Many Workers Have Limited Understanding of Retirement Plan Fees

Survey of employees at small and medium-sized businesses shows most do not review fee disclosures routinely

Overview

Retirement savings plans such as 401(k)s usually place the responsibility for selecting and managing investments with individual workers. These choices can feel overwhelming for many employees, who may be unsure how much they need to save, have more pressing financial concerns than saving for what feels like a far-off retirement, and often lack the financial resources or educational background to get the information they need to make informed retirement planning choices.

Workers who feel ill-prepared to navigate the various investments in their plans may also be unfamiliar with the investment fees the plans charge. And the consequences can be meaningful: Even small increases in investment fees can significantly reduce an employee’s overall savings at retirement. And analyses have shown that investments with higher fees do not typically perform better than those with lower fees.

In 2016, The Pew Charitable Trusts conducted a nationally representative online survey of nearly 3,000 private sector workers that focused on retirement planning issues and included questions to gauge workers’ knowledge of and familiarity with fees and how they relate to their handling of financial decisions and investments. The survey included questions about whether respondents had conducted simple retirement planning exercises and assessments of their tolerance for investment risk. This analysis, based on the results of the survey, examines how worker familiarity with investment fees is associated with confidence in investing and planning for retirement. The findings are limited to the 1,923 respondents who said they had retirement plans, though the survey included those without plans as well.

Among the key findings:

- Nearly 7 in 10 respondents with retirement plans said they were at least somewhat familiar with their plan’s fees. Still, 31 percent were not at all familiar with the fees.

- Roughly two-thirds had not read any investment fee disclosure in the previous year. Even among those who said they were very familiar with their fees, 33 percent hadn’t read any fee disclosures in the past year.

- Of the third who had read a fee disclosure, nearly 7 in 10 said they found the information understandable. Still, only 25 percent of all respondents said they had read and understood a disclosure about retirement account fees.

- Roughly 4 in 5 workers said it would be at least somewhat useful to have additional information about investment fees.

- Hispanics, women, younger workers, respondents with lower levels of education, and low-income workers were among the least likely to be familiar with the fees in their plans. On average, workers in these groups are less likely than other workers to be financially literate or to have experience with the financial system.

- Workers who had engaged in retirement planning at some point were more likely than those who had not to be familiar with their retirement plan fees. Those who were more confident about investing were more likely to say that it would be helpful to have more information about fees.

Familiarity with retirement plan fees

Most workers with retirement plans have defined contribution plans, such as 401(k)s or individual retirement accounts (IRAs). In contrast to employees who have traditional pensions or defined benefit plans, workers in these plans shoulder all the risks, including the possibility of investment losses and of outliving accumulated savings.1 The burden of making investment decisions can be complicated, in part because many workers are unsure how much they will need to have saved to retire.2 Workers must evaluate investments, including how much they are charged for management of their savings when they invest in a particular fund.3

Workers have choices when deciding how to invest their retirement savings. Workplace savings plans on average have 22 investment options, but the range of choices can vary, depending on the size of the plan. For example, in the smallest market segment examined—with assets between $1 million and $10 million—84 percent offer an index fund, a mutual fund with a portfolio that matches or tracks components of a market index, such as the Standard & Poor's 500. That number jumps to 98 percent among the largest plans. Fees tend to be higher for small plans; investor costs for small plans on average amount to 1.2 percent of assets per year, compared with 0.3 percent for the largest plans.4

Greater financial knowledge and literacy tend to be associated with better financial decisions and behavior, such as financial planning, saving, paying off loans in full, and accumulating greater wealth, although specific results vary. Those with more financial literacy often are able to earn higher returns on their retirement investments.5 Separate research has found that those who assess themselves as financially knowledgeable are more likely to select low-cost investments.6

Although analysts have found that those with greater financial literacy are more likely to make good financial decisions, evidence of the ability of financial education to increase literacy and knowledge and lead to better financial behavior is more mixed.7 Lack of familiarity with fees can lead workers to invest in higher-cost funds unknowingly, and even small differences in fees can have a large impact on overall savings over the course of a career.8

For example, a person earning about $60,000 a year who chooses a plan with high fees over one with low fees could see a difference of nearly $170,000 in the total value of investments at retirement after a 40-year career, an amount equal to working nearly three additional years.9 And research shows no advantage, in terms of market performance, in choosing a plan with higher fees, which does not typically produce higher returns than a comparable fund with lower fees.10

