From Payday to Small Installment Loans

Risks, opportunities, and policy proposals for successful markets

Stocksy

StocksyOverview

All of the largest payday lenders now offer installment loans, which are repayable over time and secured by access to the borrower’s checking account, in addition to conventional payday loans that are due in a single lump sum.1 This shift toward installment lending has been geographically widespread, with payday or auto title lenders issuing such loans or lines of credit in 26 of the 39 states where they operate.2

Research by The Pew Charitable Trusts and others has shown that the conventional payday loan model is unaffordable for most borrowers, leads to repeat borrowing, and promotes indebtedness that is far longer than advertised.3 To address these problems, the Consumer Financial Protection Bureau (CFPB) in June 2016 proposed a rule for regulating the payday and auto title loan market by requiring most small loans to be repayable in installments. In Colorado, a structure requiring that loans be payable over time—combined with lower price limits—was shown to reduce harm to consumers compared with lump-sum loans, after that state passed legislation in 2010 requiring all payday loans to become six-month installment loans.4

Further, national survey data show that 79 percent of payday borrowers prefer a model similar to Colorado’s, in which loans are due in installments that take only a small share of each paycheck.5 Seventy-five percent of the public also supports such a requirement.6

To get ahead of the CFPB’s regulation and avoid state-level consumer protections, and in response to these consumer preferences, the trend toward payday installment lending is accelerating.7 However, as it exists today, in the absence of sensible regulatory safeguards, this installment lending, as well as that in the traditional subprime installment loan market that has existed for a century, can be harmful.8

This brief describes practices that are unique to the payday installment loan market and others that exist primarily in the traditional subprime installment loan market, focusing on four that threaten the integrity of subprime small-dollar loan markets: unaffordable payments, frontloaded charges that add costs for borrowers who repay early or refinance, excessive durations, and unnecessarily high prices.9

Federal and state policymakers should act now to establish policies that benefit consumers and encourage responsible and transparent lending. Pew’s research shows that regulators can address harmful practices by containing payment sizes, requiring that all charges be spread evenly over the term of the loan, restricting most loan terms to six months, enacting price limits that are sustainable for borrowers and lenders that operate efficiently, and providing a clear regulatory path for lower-cost providers, such as banks and credit unions, to issue small loans.

The CFPB can implement many of these protections. However, it does not have the authority to limit interest rates, so although lump-sum lending will be largely curtailed after the bureau’s rule takes effect, high-cost installment loans will probably continue to be issued unless states act to regulate them. As the transition toward longer-term lending continues, policymakers should address problems wherever payday installment loans and subprime installment loans exist.

Why lenders are moving away from lump-sum products

The trend among payday and auto title lenders toward offering installment loans is being driven by three factors: consumer preference, regulatory pressure, and lenders’ effort to avoid consumer protections put in place for lump-sum payment loans.

Consumer preference

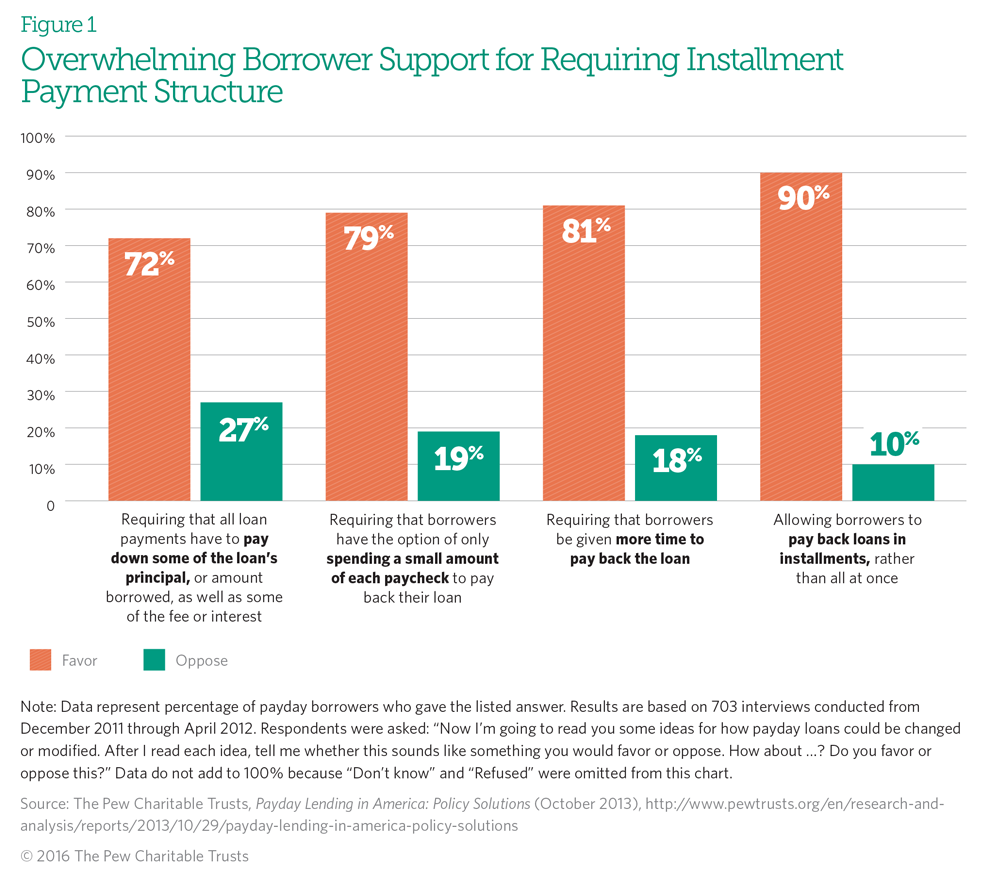

Pew’s research shows that, compared with the conventional lump-sum model, payday loan customers overwhelmingly support requiring an installment payment structure that gives them more time to repay loans in smaller amounts that fit into their budgets. One lender explained, “I learned in Colorado that our consumers like the affordability,” and noted the industry’s probable shift in that direction.10 The head of the primary trade association for online lenders said her members have mostly changed their products from two-week lump-sum loans to installment loans in response to consumer demand.11 (See Figure 1.)

