Workers Open to Retirement Plan Features Intended to Boost Savings

How those who do not participate in employer-sponsored programs view proposals to make doing so automatic

Overview

Workplace savings plans have long been key elements of funding post-retirement life, along with Social Security and other personal savings. But more than a quarter of American workers whose employers sponsor a retirement plan do not participate. These workers cite a variety of reasons, including concerns about affordability or eligibility. That means many employees may not have the resources they need once they reach retirement age, a reality that raises broader societal concerns about income insecurity over the long term.

Employers and government policymakers are examining ways to increase participation in savings plans such as individual retirement accounts (IRAs) or 401(k)s through built-in mechanisms, including automatic enrollment of new workers and automatic increases in employee contribution rates up to a certain percentage. In both cases, workers could choose to opt out.

This brief—based on an online survey conducted in 2016 of 1,991 workers with access to employer-sponsored plans at small and midsize businesses with five to 500 employees—examines how these workers perceive approaches in their employers’ plans intended to boost savings, known as pro-savings features.

Discussions at a series of focus groups help further elucidate worker attitudes. These groups addressed perceptions of state-sponsored IRA programs with automatic enrollment, known as auto-IRAs. Participant comments highlight how some see the pro-savings features as an overreach, impinging on their ability to manage their own savings.

Among the key findings:

-

Employer contributions and pay increases are among the factors that nonparticipating workers say would make them more likely to contribute to an available employer-sponsored retirement plan.

-

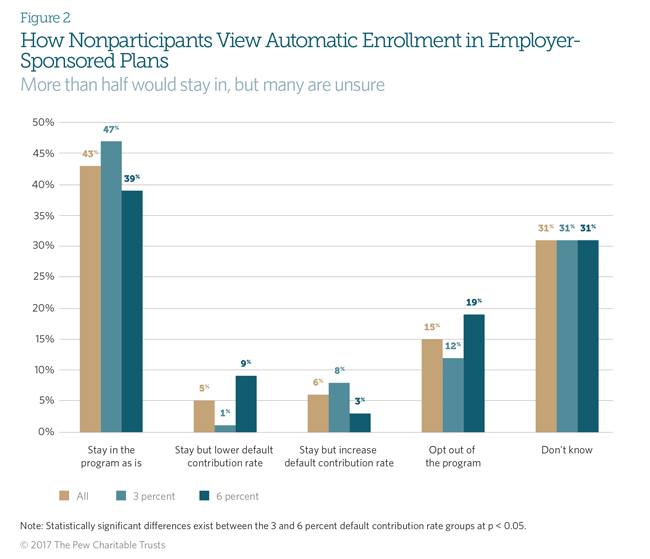

Fifty-four percent of those who do not participate in an available plan say they would stay in their employer’s plan if they were enrolled automatically with the ability to opt out.

-

Still, almost a third say they are undecided on whether they would stay in a plan.

-

-

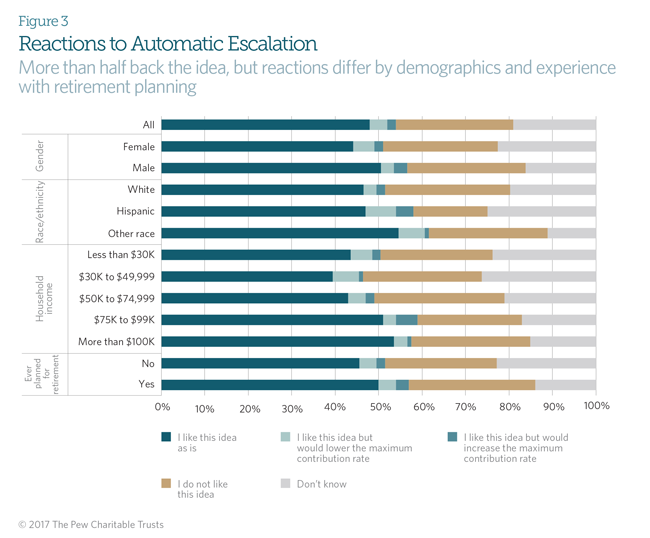

Fifty-six percent of all workers support the concept of encouraging greater savings through automatic escalation of employee contributions annually until they reach a ceiling, even when workers would not receive pay increases.

