerings.

Payment size

When making small loans to customers with poor credit scores, lenders typically obtain access to borrowers’ checking accounts to help ensure repayment. While this helps lenders make credit available to more consumers by minimizing the risk that they will not get repaid, it also puts consumers at risk that lenders will take such large payments from their accounts that they will be unable to afford other expenses. This has been a pervasive problem in the market for payday, auto title, and deposit advance loans.

Extensive research, both in borrower surveys and in analysis of installment loan markets serving customers with low credit scores, shows that these borrowers can afford payments of around 5 percent of their gross paychecks11 (or a similar 6 percent of net after-tax income). Using this threshold as a standard for affordable payments would help protect consumers whenever lenders take access to their checking accounts as loan collateral, while also providing a clear and easy-to-follow guideline that works well for lenders. To improve operational efficiency and keep costs down, banks and credit unions can assess customers’ income based on deposits into checking accounts and automatically structure loans to have affordable payments that take no more than 5 percent of each gross paycheck or 6 percent of deposits into accounts.12 This payment size is sufficient for borrowers to pay down their balances—and for lenders to be repaid—in a reasonable amount of time.

Pricing and competitive factors

Small-loan markets serving customers with very low credit scores are competitive on many elements, but generally speaking not on price13—because those seeking this credit are in financial distress and focus primarily on speed, likelihood of approval, and ease of application.14 To succeed in this market, any bank or credit union program must be competitive on these essential features. If banks and credit unions can achieve that, then they could leverage their strong competitive advantage by being able to offer loans profitably at much lower prices.

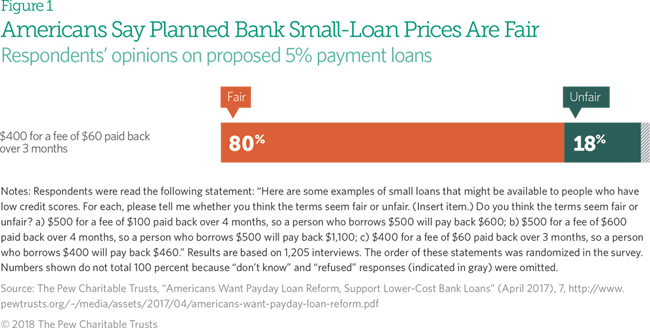

The payday loan market is typically characterized by 400 percent APRs, but banks and credit unions can be profitable at double-digit APRs as long as applicable rules allow for automated origination.15 These APRs for small loans borrowed for short periods of time need not be as low as the APRs for credit-card debt to be broadly viewed as fair. For example, 80 percent of Americans think that a $60 charge for a $400, three-month loan is fair, though its APR is 88 percent.16 (See Figure 1.) That $60 cost is roughly six times lower than average payday loan pricing for the same loan. But bank or credit union loans or lines of credit with three-digit APRs should attract additional regulatory scrutiny—because those rates are unnecessary for profitability, because they may be indicative of inadequate underwriting, and because the public sees them as unfair, meaning that they could create reputational risk for a bank or credit union. And APRs should decline as loan sizes increase, because the relatively high APRs needed for very small loans to be profitable are not justified for larger loans.

Any fees charged, other than a small application or annual fee, should be charged monthly, in order to be spread evenly over the life of the loan. Such a structure does not penalize borrowers who repay early or create an incentive for lenders to refinance loans.

Repayment term

Few borrowers can afford to repay small loans in just a few weeks. At the same time, some payday lenders have set unreasonably long terms to earn more revenue, such as 18 months to repay $500.17 The CFPB’s final small- loan rule takes the important step of steering the market toward terms of more than 45 days. To ensure that loan sizes and durations do not become excessive, some regulators and state lawmakers have set maximum terms for various loan programs, such as six months. A more flexible approach would be to ensure that the total cost of a small-dollar bank or credit union loan never exceeds half of the loan principal, which would discourage lenders from setting terms that are too long—because they cannot earn additional revenue from doing so. At the same time, such a limit would allow for terms long enough to accommodate loans larger than $1,000 (the average size of an auto title loan).

Providers should be free to experiment with both installment loans and lines of credit, as long as all of the safeguards described in this brief are included. Some consumers, such as those who need to make a substantial purchase or handle an unusually large expense, may be more likely to repay under the discipline imposed by installment loans. For consumers facing income volatility, the flexibility offered by lines of credit could be a better fit.

