Demographic Overview of Illinois Secure Choice Program Population

Survey shows program reaching populations that historically lack workplace access to retirement savings

Overview

Almost half of Americans aged 18 to 64 who work in the private sector lack access to a workplace retirement savings plan.1 The most common reason employers give for not having started a plan is that they view setup to be too expensive and burdensome.2

In response, states are implementing programs with automatic enrollment into individual retirement accounts (IRAs) for private sector workers who don’t have access to workplace retirement savings plans. Oregon was the first state to adopt such a program, followed in order by Illinois, California, Connecticut, Maryland, Colorado, and Virginia; all are actively enrolling savers into such programs. Delaware, Hawaii, Maine, Minnesota, Nevada, New Jersey, and New York have authorized automatic savings programs and will be enrolling savers in the years to come.3

To understand the participant experience in these automatic savings programs, the RAND Corporation conducted for The Pew Charitable Trusts a series of representative random sample surveys with adults eligible to participate in Illinois Secure Choice—a program that launched in 2018 and allows workers to automatically save a portion of each paycheck in an IRA. Workers can change their contribution rate or opt out of the program at any time.

This analysis presents self-reported demographics of respondents who completed the baseline survey conducted from March to May 2020 (see the methodology section for additional details); the results are representative of workers enrolled in the program as well as those who opted out. The analysis also looks at how the demographic distribution of those in Illinois Secure Choice compares with that of all Illinois private sector wage workers at similar size firms.

The results show that Illinois Secure Choice is working as intended: by providing access to workplace savings for workers who have traditionally not been covered by employer-sponsored retirement plans. And groups that not only have lacked access—but also have had comparably lower participation rates in employer-sponsored plans when they do have access to such plans—are in many cases enrolling in Illinois Secure Choice at rates comparable to, or higher than, other groups who have enrolled in the program. Among other key trends:

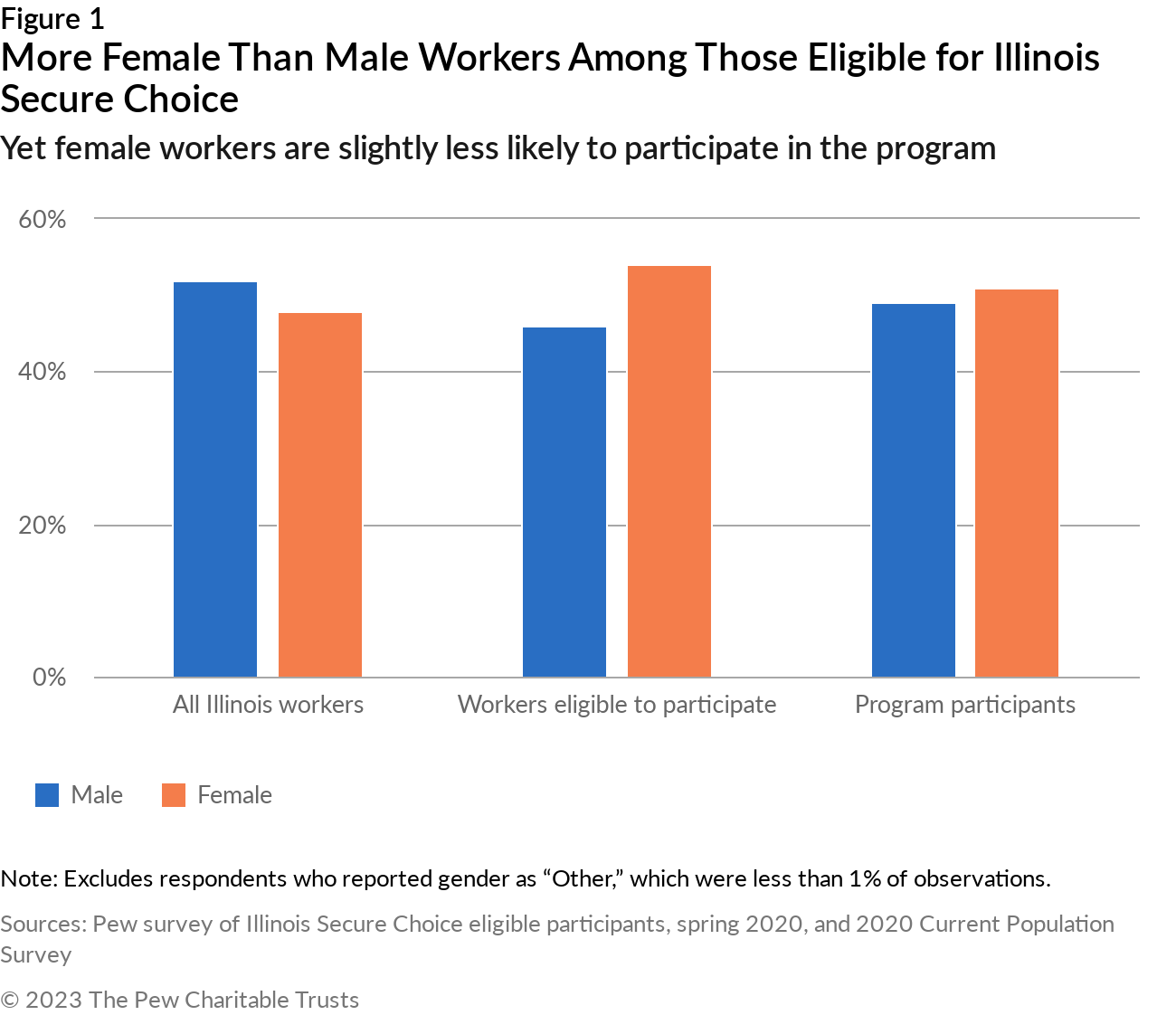

- More female than male workers are eligible to participate in Illinois Secure Choice, perhaps because women are more likely than men to work in part-time jobs—and many employer-sponsored plans are not available to part-time workers. Despite this greater access to Illinois Secure Choice, women are slightly less likely to participate in the program than men, potentially because of underlying differences in income.