Regulation

In 2013, federal banking regulators issued guidance strongly discouraging banks from issuing lump-sum “deposit advance loans,” which mimic the structure of conventional payday loans.12 The CFPB’s proposed rule for payday and similar loans emphasizes the need for affordable monthly payments, and if finalized, the bureau’s rule would expedite the transition toward installment loan structures.13

In response, payday lenders have supported bills in several states, including Arizona, Indiana, Mississippi, and Tennessee, to allow the types of high-cost installment loans and lines of credit that would be permitted under the CFPB’s proposal.14 Industry consultants have also observed that the CFPB’s pending rule encourages a shift to installment lending. One noted that “many of today’s payday consumers can likely handle an installment loan, at yields that emulate a payday loan,” and encouraged the industry to lobby to change state laws to facilitate “highyield” installment products.15

Consumer protections

Some lenders have switched to installment loans to avoid consumer protection laws.16 For example, after a Delaware law took effect in 2013 and restricted to five the number of short-term consumer loans that payday lenders in that state may make to a given borrower in any 12-month period,17 companies began offering installment loans of more than two months alongside conventional two-week payday loans. This allowed them to avoid triggering the new limit because the law defined “short term” as less than 60 days.18 In another case, the Military Lending Act of 2007 limited interest rates on loans to military service members of 91 days or less, so lenders began making loans of 92 days or more in order to charge higher rates.19 Lenders have used similar tactics in Wisconsin, Illinois, and New Mexico.20

High-Cost Installment Loans Could Proliferate Under CFPB Rule

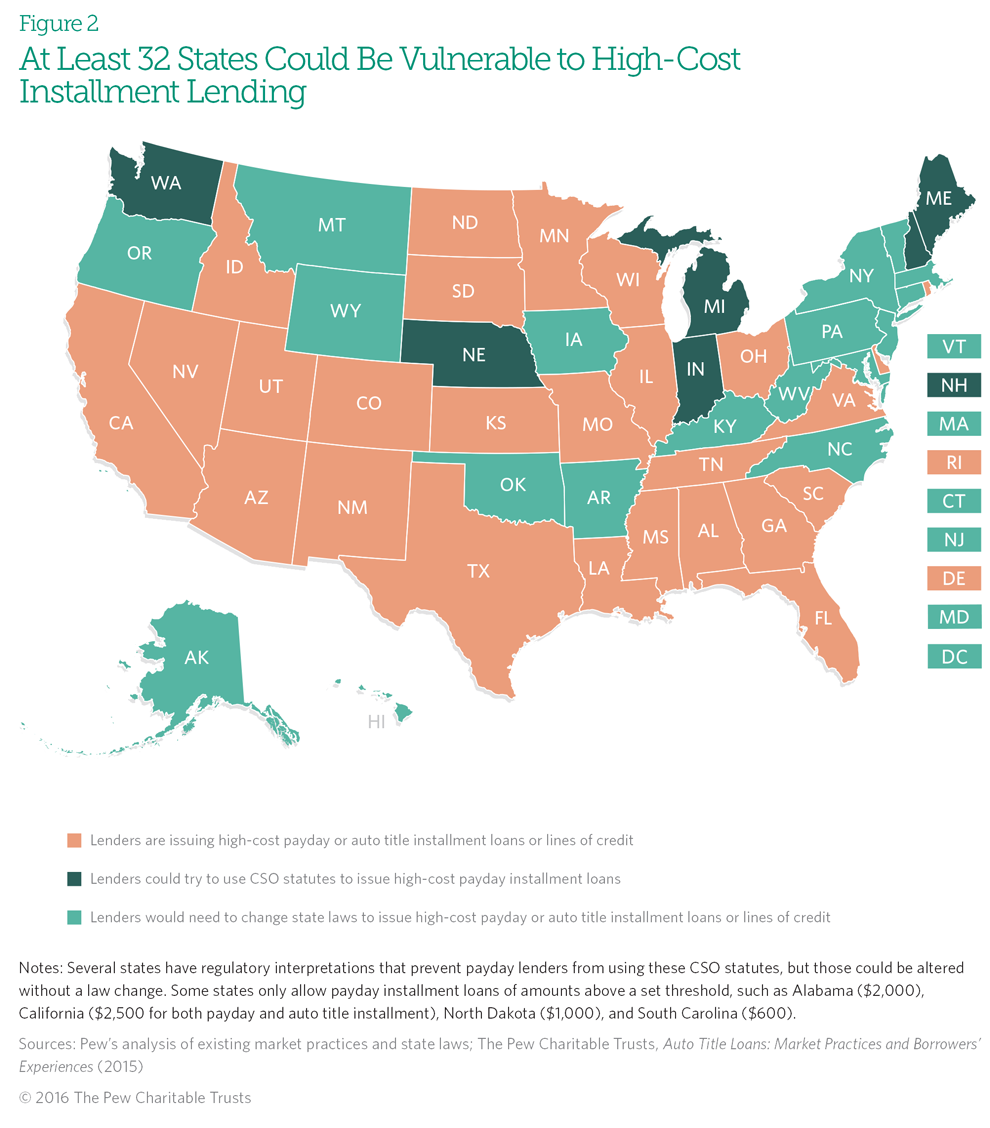

Payday and auto title lenders are already issuing high-cost installment loans or lines of credit in 26 of the 39 states where they operate. The CFPB issued a proposed rule in June 2016. Once it is finalized and lump-sum lending is more restricted, lenders will probably accelerate their efforts to expand high-cost installment loans to other states, and they are likely to do that in two ways. First, they will probably attempt to modify laws in the states that do not yet allow installment lending. Until now, lenders have had little incentive to advocate for such change because they could issue lump-sum payday and auto title loans, but as that market becomes more restricted, they will be motivated to try to increase the number of states that permit high-cost installment lending.

