Pew Analysis Shows Access to Workplace Retirement Plans Varies Widely Across States

Big differences among industries, incomes, ages, education, race and ethnicities

Getty Images

Getty ImagesWorkers carrying steel beam in manufacturing plant.

WASHINGTON—Wide differences in access to and participation in employer-based retirement plans exist across states, with variations by employer size and industry type as well as by workers’ income, age, education, race and ethnicity, according to a report released today by The Pew Charitable Trusts.

The report, Who’s In, Who’s Out: A Look at Access to Employer-Based Retirement Plans and Participation in the States, examines the rates of access to and participation in plans in all 50 states and assesses the challenges facing workers and employers in ensuring that Americans have sufficient resources to pay for their retirements.

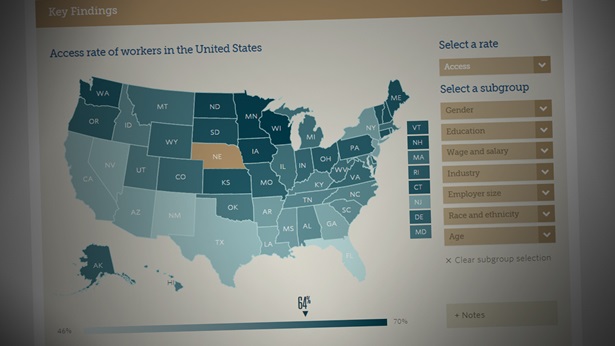

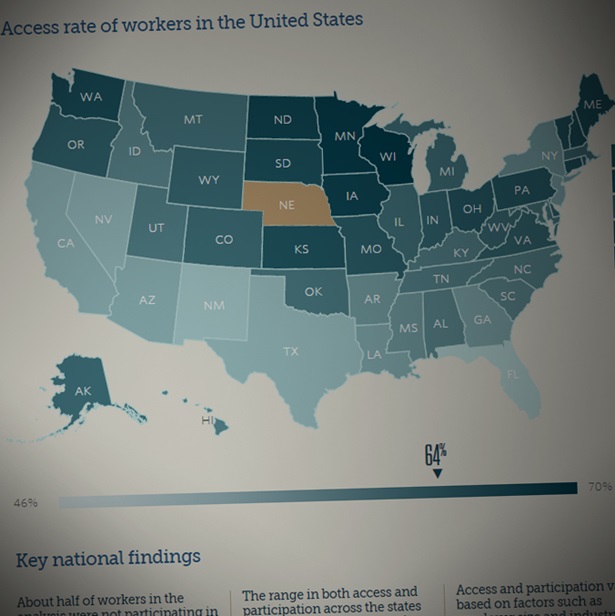

For example, the report found that 61 percent of workers in Wisconsin participate in an employer-based pension or retirement savings plan, compared with 38 percent in Florida. Access and participation is higher in the Midwest, New England, and parts of the Pacific Northwest—and lower in the South and West. The report also finds that among Hispanic workers, access to a plan is around 25 percentage points below that for white non-Hispanic workers. Black and Asian workers also report lower rates of access than white workers.

“Access to workplace retirement plans varies widely across the states,” said John Scott, director of Pew’s retirement savings project. “Recognizing the savings challenge faced by so many Americans, half of the states are looking at their own solutions.”

Overall, Pew’s analysis, based on a pooled version of the Census Bureau’s Current Population Survey (CPS), found that 58 percent of private sector workers have access to a plan, while 49 percent participate in one. Pew also found that more than 30 million full-time, full-year, private sector workers ages 18 to 64 lack access to an employer-based retirement plan, whether a traditional pension or a defined contribution plan such as a 401(k).

The report notes the numerous efforts at the state and federal levels to increase retirement savings. Illinois, for instance, adopted the Secure Choice Savings Program in 2015, which will start enrolling certain private sector workers in new payroll-deduction retirement accounts by 2017. In another example, the state of Washington created a marketplace in which small employers and the self-employed can shop for retirement plans. In addition, the federal government has rolled out the “myRA,” a new national savings program that is geared toward low-income savers.

“Workplace retirement savings plans can be a critical piece of the retirement security puzzle,” said Scott. “But for millions of Americans, this piece is missing.”

More detailed information, including state-by-state breakdowns, is available in the report’s online interactive data visualization at www.pewtrusts.org/retirementaccess.

# # #

The Pew Charitable Trusts is driven by the power of knowledge to solve today’s most challenging problems. Learn more at www.pewtrusts.org.

ADDITIONAL RESOURCES

Article

Article

Article

Explore Pew’s new and improved

Fiscal 50 interactive

Your state's stats are more accessible than ever with our new and improved Fiscal 50 interactive:

- Maps, trends, and customizable charts

- 50-state rankings

- Analysis of what it all means

- Shareable graphics and downloadable data

- Proven fiscal policy strategies

Welcome to the new Fiscal 50

Key changes include:

- State pages that help you keep track of trends in your home state and provide national and regional context.

- Interactive indicator pages with highly customizable and shareable data visualizations.

- A Budget Threads feature that offers Pew’s read on the latest state fiscal news.