-

Reactions to automatic escalation differ by race/ethnicity, gender, household income, and retirement planning—particularly in the percentage of undecided responses.

-

What would encourage greater plan participation?

Workers who did not contribute to available plans cited a variety of reasons.1 In focus groups, some cited economic concerns: They could not afford to save or they worried about low returns on their investments or difficulty accessing these funds. Others said they were ineligible because of plan requirements, such as a minimum number of hours worked.

Focus Groups Highlight Why Some Workers Do Not Participate in Company Plans

“Early in my career I was in IRAs, and I put in as much money as I could. Ultimately, I didn’t see the benefit of it. I really needed access to capital for something, and it was difficult to get to. And there were big penalties to get the money out. I didn’t see the performance from the stock market. And so at this point, at 57 years old, I can probably do better without putting it into a fund. Although if I was getting 11 percent, I might reconsider.”

—Participant from a small/medium-size business in Atlanta

“I’ve done all kinds of 401(k)s throughout my life, and I’m kind of older, and almost every time there’s come a time in my life where I had to cash out. And now living expenses are so high, I just can’t afford to put anything in there.”

—Participant from a small business in San Jose, California

“You’ve got to be there a certain amount of time.”

—Participant from a medium-size business in Philadelphia

“Because they don’t match.”

—Participant from a small business in San Jose, California

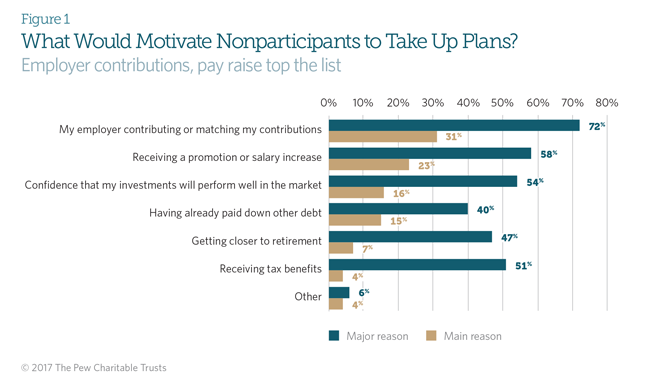

The survey sought to gauge how likely a series of factors were to motivate workers to contribute to employer- sponsored retirement plans.

Almost a third of those surveyed said they would contribute if their employer also did so, and 23 percent said they would be more likely to participate if they received a promotion or salary increase. (See Figure 1.) Though about half said that getting closer to retirement or receiving tax benefits would motivate them to take part, these were the least common “main reasons,” suggesting that for many respondents such factors alone would not push them to participate. Many also said they would be more likely to participate after paying down other debt. These findings indicate that no one change is likely to push a worker to participate. However, the most commonly cited reasons tended to be economic in nature.

The type of industry appears to play a role in worker perceptions of automatic enrollment. Only 7 percent of those in wholesale and retail trade jobs said they would opt out, compared with 31 percent of those in production, transportation, and material moving.3 Between 10 and 15 percent of respondents in other industries said they would choose not to take part in the plan. The characteristics of an industry may help explain such differences; for example, some are more likely to have high percentages of full-time workers or have higher wages or less income volatility.4

Workers with and without access to employer-sponsored retirement plans were asked in the focus groups for their impressions of automatic enrollment in a state-sponsored auto-IRA plan.5 The survey results are not directly comparable to findings from the focus groups because workers who had access to a plan but did not participate were asked about automatic enrollment by their current employer. Still, the discussions were revealing. Although some in the groups reacted negatively to the concept of automatic enrollment in a state-backed plan, many who had experience with this feature in previous jobs saw it as a good way to encourage savings.

Focus Groups: Views on Automatic Enrollment

“I don’t feel the employer should make that choice for you.”

—Participant from a medium-size business in Philadelphia

“If you’re going to take money out of my check, I better say that’s OK to do. And it shouldn’t just be that I didn’t get around to it and so you’re going to take it anyway.”

—Participant from a small business in San Jose, California

“I think nowadays everyone tends to be really lazy. We get the notifications, but we just put it to the side. If it wasn’t for being automatically enrolled, I would have never started saving.”