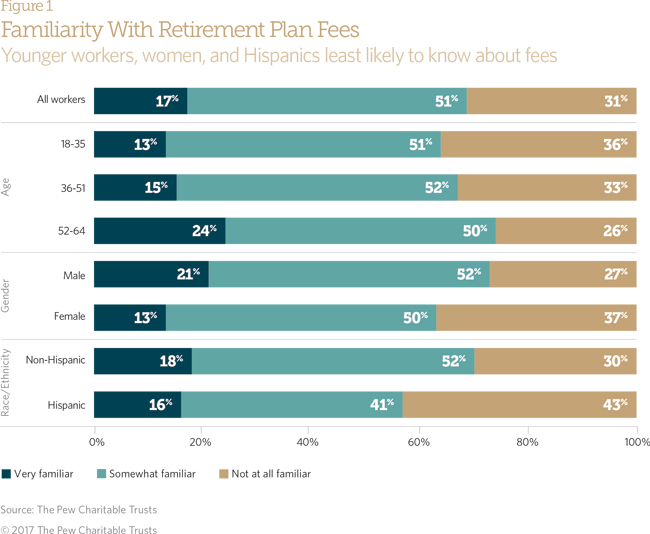

About 7 in 10 workers with retirement plans said they were at least somewhat familiar with the fees charged for managing funds in those plans. On the other hand, 31 percent said that they were not at all familiar with the fees they pay.

Among those with retirement plans, nearly two-thirds said they had not read any of the fee disclosures from their plans in the past year. Not surprisingly, workers who said they had read a fee disclosure were more likely to be familiar with the fees they were charged.

Familiarity With Plan Fees

These survey questions are the basis of this analysis:

How familiar are you with the fees for managing the investments in your retirement plan?

- Not at all familiar

- Somewhat familiar

- Very familiar

To the best of your recollection, have you read any investment fee disclosure documents from funds in your retirement plan in the past year?

- Yes

- No

- Don’t know

Was the information in the fee disclosure understandable?

- Yes

- No

Just 13 percent of those who were not at all familiar with their fees said they had read a fee disclosure in the past year, compared with 67 percent of those who said they were very familiar with those fees. Still, this means that nearly one-third of those who said they were very familiar with their fees had not read their fee disclosure.

Nearly 4 in 5 of those with retirement plans said it would be somewhat or very useful to have additional information about investment fees. This may suggest that although many workers may be familiar with their retirement fees, they recognize the limits of their own knowledge and could benefit from additional information.

Older workers were more likely than younger workers to say they were familiar with the fees in their retirement plan. About a quarter of workers ages 52 to 64 said they were not at all familiar, roughly the same proportion who said they were very familiar.11 More than a third of those ages 18 to 35 said they were not at all familiar with these fees, while just 13 percent were very familiar. Perhaps because workers may pay greater attention to their investments and fees as they near retirement, older workers also were more likely to have read a fee disclosure in the past year. At the same time, there were no significant differences among age groups in the rate at which workers reported understanding the information in the fee disclosure.

Although older workers may be more familiar with their plan fees, younger workers stand to benefit the most from reducing the costs associated with these fees, all else being equal, because they have the most years to work before retiring—meaning that any savings they accrue by reducing fees will have more time to compound and yield greater returns.

Hispanic workers, meanwhile, were less likely than non-Hispanics to be familiar with their retirement plan fees. Some 43 percent of Hispanics said they were not at all familiar with the fees they were charged, compared with 30 percent of non-Hispanics.12 Research shows that Hispanics tend to have less access to retirement plans than other racial and ethnic groups and as a result could have less experience with plan features such as fees.13

Women were also less likely than men to be familiar with fees, with 37 percent saying they were not at all familiar, compared with 27 percent of men.14 However, women and men were equally likely to have read a fee disclosure within the past year (36 percent versus 37 percent, respectively) and to have said that the information in the disclosure was understandable.