Automation

The cost of manually processing applications is too high to offer small loans at scale. So, to keep the cost of origination low—and to compete with nonbank lenders on speed and ease—banks and credit unions will need to largely automate the lending process, including determining eligibility, establishing the maximum loan size, processing applications, and disbursing funds. Some additional time would be required for banks or credit unions to process loan applications from people who are not already their customers, but the financial institutions may find it worthwhile to do so since it would mean acquiring new accountholders.

Underwriting

As highly regulated institutions, banks and credit unions engage in underwriting to ensure that they are lending in a safe and sound manner. The underwriting criteria for small-dollar installment loans must be carefully tailored so that these loans can be competitive with more expensive options such as payday, auto title, or rent-to-own loans.

The guidelines must allow for prescreening, high approval rates,18 and fast origination at very low cost, similar to those employed for overdraft programs and other automated systems; otherwise, the provider would have to charge a high price to be profitable.

Prescreening customers to determine eligibility can improve the likelihood that the loans are advertised only to customers who are likely to be approved. Among customers with damaged credit, traditional metrics such as a credit score are limited in their effectiveness at assessing the likelihood of loan repayment. Therefore, relying primarily on a credit score to determine eligibility is likely to deny access to these customers, many of whom would otherwise use high-cost products. To mitigate this issue, providers should be able to experiment with underwriting criteria. Important elements are likely to include whether the customer is maintaining an account in good standing; the length of the customer’s relationship with the bank or credit union; regularity of deposits; and the absence of any warning signs such as recent bankruptcies or major problems with overdrafts (a small installment loan would be better for most customers than paying several overdraft fees, but very heavy and persistent overdrawing could indicate deeper financial troubles that would make further extension of credit unwarranted). At the same time, if criteria are too strict, banks and credit unions may be unable to serve customers who could most benefit from small credit, leaving them with more costly nonbank options.

Providers will necessarily underwrite differently when lending to people who are not current customers but are joining the credit union or bank specifically because of its small-loan offerings. Regulators should leave banks and credit unions the flexibility to adjust their underwriting to ensure that losses remain manageable, while also making loans available to customers who would otherwise turn to high-cost lenders or suffer adverse outcomes because they could not borrow. For loans with terms of just a few months, annualized loss rates may look high compared with conventional credit products, but that should not be cause for concern as long as the absolute share of loans charged off is not excessive.

Credit reporting

Loans should be reported to credit bureaus so that borrowers can build a track record of successful repayment, which in turn could help them qualify for lower-rate financial products. To maximize customer success, borrowers should be automatically placed into electronic payments that coincide with days they are likely to have incoming deposits, which keeps losses lower for providers and increases the odds that customers will succeed. Customers must have a chance to opt out of electronic repayment and pay manually if they prefer.

Convenience

In order to attract customers from payday and other high-cost lenders, banks and credit unions must offer loans that are at least as convenient. With sufficient automation, the loans can be far easier and faster to obtain than those from nonbank lenders. The pre-existing relationship between the bank or credit union and customer means the applications can be started through an online or mobile banking platform, with the funds deposited quickly into checking accounts. Applying for credit and receiving it electronically can be especially helpful to customers who seek credit outside of normal banking hours or who do not live near a branch of their bank or credit union.

If, on the other hand, banks and credit unions offer loans that—while at a lower cost than those available through payday and other lenders—are not as fast or convenient, many customers will continue to leave the banking system to borrow money.

Other safeguards

The characteristics described above would make small loans far safer than those available from payday and other nonbank lenders. But three additional protections can benefit consumers further, without discouraging banks and credit unions from lending:

- To ensure that loans are made in a safe and sound manner only to customers who have the ability to repay them, providers should ensure that no more than 1 in 10 loans defaults. There may be valid reasons for high default rates during downturns or after natural disasters, but if more than 1 in 10 loans consistently defaults, lenders should change their loan policies and practices so at least 9 in 10 customers succeed.19

- Small-dollar loans from banks and credit unions should not trigger overdraft or nonsufficient funds fees, which today are charged when payday and other nonbank loans overdraw accounts. This protection is feasible for traditional financial institutions because they both operate the checking account and service the loan. If a lender accidentally charges such a fee, the customer should receive a prompt refund.