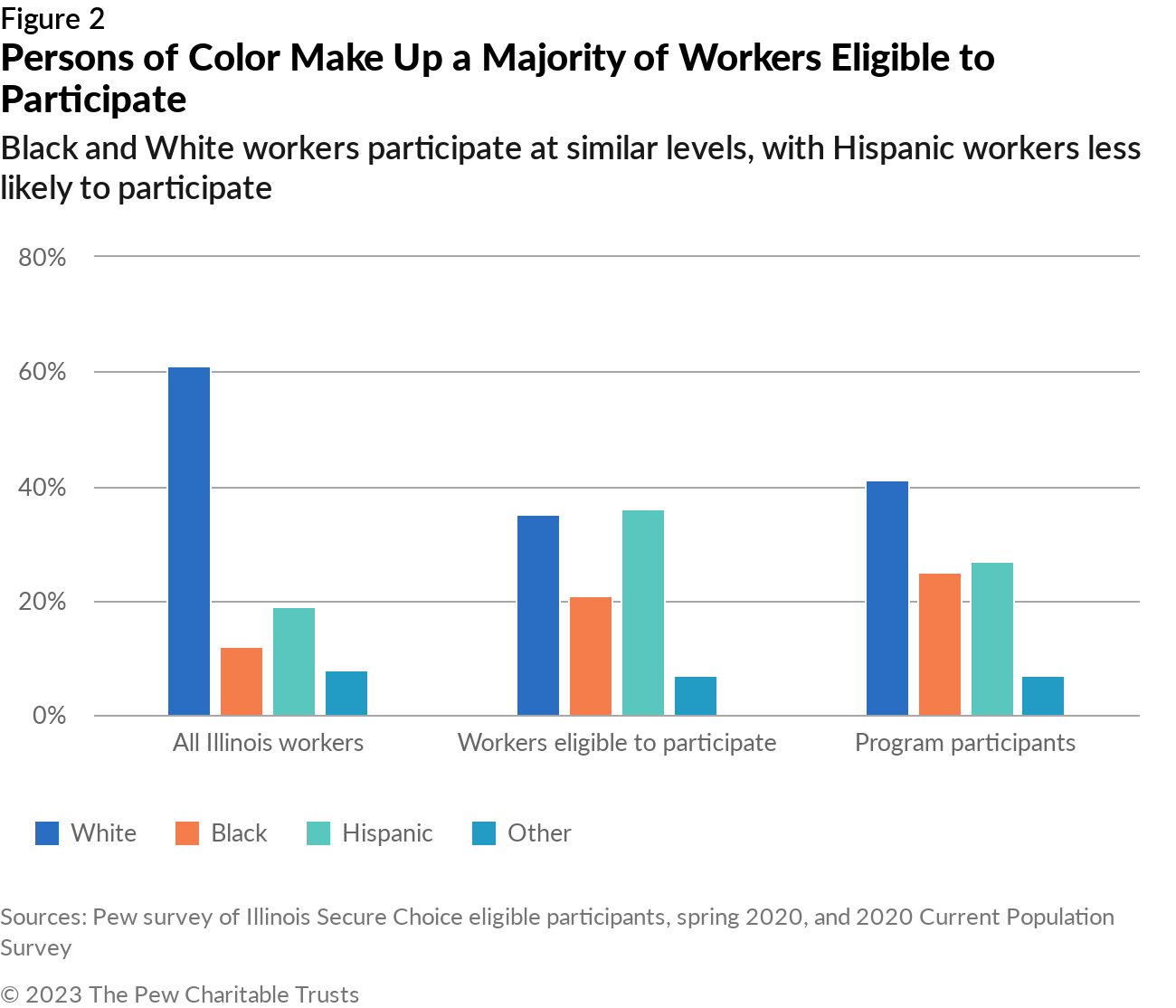

- A majority of people eligible for Illinois Secure Choice are workers of color. While Hispanic workers are less likely to participate in the program than are other workers eligible for the program—a trend that mirrors Hispanic participation rates in employer-sponsored plans—Black workers (as well as White workers) are more likely to participate than other eligible workers.

- Workers eligible for Illinois Secure Choice are comparably younger and have lower levels of educational attainment than the pool of all Illinois workers. Workers under age 35 also make up a larger share of Illinois Secure Choice participants than their share of those eligible for the program, while workers at each level of education are participating at rates similar to those at other levels of education. Both trends are a marked difference from participation in employer-sponsored plans, in which older workers and those with higher levels of educational attainment are more likely to participate than younger workers and those with lower levels of educational attainment.

- Both the program-eligible population and those who participate in the program are disproportionately—when compared with all Illinois private sector workers—made up of workers who are single and do not have dependents under the age of 18.

Gender

More female workers (54%) than male workers (46%) are eligible to participate in Illinois Secure Choice. In fact, the share of workers eligible to participate in the program who are female is higher than the share of private sector workers in the state who are female (48%). Although previous research has shown that men and women who work full time have similar access to workplace plans, the share of women who work part time is higher—which can prevent participation in many employer-sponsored plans that bar part-time workers.4 Illinois Secure Choice, on the other hand, includes both full- and part-time workers. Among the eligible population for Illinois Secure Choice, 38% of women report that their primary job is part time, compared with 27% of male workers.

Even though there are more female than male workers eligible to participate in the program, women are slightly less likely to participate than men.5 These dynamics lead to a relatively even gender split among Illinois Secure Choice participants (51% women and 49% men). Although the data does not allow for an explanation of this small participation gap, prior research indicates that underlying wage differences can account for differences in participation workplace retirement plans.6

Race and ethnicity

Black and Hispanic workers represent the majority of the program’s eligible population and about half of all program participants. Black workers comprise 21% of all eligible workers and are 12% of all Illinois workers, while Hispanic workers represent 36% of all eligible participants and are 19% of all workers statewide.

The percentage of workers in Illinois Secure Choice who are either White or Black (41% and 25%, respectively) is higher than the percentage of workers eligible for the program who are White or Black, while Hispanic workers represent a smaller share of program participants (27%) than their share of workers eligible to participate.7 This trend means that White and Black workers are participating at comparably higher rates than Hispanic workers and is noteworthy because both Black and Hispanic participation in private sector employer-sponsored retirement plans—such as 401(k)s—lags behind the participation of White workers.8 Prior research has cited lower incomes among Hispanic workers as one factor linked to lower Hispanic participation rates in workplace retirement plans.9 Despite lagging participation by Hispanics in Illinois Secure Choice, Hispanic workers still represent a larger share of workers enrolled in the program than they do of all Illinois workers.