Education, household income, and familiarity with fees

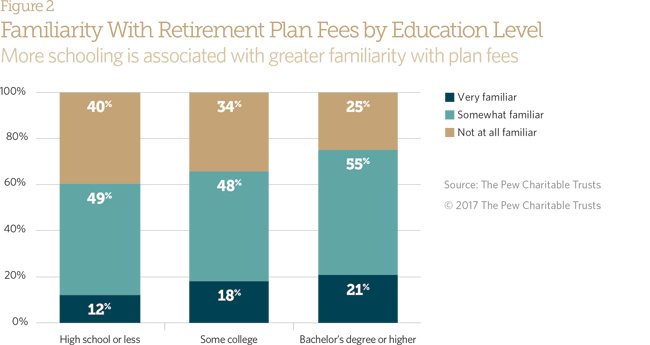

Workers with more education tend to have higher rates of access to and participation in retirement plans than those with less education; a similar disparity is apparent in familiarity with retirement plan fees.15

Four in 10 workers with a high school diploma or less education said they were not at all familiar with their fees. Among those with at least a bachelor’s degree, that drops to a quarter.16 Employees with more education also were more likely to have read and understood their fee disclosure. Just over a quarter of those with a high school degree or less said they had read their fee disclosure; more than 4 in 10 with at least a bachelor’s degree said the same thing.

Education often can be a proxy for financial literacy or a marker of higher income, both of which are important factors in worker understanding of and familiarity with plan fees. Still, a large proportion of those with at least a bachelor’s degree acknowledged having no familiarity with their plan fees.

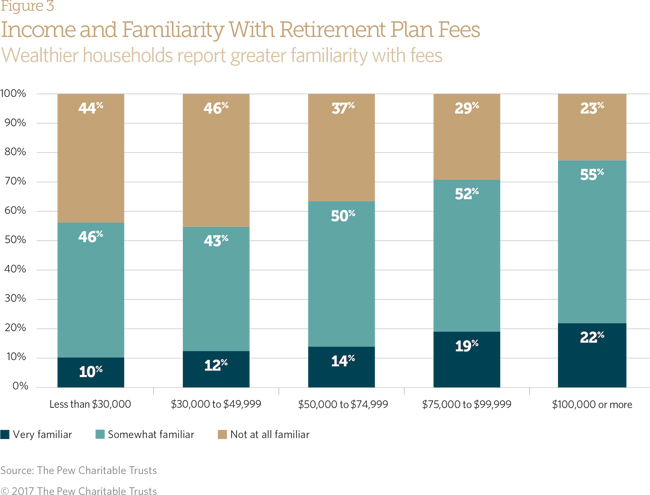

Workers’ familiarity with plan fees varies with household income. Among those earning less than $30,000, more than 4 in 10 of those with a retirement plan said they were not at all familiar with their fees.17 Just 23 percent of those with household incomes of at least $100,000 said they were not at all familiar with these fees; 77 percent were very or somewhat familiar. Higher-income workers also were more likely to have read a fee disclosure from their retirement plan within the previous year. However, among those with retirement plans who read their disclosures, those with higher incomes were not more likely than others to say they understood the details. People in higher-income households are more likely to have had experience with retirement plans, and therefore also the accompanying fees.

Planning for retirement

With Americans today typically living into their 80s or 90s, determining how much money workers will need for living expenses, leisure activities, and health and long-term care expenses in retirement can be difficult. Although this level of uncertainty makes planning more important, some workers may lack the skills, capacity, or motivation to calculate how much they might need to save. Workers also may find their retirement plan fees complex and difficult to understand, deterring them from familiarizing themselves with their fees.