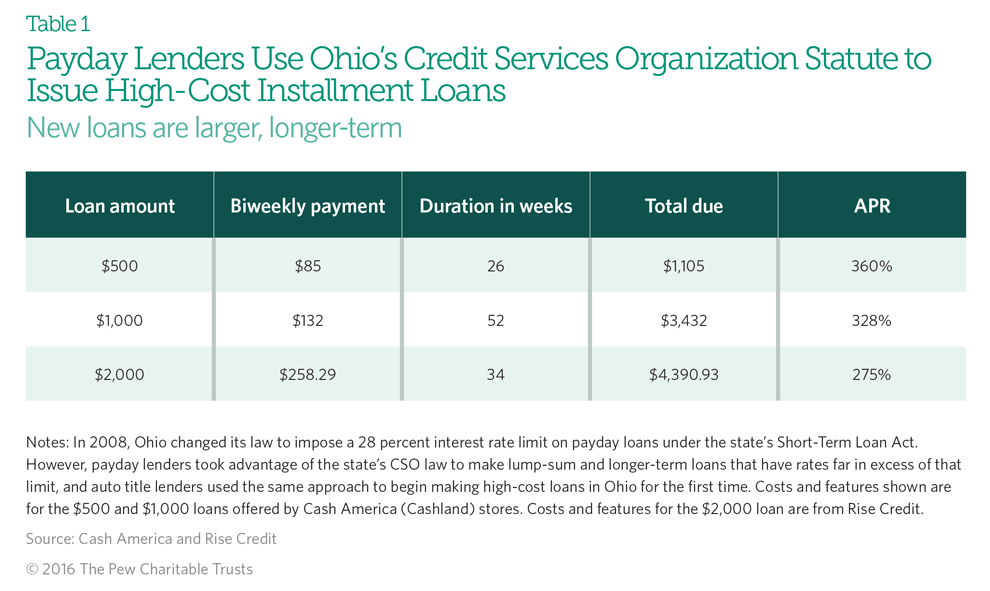

Secondly, they may try to take advantage of credit services organization (CSO) statutes, which allow the brokering of loans, in states that have such laws.* Payday and auto title lenders in Ohio and Texas already act as brokers under such laws, meaning that they charge large fees to borrowers to arrange loans and guarantee those loans for other lenders. Functionally, this brokering is an evasion of low interest rate limits because the fees charged are in addition to the interest paid to the third-party lender and significantly increase borrowers’ costs.† Some of the states where payday and auto title lenders operate but do not issue installment loans or lines of credit also have CSO statutes that lenders may try to use to circumvent consumer protections. In total, at least 32 of the 39 states where payday and auto title lenders operate could be vulnerable to high-cost payday or auto title installment loans. Table 1 shows the types of payday installment loans being issued under Ohio’s CSO statute.

* National Consumer Law Center, Installment Loans: Will States Protect Borrowers From a New Wave of Predatory Lending? (July 2015), 41-42, http:// www.nclc.org/images/pdf/pr-reports/report-installment-loans.pdf.

† Mark Huffman, “Consumer Group Charges Loophole Allows Continued Payday Lending in Ohio,” Consumer Affairs, Nov. 11, 2015, https://www.consumeraffairs.com/news/consumer-group-charges-loophole-allows-continuedpayday- lending-in-ohio-111115.html.

How regulators can address the 4 key problems with installment loans

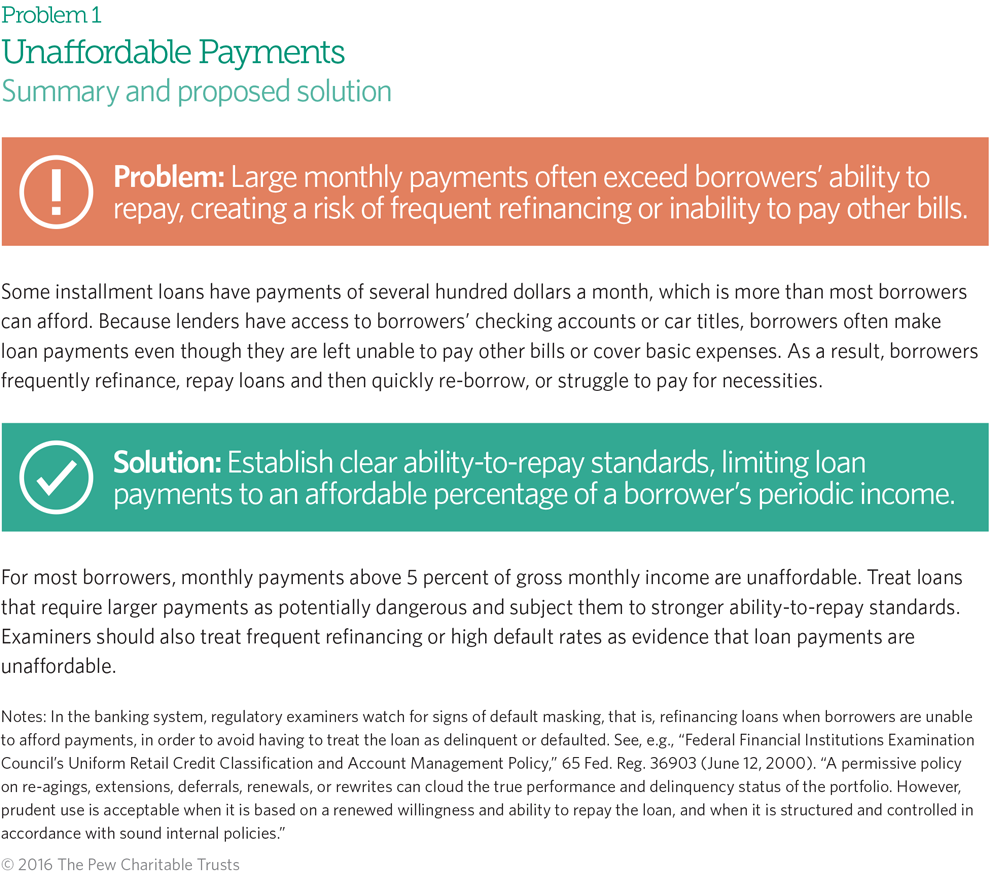

Unaffordable payments

Most installment payday loans have payments that exceed what typical borrowers can afford. Unaffordable payments can lead to the same types of problems that exist in the conventional lump-sum loan market: frequent re-borrowing, overdrafts, and the need for a cash infusion to retire debt.