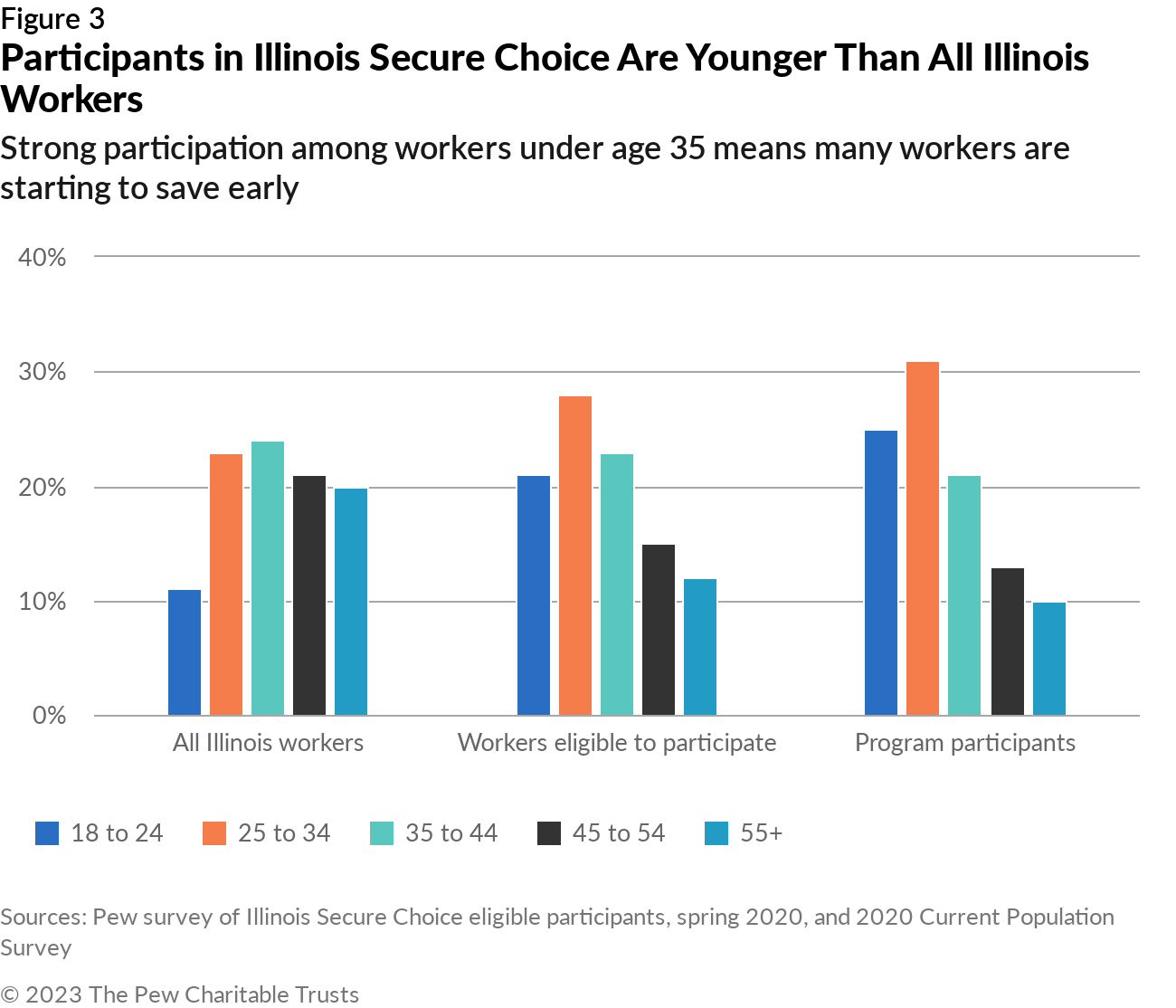

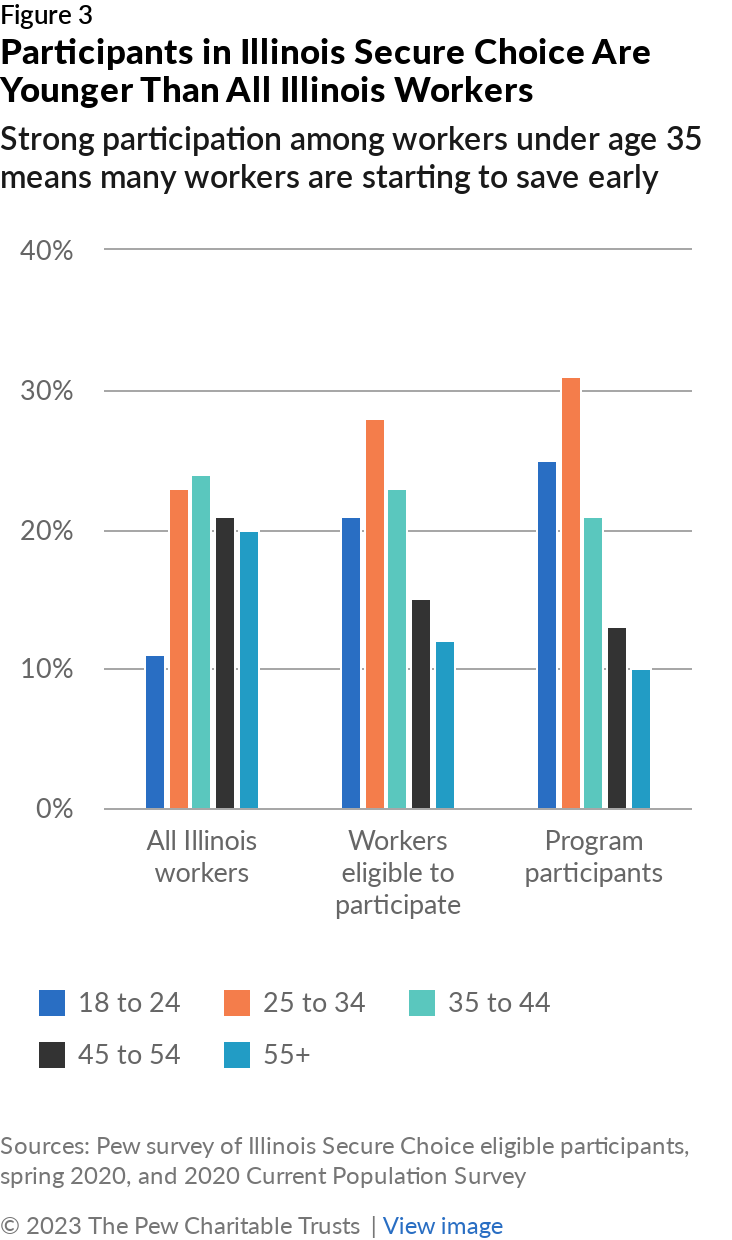

Age

Workers eligible to participate in Illinois Secure Choice are comparatively younger than the Illinois working population; the median age of program eligible workers is 35, compared with 41 for all workers in the state. This makes sense, because access to workplace savings in employer-sponsored plans is lower for workers under the age of 30 than for any other age group.10

And not only is access to private sector workplace savings plans lower for workers under the age of 30 than for other workers, the participation rate in these plans is lower among this age cohort as well.11 But with Illinois Secure Choice, there’s a strong association between age and participation—with workers younger than 35 comprising a majority of participants in the program. On the other hand, each cohort age 35 and older makes up a comparably smaller share of participants, and they are less likely to participate than younger workers.12 As a result, the median age for Illinois Secure Choice participants is 32, while the median age for those who opted out is 37. This means that many workers in the program are starting to save early and will likely have a more secure retirement as a result.