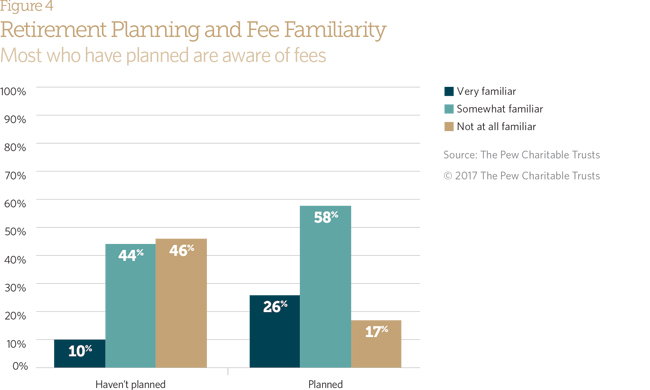

Just 50 percent of workers with retirement accounts said they had planned for retirement by trying to figure out how much they would need to save. Among those who had not estimated how much they needed to save, nearly half (46 percent) said they were not at all familiar with the fees associated with managing their retirement investments. Just 10 percent said they were very familiar with the fees, while 44 percent said they were somewhat familiar. On the other hand, among those who said they had estimated the amount they would need in retirement, 26 percent said they were very familiar and 58 percent said they were somewhat familiar with the fees charged by their plans. Just 17 percent of those who said they had planned said they were not at all familiar with their fees.18 Some 76 percent of those who said they had not estimated how much they would need for retirement also had not read any of their fee disclosures.

But although having engaged in retirement planning is clearly associated with fee familiarity, it is not clear how they are linked: Engaging in planning might increase fee awareness or vice versa. People who have planned might have greater financial literacy, which could include experience with investments or education on fees. Workers who are less aware of their fees, who therefore could see their retirement savings diminished by higher costs, also may be doing less to prepare for retirement. In any event, looking at levels of education and financial literacy, as well as access to financial planning resources, does not suggest that planning for retirement on its own would necessarily increase familiarity with retirement plan fees.

Confidence in investing

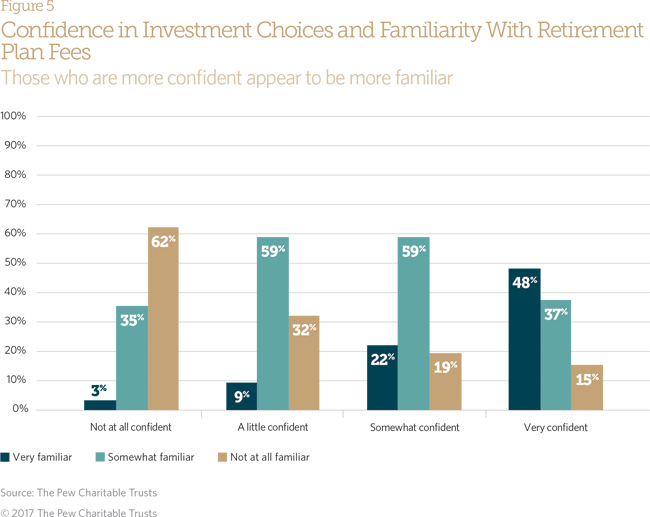

Research on investor confidence and behavior has shown that individuals who overestimate their financial knowledge and investment performance are more likely to make poor investment decisions.19 And workers’ confidence in their ability to make the right investment decisions can be related to their level of familiarity with their retirement plan fees. Among those who said they were not at all confident in their ability to make the right investment decisions, only 3 percent were very familiar with their fees; 62 percent were not at all familiar. (See Figure 5.)

On the other hand, majorities of those who felt a little or somewhat confident in their ability to make the right investment choices said they were somewhat familiar with their retirement fees. Nearly half of those with a retirement plan who felt very confident in their ability to make the right investment decisions said they were very familiar with their plans’ investment fees. Only 15 percent of those who were very confident said they were not at all familiar with their retirement plan fees.20

However, more than 6 in 10 who said they felt very confident in their investment choices also said they had read a fee disclosure. Those with greater confidence were more likely to have understood the disclosure when they read it and were also more likely to say that it would be helpful to have more information about fees. However, 15 percent of those who said they were very confident in their investment choices also said that they were not at all familiar with fees.