Payday installment loan payments are usually much more than the 5 percent of income that borrowers can afford. And because lenders have access to borrowers’ checking accounts, either electronically or with postdated checks, they can collect the installments regardless of the borrowers’ ability to afford the payments. Similarly, in the auto title loan market, lenders’ ability to repossess borrowers’ vehicles can pressure customers to make loan payments they cannot afford, which in turn can leave consumers without enough money to meet their basic needs.

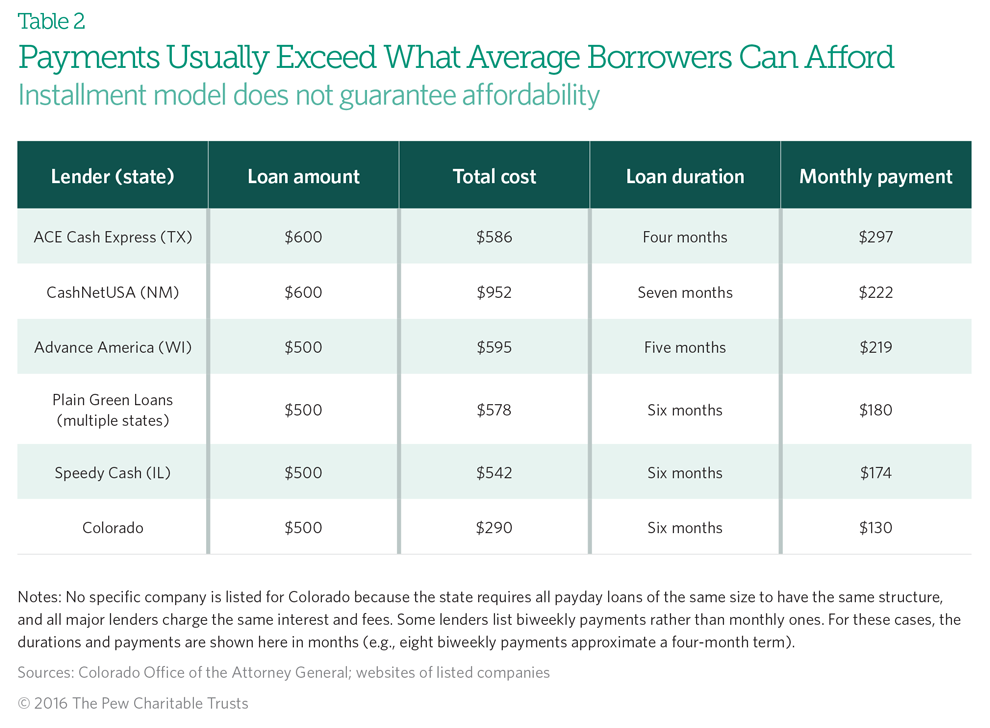

Table 2 shows how payday installment loan payments in several states consume between 7 percent and 12 percent of the average borrower’s gross monthly income (of just under $2,600) and compares that with loan payments in Colorado, where strong regulations require both smaller payments and lower prices.21

To solve the problem of unaffordable payments, policymakers should require loans to be repayable in small installments that are affordable for most borrowers. Research shows that in order to fit the budgets of typical payday loan borrowers, payments must not exceed 5 percent of monthly income.

Another solution that has been proposed is to require lenders to conduct underwriting to assess the borrowers’ ability to repay. However, without clear product safety standards, such as limiting loan payments to 5 percent of a borrower’s paycheck, this approach carries risk. It can add substantially to the price of loans by imposing new costs on lenders. And because lenders have access to borrowers’ checking accounts or car titles and can collect even if borrowers lack the ability to repay, it provides lenders with little incentive to ensure that payments are truly affordable.

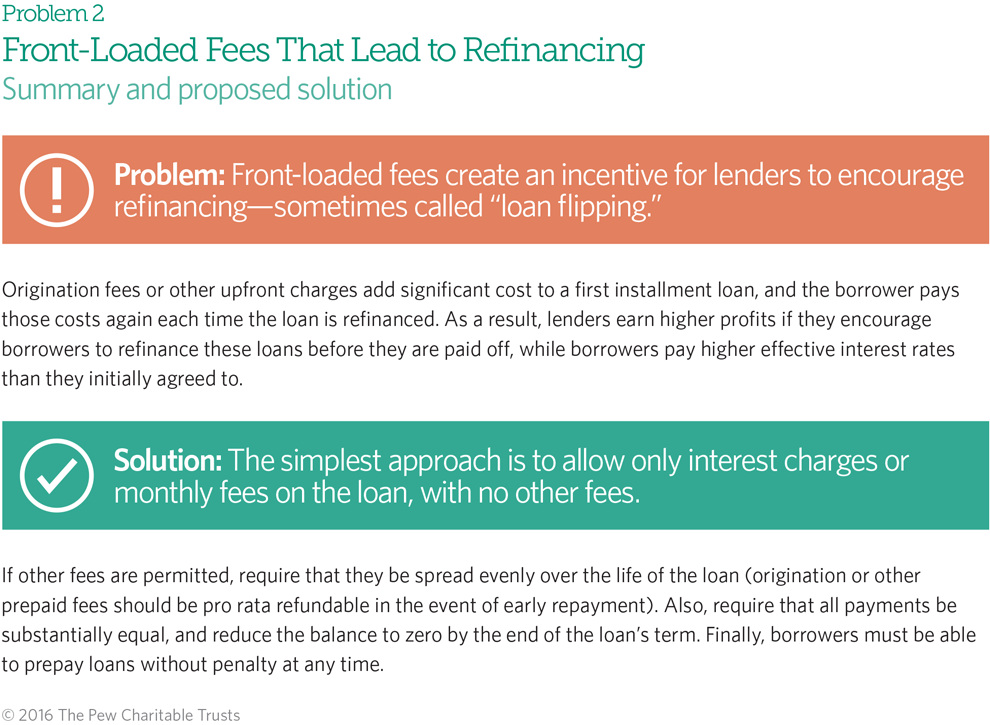

Front-loaded charges

It is customary in consumer credit markets for lenders to assess an upfront fee to process an application or originate a loan. But in subprime consumer finance installment loan markets, large upfront origination fees often harm consumers by significantly increasing the cost of the loan at the time it is issued, effectively penalizing borrowers who repay early. These fees increase revenue and provide a substantial incentive for lenders to encourage refinancing in order to earn an additional origination fee. Small-loan borrowers are particularly susceptible to offers to refinance because, like many low- and moderate-income households, their income is often volatile and they have little or no savings.22