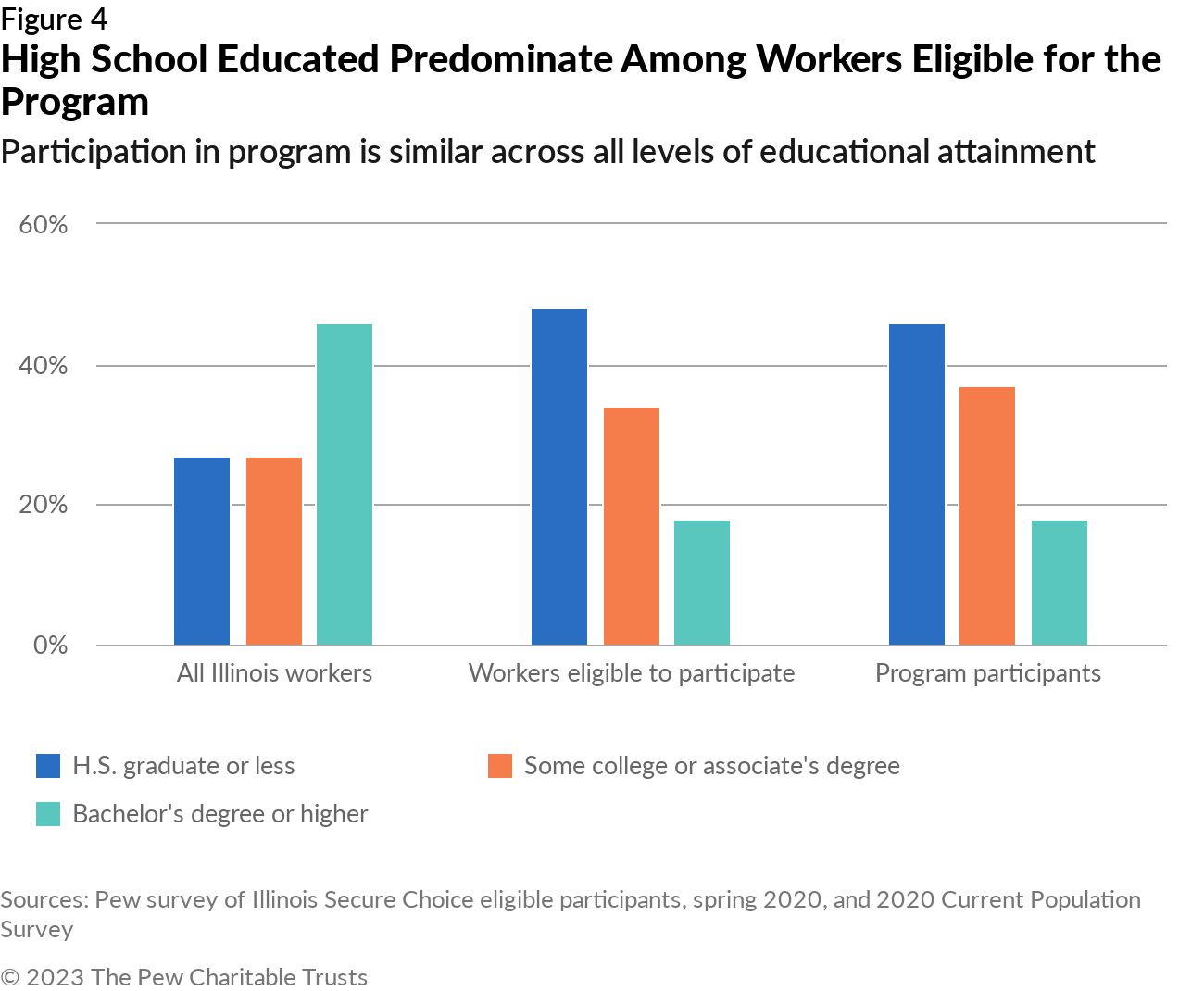

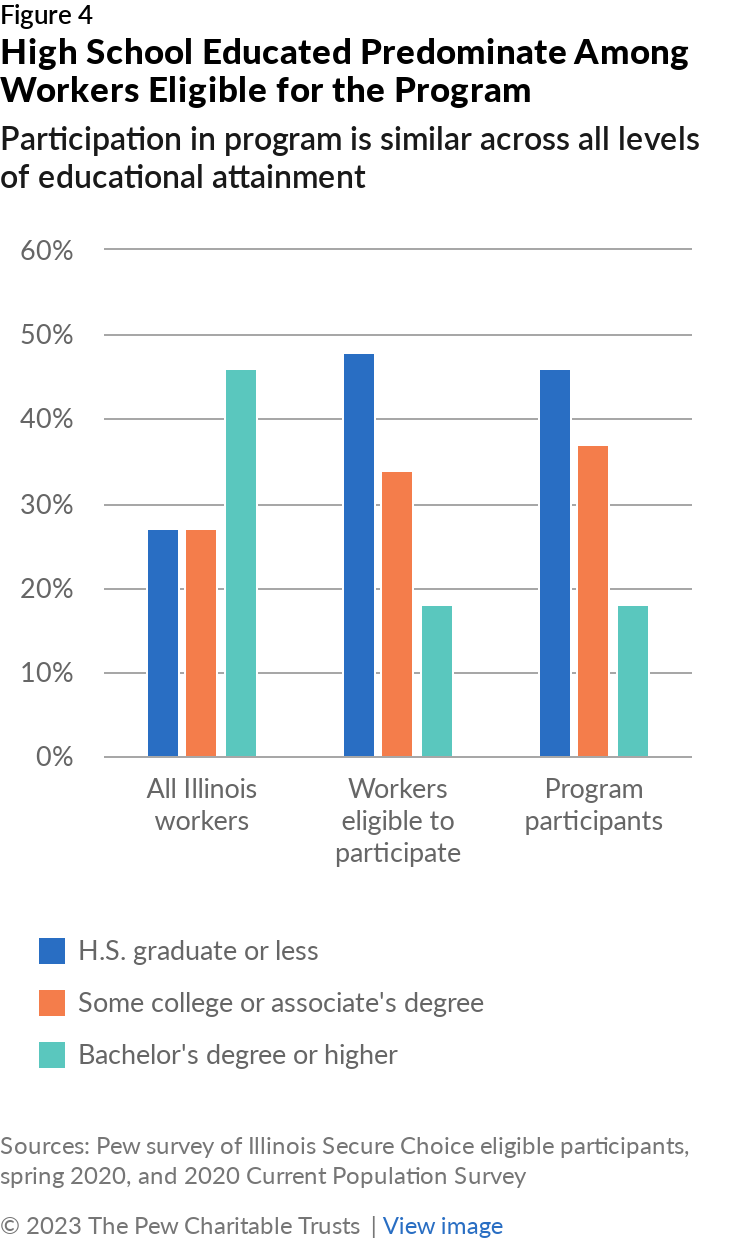

Education

Workers whose formal education stopped with a high school diploma predominate in the Illinois Secure Choice program eligible population, with almost half (48%) reporting having a high school degree or less. This group also comprises 46% of program participants compared with only 27% of all Illinois workers.

The education levels of workers enrolled in the program appear similar to the population of those eligible for the program. Although the share of program participants with a high school diploma or less is slightly smaller than the share of program-eligible workers with a high school diploma or less—and the share of program participants with some college or an associate’s degree is slightly larger than the share of program-eligible workers with some college or an associate’s degree—this small association between education and participation is not statistically significant.13 In employer-sponsored plans, those with a bachelor’s degree or higher participate at higher rates than those without at least a bachelor’s degree, so it’s notable that participation in Illinois Secure Choice does not show a significant variance among workers with differing levels of educational attainment.14