Risk tolerance and fee familiarity

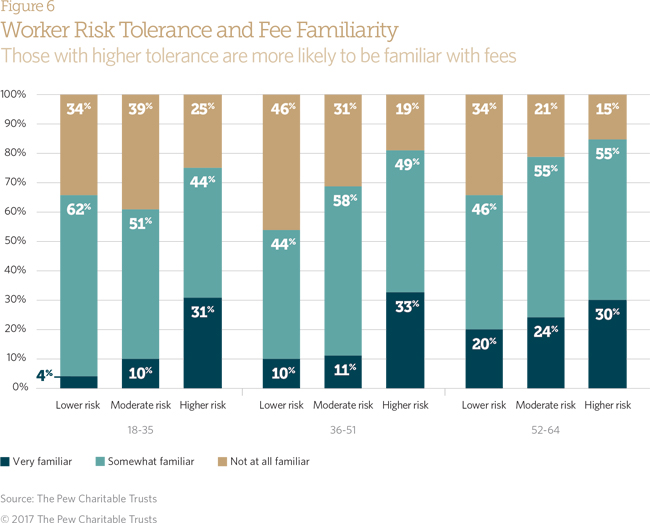

Tolerance for taking on risk in investing is another factor associated with awareness of plan fees. The survey asked workers if they would prefer to put money in three types of investments: those with a lower risk of loss but with the potential for smaller gains, those with moderate risk but with potential for moderate gains, or those with a higher risk of loss but the potential for the greatest gains. Older workers were more likely than younger ones to prefer low-risk investments. Nearly 3 in 10 (28 percent) of those ages 52 to 64 preferred the lower-risk option, compared with just 19 percent of those 18 to 35. Younger respondents’ willingness to expose themselves to greater investment risk aligns with typical asset allocation and risk management guidance, which calls for workers to gradually reduce their risk exposure as they age. (See Figure 6.)

Across age groups, those who said they were more familiar with their retirement plan’s fees were more likely to say they preferred higher-risk investment options. However, only 4 percent of workers 18 to 35 who preferred low-risk investments said they were very familiar with their plan fees, compared with 20 percent of those 52 to 64.21 This means that many young workers who lack familiarity with their fees may also be investing in lower-risk investment options at a time when they could take on greater risk in hopes of realizing greater returns over the course of their careers.

Because they have more time to recover from losses, younger workers can generally take on higher-risk investments, such as stocks, which have the potential for higher returns over time than other investments. Overall, workers with greater familiarity were more likely to choose higher-risk investments, but that doesn’t necessarily mean that higher-risk options are better. Additional research on the relationship between retirement plan fee familiarity and investment risk may shed greater light on workers’ risk preferences.

Conclusion

Workers who are unfamiliar with the fees charged for managing their retirement funds are investing without fully understanding the costs associated with these plans. That is especially common for younger workers and those with less education. The survey results also indicate that workers who said they were unfamiliar with their plan fees also tended to be less confident in their ability to make the right investment choices. In addition, they were less likely to say they had planned for retirement by trying to figure out how much they would need to save. All of these factors make it more difficult to accumulate the savings needed for retirement.

Not surprisingly, workers closer to retirement reported greater familiarity with their fees than younger workers, although older workers are less likely to benefit from reducing the fees, which can mean less long-term savings. On the other hand, younger workers, with much of their careers ahead of them, can see significant savings by investing in lower-cost investments. Because of the impact of compounding, they will see greater growth over time.

Examining whether workers have read plan fee disclosures does not provide a full picture of their understanding of these costs. They may learn about fees through other means, such as speaking with a plan administrator or a financial adviser. But many also may be overstating their knowledge. In addition, greater familiarity with and understanding of fees can have only a limited impact in certain situations, particularly when workers have just a few choices in their plan investment menu.

Still, keeping fees down can make a big difference over time. Future research can explore the extent to which workers understand the fee and cost structures of their funds and how familiarity drives investment behavior.

Appendix

Survey questions about retirement plan fees

Questions on retirement plan fees were asked to those respondents who indicated they had a retirement plan, including an IRA, 401(k), or other pension plan. Question G5a was asked only of those who indicated they had read an investment fee disclosure document within the past year.

G4. How familiar are you with the fees for managing the investments in your retirement plan?

G5. To the best of your recollection, have you read any investment fee disclosure documents from funds in your retirement plan in the past year?

G5a. Was the information in the fee disclosure understandable?

G6. How useful would it be for you to have additional information about investment fees?

Methodological appendix

The Pew Charitable Trusts surveyed 2,918 Americans ages 18 to 64 who are employed and not working for the government using GfK’s probability-based internet panel, KnowledgePanel. The survey was released to a random sample of 15,872 panel members. GfK fielded the survey Aug. 2-23, 2016, in English and Spanish. Data were weighted to be nationally representative using several benchmarks (i.e., gender, race/ethnicity, education, census region, household income, language proficiency, and employment status). This brief looks at the subset that indicated they currently had a retirement plan, 1,923 respondents. Of these 1,923, 17 were classified as missing because they did not answer the survey question on plan fee familiarity. Figures 1-3 have a sample size of 1,906. Sample sizes for Figures 4, 5, and 6 are 1,829, 1,827, and 1,807, respectively.