This misalignment of incentives has led to widespread repeated refinancing, or “loan flipping,” in the traditional subprime small installment loan market, with refinances accounting for about three-quarters of loan volume for one of the largest lenders.23 One company’s CEO explained on an earnings call with investors that its customer service representatives receive a bonus based on how many of their customers refinance “because encouraging renewals is a very important part of our business.”24

To solve this problem, finance charges, such as fees and interest, should be spread evenly over the life of the loan, rather than front-loaded. This protects borrowers against incurring large fees at the outset of the loan and aligns lenders’ and borrowers’ interests by ensuring profitability and affordability without discouraging early payment or providing an incentive to lenders to steer their customers toward refinancing.

When Colorado reformed its payday loan statute in 2010, it allowed an origination fee but required lenders to provide pro rata refunds whenever borrowers prepay. This was critical to the success of the state’s reform because lenders did not have an incentive to steer borrowers to refinance loans.25

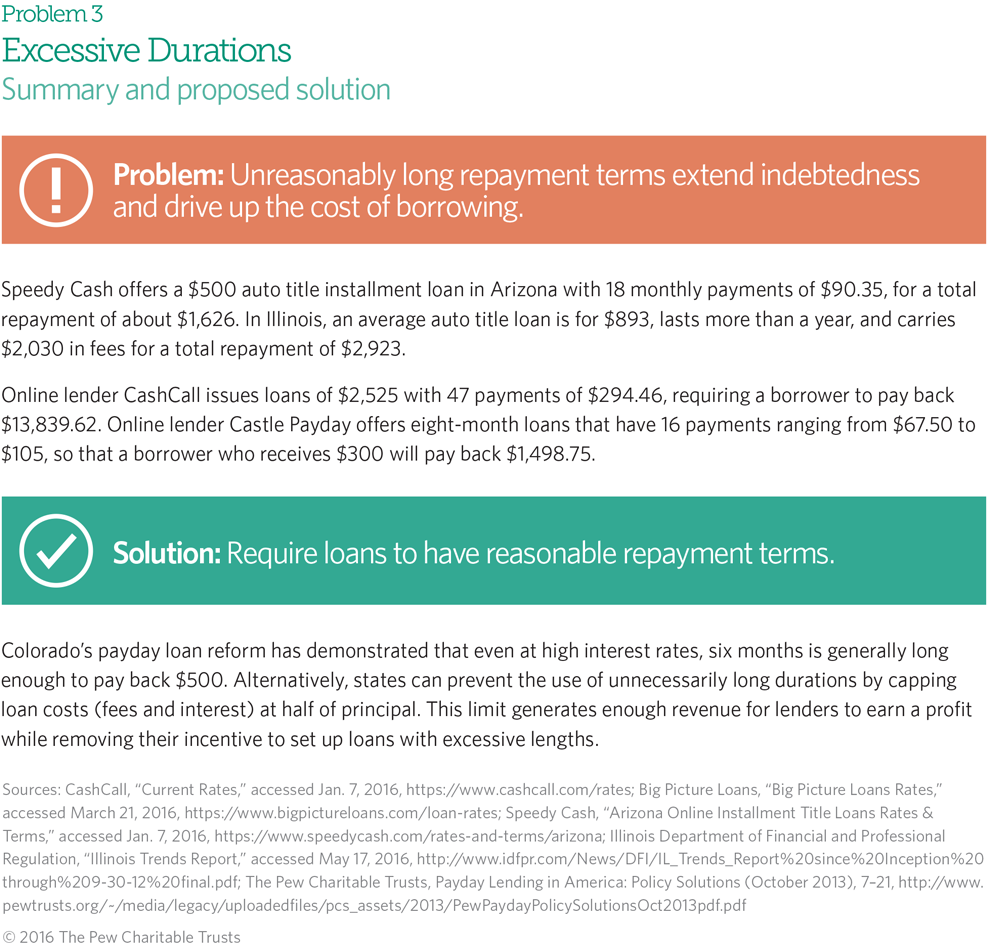

Excessive durations

Some high-interest installment loans have unreasonably long terms, with only a small portion of each payment reducing the loan’s balance. Excessive loan lengths can double or triple borrowers’ costs,26 and very long loan durations also pose risk to borrowers with volatile incomes. In lower-income months, they may struggle to afford loan payments but have little choice because lenders have access to their checking accounts or car titles. Pew’s research has found that even at high interest rates, six months is generally long enough to repay a $500 loan, and one year is typically sufficient for a $1,000 loan.27 Similarly, the public considers very short terms (less than a month) or very long terms (more than a year) to be unreasonable for a $500 loan.28

Discouraging excessive loan terms will become important as longer-term installment loans become the norm. The final CFPB rule for payday and similar loans will need to include clear guidelines for appropriate loan durations. States that modify their existing payday or installment loan statutes should also put policies in place that discourage excessive lengths. The CFPB’s proposed guidelines for certain longer-term alternative loans require terms between 45 days and six months.29 This range is consistent with Pew’s findings about the time borrowers need to repay loans affordably, with public opinion about reasonable durations for a $500 loan, and with the small-dollar loan programs established by the Federal Deposit Insurance Corp., National Credit Union Administration, and National Federation of Community Development Credit Unions, which give borrowers several months to repay.30