- Each lender should ensure that it is extending only one small loan at a time to each customer.20 If customers repay as agreed, they should be able to borrow again.

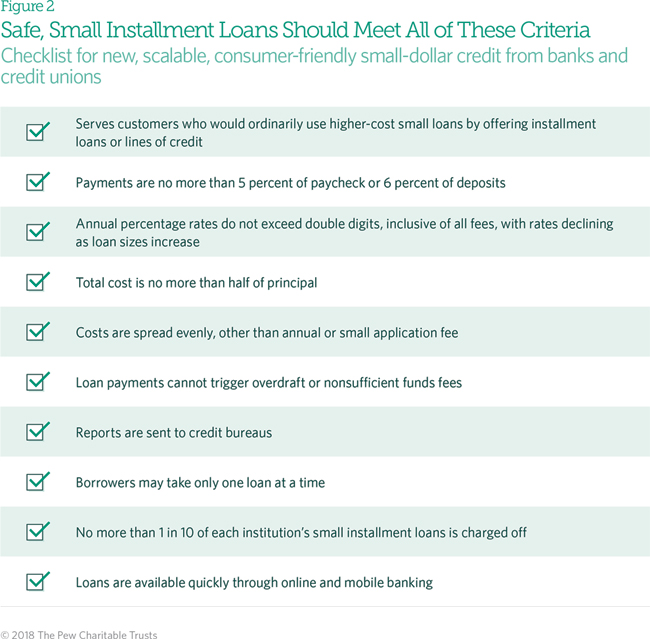

Figure 2 identifies the features that would make high-volume offerings of small installment loans and lines of credit from banks and credit unions safe. Programs that use automation and seek to achieve scale should meet all of these criteria. Existing, low-cost, ad hoc, or low-volume programs from community banks and credit unions that are not automated tend to have many consumer-friendly features, though they do not meet all of these criteria.

Conclusion

For too long, consumers who are struggling financially have had poor options when they seek to borrow small sums of money. These consumers are mostly bank and credit union customers, and it is imperative for their financial health that regulators, banks, credit unions, and other stakeholders find a way for them to gain access to better credit than that offered at high cost by nonbank lenders. Seventy percent of Americans report that they would have a more favorable view of their bank or credit union if it offered a $400, three-month loan for $60, and 80 percent believe that such a loan is fair21—as do 86 percent of payday loan borrowers.22 Around this price point, 90 percent of current payday loan customers would rather borrow from a bank or credit union.23 Numerous banks and credit unions are interested in offering small loans with the consumer-friendly characteristics laid out in this brief. With clear guidelines from regulators, that credit could reach the market and millions of Americans who are using high-cost loans today could save billions of dollars annually.

- The Pew Charitable Trusts, ”Payday Lending in America: Who Borrows, Where They Borrow, and Why” (July 2012), 4, http://www.pewtrusts.org/~/media/legacy/uploadedfiles/pcs_assets/2012/ pewpaydaylendingreportpdf.pdf; Center for Financial Services Innovation, ”2016 Financially Underserved Market Size Study” (November 2016), http://cfsinnovation.org/wp-content/uploads/2016/11/2016-Financially-Underserved-Market-Size-Study_Center-for-Financial-Services-Innovation.pdf .

- Federal Deposit Insurance Corp., ”2015 FDIC National Survey of Unbanked and Underbanked Households” (October 2016), https://www.fdic.gov/householdsurvey/2015/2015report.pdf .

- The Pew Charitable Trusts, ”Payday Lending in America: Policy Solutions” (October 2013), http://www.pewtrusts.org/~/media/legacy/uploadedfiles/pcs_assets/2013/ pewpaydaypolicysolutionsoct2013pdf; Luigi Zingales, ”Does Finance Benefit Society?” (January 2015), http://faculty.chicagobooth.edu/luigi.zingales/papers/research/finance.pdf.

- The Pew Charitable Trusts, ”Payday Lending in America: Policy Solutions,” 28.

- The Pew Charitable Trusts, ”Payday Lending in America: Fraud and Abuse Online” (October 2014), 4–7, http://www.pewtrusts.org/~/media/assets/2014/10/payday-lending-report/fraud_and_abuse_online_harmful_practices_in_internet_payday_lending.pdf.

- The Pew Charitable Trusts, ”Payday Lending in America: Who Borrows,” 8.