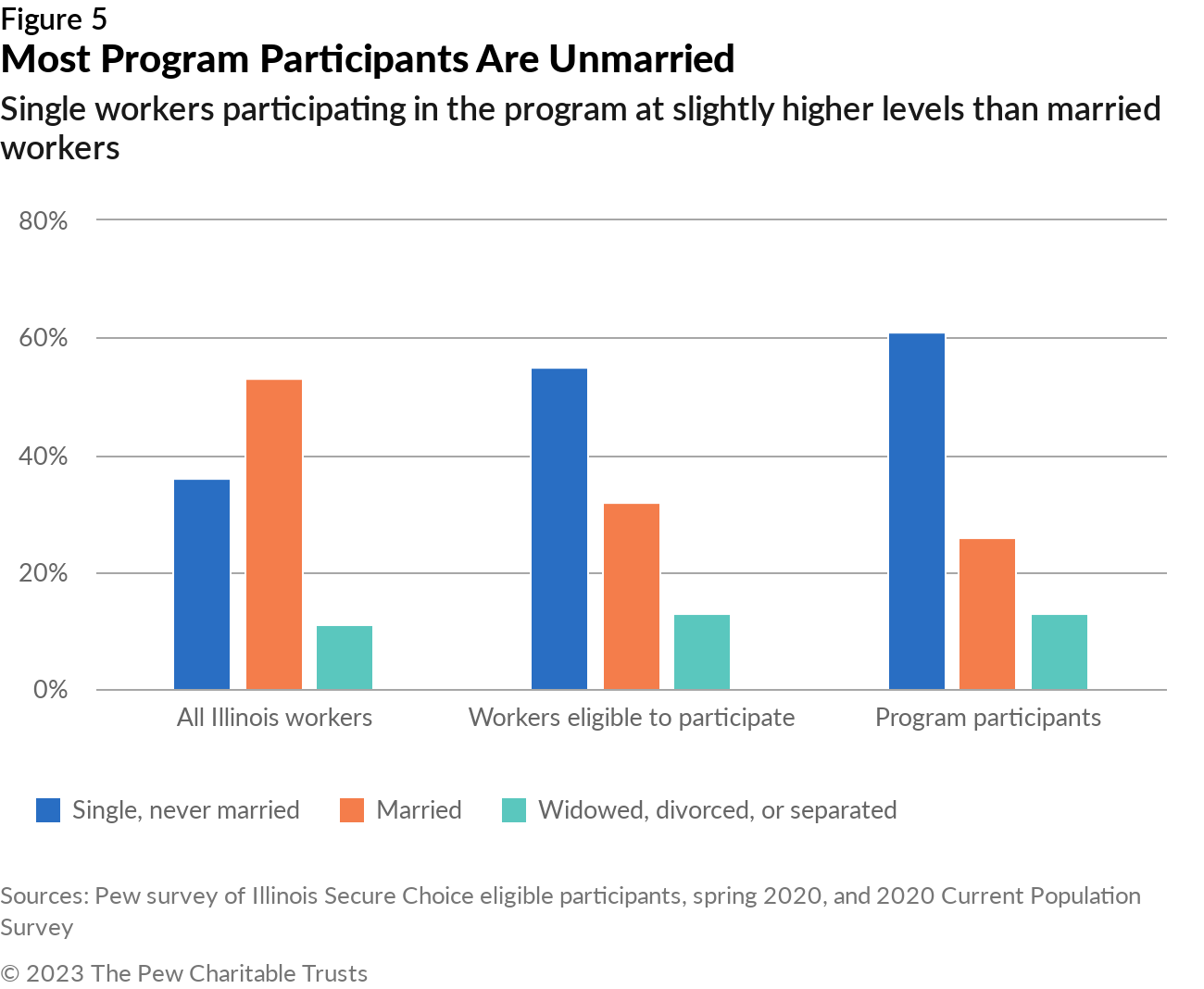

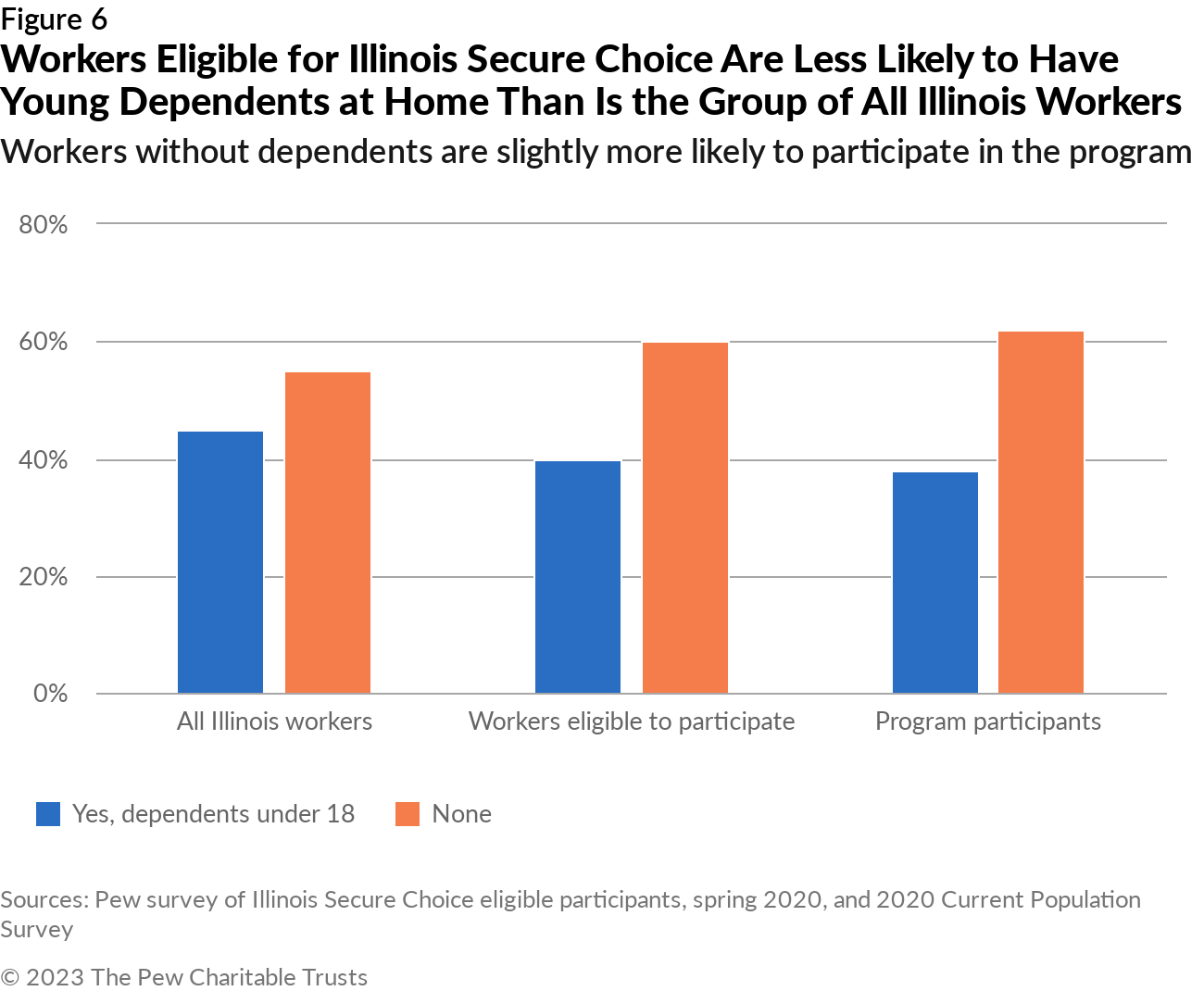

Marital status

Workers who have never been married comprise the majority (55%) of Illinois Secure Choice’s eligible population—the opposite of all Illinois workers, of whom a majority (53%) are married. This is not particularly surprising, given that the program-eligible population is younger than the cohort of all Illinois workers. Married workers are less likely than single workers to participate in Illinois Secure Choice: Workers who are married make up a larger share of those who opted out relative to their share of all eligible workers, while single workers represent a larger proportion of program participants relative to their share of eligible workers.15

