Size of Long-term Obligations Varies Across States

States commit to future spending both when they borrow and when they fall short of funding the cost of retirement benefits for their public employees. As of fiscal year 2012, the largest of these long-term obligations was unfunded pension liabilities in 35 states, unfunded retiree health care costs in seven states, and public debt in eight states.

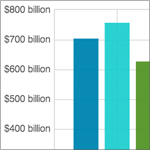

States pass balanced budgets each year, but some spending commitments that will not come due for years go unpaid. A snapshot of debt and unfunded retirement costs in fiscal 2012 shows totals of $915 billion in unfunded pension benefits, $757 billion in outstanding public debt, and $577 billion in unfunded retiree health care and other nonpension benefits.

States take on these obligations, which are paid over decades, for different reasons. Sometimes a state borrows to build infrastructure projects that deliver services for years in the future and may spur economic growth. When the bill comes due, states usually cover these debt obligations before other expenses. In other instances, a state creates unfunded liabilities when it sets aside less than is needed to cover the full retirement costs for public services already performed, shifting those expenses to future taxpayers. Download the data.

Largest Long-term Obligations |

|||

| Unfunded pension benefits | 31 states | ||

| Unfunded retiree health care | 11 states | ||

| Public debt | 8 states | ||

|

Source: Pew analysis of data from the U.S. Census Bureau’s Annual Survey of State Government Finances and Pew’s report, “The Widening Gap Update” |

|||

States face larger shortfalls for pensions than for retiree health care but have already saved far more for retirees’ pension checks than for their medical bills. Nationwide, state pension promises were 72.3 percent funded in fiscal 2012, ranging on a state-by-state basis from 99.9 percent in Wisconsin to 40.4 percent in Illinois. For retiree health care, however, states could cover only 6.1 percent of total liabilities. Just two states, Arizona and Ohio, had set aside even half of the cost of their future retiree health care benefits, and 15 had set aside nothing. It is more common for states to pay retiree health care bills as they occur than to prefund the costs, as they do for pensions.

This snapshot found that, as of fiscal 2012:

- Pension shortfalls in 24 states accounted for more than half of total costs from this trio of long-term obligations. By contrast, these unfunded liabilities made up the smallest share of long-term obligations in Wisconsin (0.5 percent). Because most states smooth losses or gains in pension fund investments across several years, unfunded liabilities in fiscal 2012 still reflected some of the steep market drops experienced during the Great Recession. Recent stock gains are expected to make up some of these declines. (For more information, see The Pew Charitable Trusts’ fact sheet, “The Fiscal Health of State Pension Plans.”)

- Unfunded retiree health care costs accounted for more than half of states’ long-term obligations in Delaware and North Carolina. Meanwhile, Nebraska does not acknowledge any retiree health care obligations.

- Debt was a larger liability than total unfunded retirement costs (for pensions and retiree health care combined) in six states: Massachusetts, New York, Oregon, South Dakota, Washington, and Wisconsin.

These claims on future revenue put pressure on state finances, potentially affecting borrowing costs, credit ratings, and funds available for other priorities—such as education or health care. However, the degree of fiscal challenge varies depending on the size of a state’s budget, economy, and population, and on the type of liability. States with faster-growing economies may find their obligations more manageable. States also may be able to cut certain costs over time by refinancing debt or modifying retiree health benefits, which in some places may have fewer legal protections than pensions do.

Besides debt and unfunded retirement costs, states also face other long-term budget pressures, such as expenses for deferred maintenance and upgrades to infrastructure.

Analysis by Sarah Babbage and Kil Huh

ADDITIONAL RESOURCES

Fact Sheet

Podcast