Unnecessarily high prices

Prices in the payday and auto title loan markets are higher than is needed to ensure the availability of credit and the profitability of lenders. But research shows that borrowers are in financial distress and are primarily focused on how much they can borrow, how quickly they can receive the funds, and how certain they are to be approved, so lenders compete on location, customer service, and speed and do not lower prices to gain customers.31 As a result, prices remain far higher than is necessary for lenders to be profitable and to ensure the widespread availability of credit for consumers.32 Therefore, rate limits are necessary to reduce prices and promote safe payday and auto title loans. Forty-six states and the District of Columbia set price limits on at least one type of small-dollar loan.33

Policymakers can employ two strategies to encourage reasonably priced credit. The first is to cap fees and interest rates. When states have enacted limits that fall below current payday loan prices but somewhat above traditional usury rate thresholds, lenders have stayed in business and continued to be profitable and credit has remained readily available. Policymakers can restrict interest rates and fees at or slightly below the level seen in Colorado, where an average $389 payday installment loan is repaid in three months and carries an APR of 121 percent—the lowest of any state—for a total cost of $116 in fees.34

Regardless of the CFPB’s final rule, however, state policymakers may reasonably choose to prohibit payday and auto title loans in their states. An effective way to do this is by limiting finance charges to 36 percent APR (inclusive of all fees), which has historically applied to loans of larger sizes and is a price point at which these lenders will not operate.

The second strategy to drive down loan prices is to enable lower-cost providers of small loans. Banks and credit unions have large competitive advantages over payday and auto title lenders because they are diversified businesses that cover their overhead by selling other products, could lend to their own customers rather than paying to attract new ones, have customers who make regular deposits in their checking accounts, and have a low cost of funds.35 As a result, these financial institutions could profitably make small loans at double-digit APRs, for prices that are six to eight times lower than those offered by payday lenders. However, to offer these loans sustainably, banks’ fee-inclusive rates would generally need to be somewhat higher than 36 percent APR.36

Banks and credit unions would also need to use simple, clear, streamlined underwriting standards to issue small loans profitably, such as a limit on monthly loan payments of 5 percent of monthly income and on loan terms of six months as the CFPB proposed in its March 2015 framework.37 Underwriting that requires staff time or extensive documentation would discourage banks from issuing small loans, because it would cost more in overhead than they could earn in revenue and make them vulnerable to increased regulatory scrutiny.

In addition, banks could take steps to screen out very poor credit risks by ensuring that applicants make regular deposits, have an account in good standing, are not using overdraft services excessively, and are not delinquent on other loans inside the bank or credit union. Pew estimates that with streamlined standards such as these, banks could profitably offer a $400, three-month loan for about $50 to 60, or half what Colorado’s payday installment loans cost today.

Conclusion

The payday loan market is quickly moving away from lump-sum lending and toward installment loans. The shift is driven in part by consumer preference and regulatory pressure, but in some instances lenders have used installment loan models to evade consumer protections that cover only shorter-term loans.

The CFPB’s proposed small-dollar loan rule will almost certainly accelerate this transition, but if it is going to benefit consumers, it must also be structured to ensure reasonable terms, affordability, and lower prices. To prevent new harm to borrowers, federal and state policymakers should take additional steps to resolve the four major problems with the small installment loan market: unaffordable payments, front-loaded charges that often lead to high rates of loan refinancing, excessive durations, and noncompetitive pricing. These issues can be solved by requiring that payments be affordable as determined by the borrower’s income, mandating that all charges be spread evenly over the term of the loan, limiting terms for small-dollar loans to six months in most cases, enacting price limits that are sustainable for borrowers and lenders that operate efficiently, and allowing lower-cost providers such as banks and credit unions to issue small loans sustainably.

Methodology

To conduct this research, Pew reviewed the payday, auto title, pawn, and installment loan and credit services organization statutes of every state as well as the websites of selected payday and auto title lenders. Pew contacted state regulators and lenders in any state where it was unclear whether payday installment loans, auto title installment loans, or similar lines of credit were being issued.

Endnotes

- High-interest installment loans and lines of credit are issued by storefront payday lenders and state-licensed online payday lenders in 19 states: Alabama, California, Colorado, Delaware, Idaho, Illinois, Kansas, Missouri, New Mexico, North Dakota, Ohio, Rhode Island, South Carolina, South Dakota, Tennessee, Texas, Utah, Virginia, and Wisconsin. High-interest auto title installment loans are issued in 17 states, and lenders were allowed to start offering them in Mississippi as of July 1, 2016. In total, multipayment payday or auto title loans are available in 26 of the 39 states where payday and auto title lenders operate.

- This figure includes only state-licensed lenders. Online lenders that are not complying with state laws are offering these loans in more states. The Pew Charitable Trusts, Fraud and Abuse Online: Harmful Practices in Internet Payday Lending (October 2014), 23, http://www.pewtrusts.org/~/media/assets/2014/10/ payday-lending-report/ fraud_and_abuse_online_harmful_practices_in_internet_payday_lending.pdf.

- The Pew Charitable Trusts, “Collection: Payday Lending in America,” accessed April 19, 2016, http://www.pewtrusts.org/en/research-and-analysis/collections/2014/12/payday-lending-in-america.

- The Pew Charitable Trusts, Payday Lending in America: Policy Solutions (October 2013), 12–16, http://www.pewtrusts.org/~/media/legacy/uploadedfiles/pcs_assets/2013/ pewpaydaypolicysolutionsoct2013pdf.pdf.

- Ibid., 22.

- The Pew Charitable Trusts, “CFPB Proposal for Payday and Other Small Loans: A Survey of Americans” (July 2015), 4, http://www.pewtrusts.org/~/media/assets/2015/07/ cfpb_chartbook.pdf.

- The largest online lender, Enova, earned 40 percent of its revenue from installment loans in the third quarter of 2015, up from 30 percent a year earlier. Enova International, “Enova Announces Third Quarter 2015 Results,” last modified Nov. 4, 2015, https://www.enova.com/newsroom/ enova-announces-third-quarter-2015-results. Another large online lender, Elevate, has eliminated lump-sum credit in favor of loans that are repayable over at least a few months. Elevate Credit, “Form S-1 Registration Statement” (November 2015), https://www.sec.gov/Archives/edgar/data/1651094/ 000119312515371673/ d83122ds1.htm.