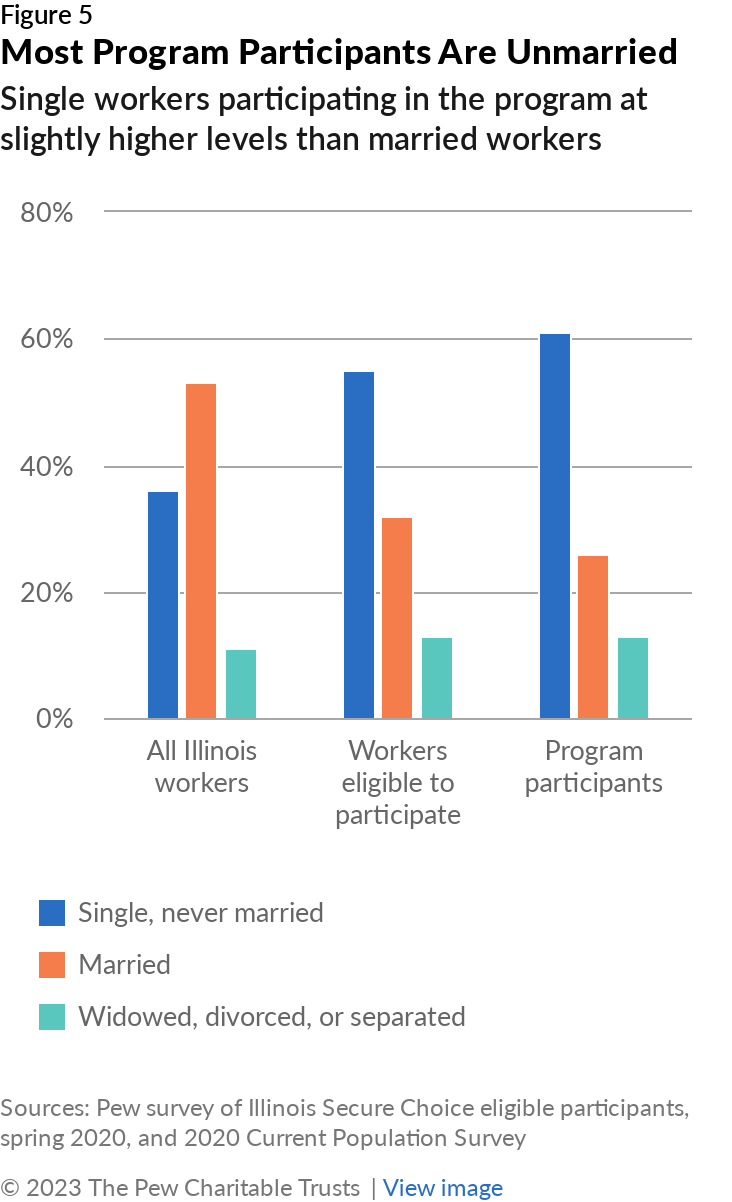

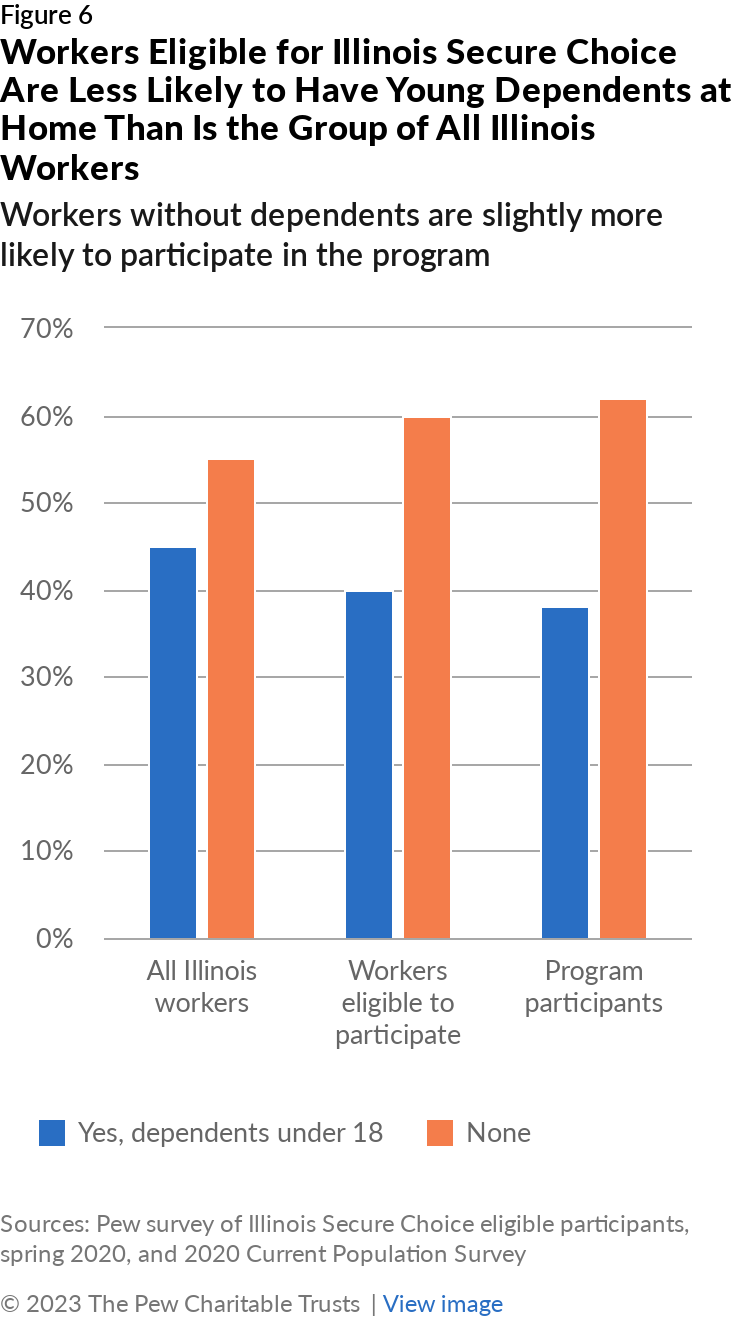

Dependents under the age of 18 at home

A smaller proportion of workers eligible for Illinois Secure Choice (40%) have dependents under the age of 18 than among all Illinois workers (45%). Workers without dependents appear slightly more likely to participate in the program than workers with dependents: Compared with the distribution of workers eligible for the program, workers with dependents represent a slightly larger share of those who opted out of the program, while those without dependents represent a slightly larger share of program participants.16 This trend is consistent with the finding about eligibility and participation by marital status; since single workers are more likely to participate in Illinois Secure Choice than married workers are, it makes sense that fewer program participants have young dependents.