—Participant from a small business in Atlanta

Participant from a medium-size business in Chicago: “Frankly, in the beginning, when I was enrolled, it was in my paperwork. You had so many documents. I’m, like, ‘Didn’t read that.’ ‘Forgot about it.’ And so when they started taking out 3 percent and I saw my check, it was a big shock.”

Moderator: “So did it bug you?”

Participant: “In the beginning. But now I wish I could even contribute more. I’m happy that it’s there.”

Survey participants additionally responded to questions about automatic escalation—when contributions are increased by a certain percentage annually until they reach a ceiling. For respondents who were shown a 3 percent default contribution, the maximum was 7 percent; for those with a 6 percent default, the maximum contribution was 10 percent.

Survey respondents showed less support for automatic escalation than for automatic enrollment, but a majority—54 percent—still said they would participate. (See Figure 3.) Reactions to the concept varied by gender, race/ethnicity, household income, and retirement planning. Hispanic workers were less likely than non-Hispanics to say they did not like this feature (17 percent compared with 27 to 29 percent), but they were 25 percent more likely than white workers to say they did not know whether they would take part. Women were 44 percent more likely than men to say they did not know what they would do in this situation.

Those in households that earned less than $75,000 per year were at least 25 percent more likely to say they did not know if they would participate than those in households with $75,000 or more in income. Finally, those who had never planned for retirement were more likely to say they did not know than those who had.

Some demographic groups may be more averse to investing for the future because they have less disposable income. For example, Hispanic Americans are more likely to face unemployment than white Americans.6 These realities may make certain groups more hesitant to lock away a higher percentage of their incomes if they may need that money before retirement.

Conclusion

Employers and policymakers looking to address retirement insecurity by increasing participation in and contributions to retirement plans can do so via plans that make it easier for workers to save. The survey and focus groups indicate that there is no single factor, such as employer contributions or a pay increase, that would motivate workers to voluntarily participate in available employer-sponsored plans.

However, the survey found that at least half of those who have chosen not to participate in a workplace plan might do so if automatically enrolled. Moreover, the differences in perceptions among demographic groups on automatic enrollment were slight, suggesting that it could be an effective means to close gaps in participation.

By contrast, the differences among groups were more pronounced on the idea of automatic escalation of contributions. Making clear to potential plan participants that they could change their contribution amounts could help increase confidence in automatic escalation.

Endnotes

-

The Pew Charitable Trusts, “Employer-Sponsored Retirement Plan Access, Uptake, and Savings” (2016), http://www.pewtrusts.org/en/research-and-analysis/issue-briefs/2016/09/employer-sponsored-retirement-plan-access-uptake-and-savings.

-

Government Accountability Office, “Retirement Security: Most Households Approaching Retirement Have Low Savings” (2015), https://www.gao.gov/assets/680/670153.pdf.

-

Material moving includes occupations such as delivery-truck drivers, railroad workers, and material moving machine operators. See Bureau of Labor Statistics, “Occupational Outlook Handbook: Transportation and Material Moving Occupations” (Dec. 17, 2015), https://www.bls.gov/ooh/transportation-and-material-moving/home.htm.

-

The Pew Charitable Trusts, “Having a Retirement Plan Can Depend on Industry or Hours Worked” (2016), http://www.pewtrusts.org/en/research-and-analysis/issue-briefs/2016/11/having-a-retirement-plan-can-depend-on-industry-or-hours-worked.

-

For more information on such plans, see The Pew Charitable Trusts, “How States Are Working to Address the Retirement Savings Challenge” (2016),http://www.pewtrusts.org/en/research-and-analysis/reports/2016/06/how-states-are-working-to-address-the-retirement-savings-challenge.

-

Bureau of Labor Statistics, “Employee Tenure in 2016” (Sept. 22, 2016), https://www.bls.gov/news.release/tenure.nr0.htm.

America’s Overdose Crisis

Sign up for our five-email course explaining the overdose crisis in America, the state of treatment access, and ways to improve care

Sign up

Workers React Positively to Steps to Make Retirement Saving More Automatic

Survey shows employees at small businesses support auto-enrollment in workplace plans

ADDITIONAL RESOURCES

Fact Sheet

Podcast