- Traditional installment lenders offer loans typically ranging from $100 to $10,000 from nonbank offices. These loans are underwritten and are generally secured not by a checking account but by household goods or car titles. They carry APRs that are usually higher than credit cards but much lower than conventional payday loans. The Pew Charitable Trusts, Payday Lending in America: Policy Solutions, 6; Paul Kiel, “The 182 Percent Loan: How Installment Lenders Put Borrowers in a World of Hurt,” ProPublica, May 13, 2013, https://www.propublica.org/article/installment-loans-world-finance; Thomas A. Durkin, Gregory Elliehausen, and Min Hwang, “Findings From the AFSA Member Survey of Installment Lending,” Oct. 18, 2014, http://www.masonlec.org/site/rte_uploads/files/Manne/11.21.14 JLEP Consumer Credit and the American Economy/Findings from the AFSA Member Survey of Installment Lending.pdf.

- National Consumer Law Center, Installment Loans: Will States Protect Borrowers From a New Wave of Predatory Lending? (July 2015), http://www.nclc.org/images/pdf/pr-reports/report-installment-loans.pdf.

- Jim Brunner, “Moneytree Leads Push to Loosen State’s Payday-Lending Law,” Seattle Times, March 3, 2015, http://www.seattletimes.com/seattle-news/moneytree-leads-push-to-loosen-states-payday-lending-law/.

- Lisa McGreevy, CEO of the Online Lenders Alliance, an industry trade group in Alexandria, Virginia, said most of its members have moved from two-week payday loans to longer-term products because of consumer demand. John Oravecz, “Feds Eye Online Lending Practices,” TribLIVE Business, Aug. 9, 2014, http://triblive.com/business/headlines/6575923-74/loans-cashcall-lending#axzz3KOdKTDWD.

- Office of the Comptroller of the Currency, “Guidance on Supervisory Concerns and Expectations Regarding Deposit Advance Products,” Nov. 21, 2013, http://www.occ.gov/news-issuances/news-releases/2013/ nr-ia-2013-182a.pdf; Federal Deposit Insurance Corporation, “Guidance on Supervisory Concerns and Expectations Regarding Deposit Advance Products,” Nov. 21, 2013, https://www.fdic.gov/news/news/press/2013/pr13105a.pdf.

- Consumer Financial Protection Bureau, “Consumer Financial Protection Bureau Proposes Rule to End Payday Debt Traps,” June 2, 2016, http://www.consumerfinance.gov/about-us/newsroom/consumer-financial-protection-bureau-proposes-rule-end-payday-debt-traps/.

- Scot Mussi, “My Turn: Why Arizona Needs ‘Flex Loans,’” The Arizona Republic, Feb. 29, 2016, http://www.azcentral.com/story/opinion/op-ed/2016/02/29/flex-loans-mussi/80951160/; Doug LeDuc, “Payday Lenders Look to Expand,” KPC News, Feb. 17, 2016, http://kpcnews.com/special_sections/working_and_struggling/ article_aa21d879-882d-5ebb-b22a-58a82f32a31f.html; Ted Carter, “Mississippi Senate Passes Bill to Expand Car Title-Lending,” Mississippi Business Journal, March 4, 2016, http://msbusiness.com/2016/03/car-title-lending-bill-called-step-to-preserve-small-loans/; Jennifer Kraus, “Critics Call 279% Loan a ‘Debt Trap’ for Poor,” News Channel 5, Feb. 16, 2016, http://www.newschannel5.com/news/newschannel-5-investigates/consumer-alert/critics-call-279-loan-a-debt-trap-for-poor.

- Rick Hackett, “Report From NonPrime101 Conference: Redesigning Small Dollar Lending to Survive Threatened Regulatory Intervention?” NonPrime101 Blog, Aug. 3, 2015, https://www.nonprime101.com/report-from-nonprime101-conference-redesigning-small-dollar-lending-to-survive-threatened-regulatory-intervention/.

- Carter Dougherty, “Payday Lenders Evading Rules Pivot to Installment Loans,” Bloomberg News, May 29, 2013, http://www.bloomberg.com/news/articles/2013-05-29/payday-lenders-evading-rules-pivot-to-installmant-loans. Some payday lenders claim that they are “making a pragmatic change in business strategy” or responding to “approving statements” that regulators have made about installment loans. Industry analysts and advocates quoted in the article describe the shift toward installment lending both as a way of “shedding regulatory risk” and as part of an ongoing effort “to meet the needs of our customers with new products.”

- 66 Del. Laws, c. 22, § 1.; §2235A, “Short-Term Consumer Loans,” http://delcode.delaware.gov/title5/c022/sc03/index.shtml.

- 5 Del. C. §2227 et seq.; 5 Del. C. §2235a et seq., http://delcode.delaware.gov/title5/title5.pdf; Advance America, “Fees and Terms for Loans in Delaware,” accessed Dec. 28, 2015, https://www.advanceamerica.net/locations/details/store-5467/527-E-Basin-Road/New-Castle/DE/19720.

- “Limitations on Terms of Consumer Credit Extended to Service Members and Dependents,” a proposed rule by the Defense Department, Fed. Reg. (Sept. 29, 2014), https://www.federalregister.gov/articles/2014/09/29/2014-22900/limitations-on-terms-of-consumer-credit-extended-to-service-members-and-dependents; U.S. Department of Defense, “Department of Defense Issues Final Military Lending Act Rule,” July 21, 2015, http://www.defense.gov/News/News-Releases/News-Release-View/Article/612795.

- Paul Kiel, “Whack-a-Mole: How Payday Lenders Bounce Back When States Crack Down,” ProPublica, Aug. 6, 2013, https://www.propublica.org/article/how-payday-lenders-bounce-back-when-states-crack-down; Patrick Marley, “Payday Lenders Back in Business With Looser Regulations,” Milwaukee Journal-Sentinel, Dec. 9, 2012, http://archive.jsonline.com/news/statepolitics/payday-lenders-back-in-business-with-looser-regulations-jt7useg-182755581.html.

- The Pew Charitable Trusts, Payday Lending in America: Policy Solutions, 30.