Conclusions

Illinois Secure Choice, an early pioneer of state automated savings programs, is providing access to workplace savings for demographic groups that have traditionally been left out of employer-sponsored coverage—and, as a result, typically do not save for retirement. And, because these automated savings programs allow workers to withdraw their contributions for nonretirement needs, such as unexpected expenses or sudden loss of income, these programs also have the potential to strengthen participants’ overall economic stability and ability to save for retirement over time. Workers of color, workers under the age of 35, and workers who have a high school diploma or less are all represented in large numbers among those eligible to participate in the program. Eligible workers are also more likely to be single than married, and more likely not to have any dependents under the age of 18 than to have such dependents. A larger proportion of workers eligible for Illinois Secure Choice are female rather than male, likely a result of women working part time in greater numbers than men; auto-IRAs such as the Illinois program provide access to workplace savings for both full- and part-time workers, while many workplace plans such as 401(k)s are open to full-time employees only.

Beyond these groups having greater access than they would through private sector employer-sponsored plans, certain groups appear more likely to participate in Illinois Secure Choice than in employer-sponsored plans. For example, although female workers have greater access to the program, male workers are slightly more likely to participate, potentially due to underlying wage differences. And although Black workers have lower participation in employer plans than White workers, Black workers comprise a larger share of workers participating in Illinois Secure Choice compared with all workers eligible for the program. However, Hispanic workers make up a smaller proportion of participants compared with those eligible, a trend that is similar to Hispanic participation in employer plans and potentially linked to lower incomes. To counter these trends, outreach and marketing may have to be tailored to female workers and Hispanic households. However, since these participation trends are likely linked to underlying wage differences, broader policies aimed at improving wages may be necessary to improve program participation.

Workers under the age of 35 are more likely to participate in Illinois Secure Choice than workers over 35, while participation among those without a bachelor’s degree is similar to that of those with at least a bachelor’s degree. The participation by younger workers is especially encouraging given that their modest levels of contributions in Illinois Secure Choice now will give them a longer period for compounding of investment returns than if they had waited until after age 35 to begin contributing.

Not only is the program fulfilling its goal of increasing savings for those who have traditionally had trouble accessing employee savings programs, workers who have disproportionately opted out of participating in other workplace plans are participating in Illinois Secure Choice. The trends are promising and demonstrate that there is an appetite for saving for retirement among populations that have traditionally not done so when convenient mechanisms are available.

Methodology

To gain a better understanding of the Illinois Secure Choice program demographics, Pew analyzed an original survey of the program’s eligible participants. The RAND Corporation conducted a series of surveys for Pew with adults eligible to participate in Illinois Secure Choice, reaching out to a representative sample of workers enrolled in the program as well as those who had opted out. The survey was conducted in three waves at roughly six-month intervals from March 2020 through April 2021. For more details on the survey’s methodology, please see the downloadable methodology statement. This brief looks at findings for respondents who completed the baseline survey conducted from March to May 2020. Among respondents, “participants” are those who were enrolled in the program at the time the sample was drawn in February 2020.

For the comparison to Illinois workers, Pew analyzed 2020 data from the Current Population Survey, sponsored by the U.S. Census Bureau and the U.S. Bureau of Labor Statistics. The data was limited to adult private sector wage and salary workers at employers that had at least 25 workers. Although Illinois Secure Choice started covering employers with five or more employees at the start of 2022, only employers of at least 25 employees were covered by the program at the time that eligible participants were surveyed.

Endnotes

- D. John, G. Koenig, and M. Malta, “Payroll Deduction Retirement Programs Build Economic Security” (AARP Public Policy Institute, 2022), https://www.aarp.org/content/dam/aarp/ppi/2022/07/payroll-deduction-retirement-programs-build-economic-security.doi.10.26419-2Fppi.00164.001.pdf.

- The Pew Charitable Trusts, “Employer Barriers to and Motivations for Offering Retirement Benefits” (2017), https://www.pewtrusts.org/-/media/assets/2017/09/employer_barriers_to_and_motivations.pdf.

- For a review of legislative activity at the state level, see Center for Retirement Initiatives, “State Programs 2023: More Programs Are Open and Enrolling Workers, Smaller States Actively Explore Partnership Opportunities, While Other States Continue to Introduce Legislative Proposals,” accessed March 22, 2023, https://cri.georgetown.edu/states/.

- The Pew Charitable Trusts, “Who’s In, Who’s Out: A Look at Access to Employer-Based Retirement Plans and Participation in the States” (2016), https://www.pewtrusts.org/-/media/assets/2016/01/retirement_savings_report_jan16.pdf.

- A chi square test indicated a statistically significant relationship between gender and program participation (p<0.05).

- Vanguard, “How America Saves 2023” (2023), https://institutional.vanguard.com/content/dam/inst/iig-transformation/has/2023/pdf/has-insights/how-america-saves-report-2023.pdf.

- A chi square test indicated a statistically significant relationship between race and ethnicity and program participation (p<0.0001).

- N. Bhutta et al., “Disparities in Wealth by Race and Ethnicity in the 2019 Survey of Consumer Finances” (Board of Governors of the Federal Reserve System, 2020), https://www.federalreserve.gov/econres/notes/feds-notes/disparities-in-wealth-by-race-and-ethnicity-in-the-2019-survey-of-consumer-finances-20200928.html.

- National Council of La Raza, “Enhancing Latino Retirement Readiness in California” (2015), https://unidosus.org/wp-content/uploads/2021/07/LatinoRetirementReadiness2015.pdf.

- The Pew Charitable Trusts, “Who's In, Who's Out.”

- Ibid.

- A chi square test indicated a statistically significant relationship between age cohort and program participation (p<0.0001).

- A chi square test showed no evidence of an overall systematic relationship between education and participation (p=0.077).

- The Pew Charitable Trusts, “Who's In, Who's Out.”

- A chi square test indicated statistically significant relationship between marital status and program participation (p<0.0001).

- A chi square test indicated a statistically significant relationship between whether a worker has dependents under age 18 at home and program participation (p<0.05).

ADDITIONAL RESOURCES

Opinion