- The Pew Charitable Trusts, “Payday Loan Customers Want More Protections, Access to Lower-Cost Credit From Banks” (April 2017), 6, http://www.pewtrusts.org/~/media/assets/2017/04/payday-loan-customers-want-more-protections .

- Consumer Financial Protection Bureau, ”Payday, Vehicle Title, and Certain High-Cost Installment Loans” (November 2017), https://www.federalregister.gov/documents/2017/11/17/2017-21808/payday-vehicle-title-and-certain-high-cost-installment-loans .

- Nick Bourke, “Why Credit Unions Should Watch the Payday Loan Market,” Credit Union Times, Dec.4, 2015, http://www.cutimes.com/2015/12/04/why-credit-unions-should-watch-the-payday-loan-mar ; Federal Deposit Insurance Corp., “The FDIC’s Small-Dollar Loan Pilot Program: A Case Study After One Year,” FDIC Quarterly 3, no.2 (2009): 29–38, https://www.fdic.gov/bank/analytical/quarterly/2009-vol3-2/smalldollar.pdf ; National Federation of Community Development Credit Unions, ”Borrow & Save: Building Assets With a Better Small-Dollar Loan” (July 2013), http://cdcu.coop/wp-content/uploads/2013/03/Borrow-and-Save-Final-July-30-2013.pdf.

- The Pew Charitable Trusts, Oct.7, 2016, comment letter to Director Richard Cordray regarding “Proposed Rule for Payday, Vehicle Title, and Certain High-Cost Loans, Docket ID: CFPB-2016-0025,” 28, https://www.regulations.gov/document?D=CFPB-2016-0025-142716.

- 11. Ibid., Appendix C.

- To gain a more complete financial picture, providers may wish to ask the applicant to state his or her income on the loan application, especially for joint accounts, but payment size should be determined using verified income or deposits, not stated income.

- The Pew Charitable Trusts, “How State Rate Limits Affect Payday Loan Prices” (April 2014), http://www.pewtrusts.org/~/media/legacy/uploadedfiles/pcs/content-level_pages/fact_sheets/stateratelimitsfactsheetpdf.pdf.

- Elevate Credit Inc., Form S-1 (2017), 119, http://otp.investis.com/clients/us/elevate_inc1/SEC/sec-show.aspx?Type=html&FilingId=11981715&CIK=0001651094&Index= 10000#D310075DS1A_HTM_TOC310075_14; Veritec Solutions LLC, “Competition Commission Payday Lending Market Investigation” (2013), 10–11, http://docplayer.net/9461788-Competition-commission-payday-lending-market-investigation-submission-from-veritec-solutions-llc.html.

- Ian McKendry, “Banks’ Secret Plan to Disrupt the Payday Loan Industry,” American Banker, May 6, 2016, http://consumerbankers.com/cba-media-center/cba-news/banks-secret-plan-disrupt-payday-loan-industry.

- The Pew Charitable Trusts, “Americans Want Payday Loan Reform, Support Lower-Cost Bank Loans” (April 2017), 7, http://www.pewtrusts.org/~/media/assets/2017/04/americans-want-payday-loan-reform.pdf.

- The Pew Charitable Trusts, “From Payday to Small Installment Loans” (August 2016), 10, http://www.pewtrusts.org/~/media/assets/2016/08/ from_payday_to_small_installment_loans.pdf.

- Although providers’ underwriting criteria will vary, they should all target loans to customers who are likely to be approved and make those loans available via online or mobile banking so that customers do not become discouraged and turn to high-cost lenders.

- This recommendation refers to the proportion of loans defaulting, but it intentionally does not use annualized loss rates to measure that share. Annualizing losses on short-term loans, but not outstanding balances, tends to yield a high annualized default rate even when relatively few loans go unpaid.

- Pew intends this recommendation to ensure that banks or credit unions do not issue more than one loan at a time to each borrower, but that does not mean that, when using third-party vendors, these lenders should be required to check the records of other providers using the same vendor.

- The Pew Charitable Trusts, “Americans Want Payday Loan Reform,” 4, 7.

- The Pew Charitable Trusts, “Payday Loan Customers Want More Protections,” 11.

- 23. Ibid., 7.

Payday Loan Customers Want More Protections

Results of a nationally representative survey of U.S. borrowers

How to Fix Payday Loans

Americans Want Payday Loan Reform

Results of a nationally representative survey of U.S. adults