- The Pew Charitable Trusts, The Precarious State of Family Balance Sheets (January 2015), http://www.pewtrusts.org/en/research-and-analysis/reports/2015/01/ the-precarious-state-of-family-balance-sheets; Jonathan Morduch and Rachel Schneider, “Spikes and Dips: How Income Uncertainty Affects Households,” U.S. Financial Diaries (2013), 1, http://www.usfinancialdiaries.org/issue1-spikes; Sharon Wolf et al., “Patterns of Income Instability Among Low- and Middle-Income Households With Children,” Family Relations 63, no. 3 (2014): 397–410, http://onlinelibrary.wiley.com/doi/10.1111/fare.12067/abstract; Constance Newman, “The Income Volatility See-Saw,” USDA Economic Research Service (2006), http://www.ers.usda.gov/media/ 1038421/err23.pdf.

- Morningstar, World Acceptance Corporation 2014 Annual (10-K) Report (March 2014), 12, http://quote.morningstar.com/stock-filing/Annual-Report/2014/3/31/t.aspx?t=:WRLD&ft=10-K&d=cd8e84303d5b870ed9bdc2d5ef2dae71. “For fiscal 2014, 2013, and 2012, the percentages of the Company’s loan originations that were refinancings of existing loans were 73.5%, 75.3%, and 75.9%, respectively.”

- Sandy McLean, “World Acceptance’s CEO Discusses F4Q 2014 Results—Earnings Call Transcript,” April 29, 2014, http://seekingalpha.com/article/2174173-world-acceptances-ceo-discusses-f4q-2014-results-earnings-call-transcript.

- The Pew Charitable Trusts, “Trial, Error, and Success in Colorado’s Payday Lending Reforms” (December 2014), http://www.pewtrusts.org/~/media/assets/2014/ 12/ pew_co_payday_law_comparison_dec2014.pdf.

- The Pew Charitable Trusts, Payday Lending in America: Policy Solutions, 42, 45–46.

- Ibid., 42.

- The Pew Charitable Trusts, “CFPB Proposal for Payday and Other Small Loans: A Survey of Americans.”

- Consumer Financial Protection Bureau, “Consumer Financial Protection Bureau Proposes Rule to End Payday Debt Traps.”

- The Pew Charitable Trusts, Payday Lending in America: Policy Solutions, 42; The Pew Charitable Trusts, “CFPB Proposal for Payday and Other Small Loans: A Survey of Americans,” 5; National Federation of Community Development Credit Unions, Borrow & Save: Building Assets With a Better Small-Dollar Loan (July 2013), http://cdcu.coop/wp-content/uploads/2013/03/Borrow-and-Save-Final-July-30-2013.pdf. pdf; Federal Deposit Insurance Corporation, “A Template for Success: The FDIC’s Small-Dollar Loan Pilot Program” (2010), https://www.fdic.gov/bank/analytical/quarterly/2010_vol4_2/ FDIC_Quarterly_Vol4No2_SmallDollar.pdf; National Credit Union Administration, 12 CFR Part 701, Sept. 24, 2010, https://www.ncua.gov/Legal/Documents/Regulations/FIR20100916SmAmt.pdf.

- The Pew Charitable Trusts, “The Post Office and Financial Services” (July 2014), http://www.pewtrusts.org/~/media/assets/2014/07/fin_presentation-of-pew-research--the-post-office-and-financial-services.pdf; Robert B. Avery and Katherine A. Samolyk, “Payday Loans Versus Pawn Shops: The Effects of Loan Fee Limits on Household Use” (2011), http://dx.doi.org/10.2139/ssrn.2634584; Mark J. Flannery and Katherine A. Samolyk, “Scale Economies at Payday Loan Stores” (paper presented at the Federal Reserve Bank of Chicago’s 43rd Annual Conference on Bank Structure and Competition, Chicago, May 2007), http://dx.doi.org/10.2139/ssrn.2360233.

- The Pew Charitable Trusts, “How State Rate Limits Affect Payday Loan Prices” (April 2014), http://www.pewtrusts.org/~/media/legacy/uploadedfiles/pcs/content-level_pages/fact_sheets/stateratelimitsfactsheetpdf.pdf.

- The Pew Charitable Trusts, Payday Lending in America: Policy Solutions, 39.

- Colorado Office of the Attorney General, “2014 Deferred Deposit/Payday Lenders Annual Report,” http://www.coloradoattorneygeneral.gov/sites/default/files/contentuploads/ cp/ConsumerCreditUnit/UCCC/2014_ddl_ar_composite.pdf.

- Nick Bourke, “Regulators Should Let Banks Get Back to Small-Dollar Loans,” American Banker, Sept. 16, 2015, http://www.americanbanker.com/bankthink/regulators-should-let-banks-get-back-to-small-dollar-loans-1076693-1.html.

- Nick Bourke, “Why Credit Unions Should Pay Attention to the Payday Loan Market—and What the CFPB Does About It,” Credit Union Times, Dec. 9, 2015, http://www.pewtrusts.org/en/about/news-room/opinion/2016/01/06/why-credit-unions-should-pay-attention-to-the-payday-loan-market-and-what-the-cfpb-does-about-it.

- Consumer Financial Protection Bureau, Small Business Advisory Review Panel for Potential Rulemakings for Payday, Vehicle Title, and Similar Loans: Outline of Proposals Under Consideration and Alternatives Considered (March 2015), http://files.consumerfinance.gov/f/201503_cfpb_outline-of-the-proposals-from-small-business-review-panel.pdf; The Pew Charitable Trusts, “Understanding the CFPB Proposal for Payday and Other Small Loans” (July 2015), http://www.pewtrusts.org/~/media/assets/2015/07/cfpb-primer_artfinal.pdf.

This video is hosted by YouTube. In order to view it, you must consent to the use of “Marketing Cookies” by updating your preferences in the Cookie Settings link below. View on YouTube

This video is hosted by YouTube. In order to view it, you must consent to the use of “Marketing Cookies” by updating your preferences in the Cookie Settings link below. View on YouTube

Federal Rules for Small Loans

ADDITIONAL RESOURCES

Opinion

Issue Brief