Endnotes

- The Pew Charitable Trusts, “How States Are Working to Address the Retirement Savings Challenge: An Analysis of State-Sponsored Initiatives to Help Private Sector Workers” (2016), http://www.pewtrusts.org/~/media/assets/2016/06/ howstatesareworkingtoaddresstheretirementsavingschallenge.pdf.

- FINRA Investor Education Foundation, “Financial Capability in the United States 2016” (2016), http://www.usfinancialcapability.org/downloads/ NFCS_2015_Report_Natl_Findings.pdf.

- Ray Boshara et al., New America, “Consumer Trends in the Private, Public, and Nonprofit Sector” (2011), https://static.newamerica.org/attachments/3844-consumer-trends-in-the-private-public-and-non-profit-sector/BosharaetalNEFEConsumertrends. 4e455c765cec48e99759f11ae5669a8d.pdf.

- Investment Company Institute, “The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at 401(k) Plans, 2014,” (2016), https://www.ici.org/pdf/ppr_16_dcplan_profile_401k.pdf.

- Olivia S. Mitchell and Annamaria Lusardi, “Financial Literacy and Economic Outcomes: Evidence and Policy Implications,” the National Bureau of Economic Research, (2012), http://www.nber.org/papers/w18412; Robert Clark et al., “Financial Knowledge and 401(k) Investment Performance: A Case Study,” the National Bureau of Economic Research (2014), http://www.nber.org/papers/w20137.

- James J. Choi et al., “Why Does the Law of One Price Fail? An Experiment on Index Mutual Funds,” the National Bureau of Economic Research (2006), http://www.nber.org/papers/w12261.

- Marianne A. Hilgert et al., “Household Financial Management: The Connection Between Knowledge and Behavior,” Federal Reserve Bulletin 89, no. 7 (2003): 309–322, https://www.federalreserve.gov/pubs/bulletin/2003/0703lead.pdf. Hilgert et al. show that across four types of financial practices (cash flow management, credit management, saving, and investment) those with greater financial knowledge had better financial behaviors as measured by a series of financial practices indexes; Angela Lyons et al., “Are We Making the Grade? A National Overview of Financial Education and Program Evaluation,” The Journal of Consumer Affairs 40, no. 2 (2006): 208–235, http://dx.doi.org/10.1111/j.1745-6606.2006.00056.x. Lyons et al. find mixed evidence of the effectiveness of financial literacy education in improving outcomes and financial behaviors.

- U.S. Securities and Exchange Commission, Updated Investor Bulletin: How Fees and Expenses Affect Your Investment Portfolio, (Sept. 8, 2016), https://www.investor.gov/additional-resources/news-alerts/alerts-bulletins/updated-investor-bulletin-how-fees-expenses-affect.

- Pew analysis based on a hypothetical 25-year-old worker who earns an annual pretax income of $60,000 over a 40-year career who has the choice between a low- and high-cost retirement fund. This scenario assumes biweekly contributions to the fund of 8 percent of total pay, equaling $175 every two weeks. The high-cost fund charges a 1 percent annual operating fee, while its low-cost alternative charges 0.05 percent. Both funds are assumed to have the same 6 percent annual rate of return.

- William F. Sharpe, “The Arithmetic of Investment Expenses,” Financial Analysts Journal 69, no. 2 (2013): http://dx.doi.org/10.2469/faj.v69.n2.2; John C. Bogle, “The Arithmetic of ‘All-In’ Investment Expenses,” Financial Analysts Journal 70, no. 1 (2014): http://dx.doi.org/10.2469/faj.v70.n1.1.

-

Chi-square tests of significance show significant differences in familiarity of retirement plan fees between age groups at p<0.05.

-

Chi-square tests of significance show significant differences in familiarity of retirement plan fees between Hispanics and non-Hispanics at p<0.05.

-

The Pew Charitable Trusts, “Employer-Sponsored Retirement Plan Access, Uptake, and Savings” (2016), http://www.pewtrusts.org/~/media/assets/2016/09/ employersponsoredretirementplanaccessuptakeandsavings.pdf.

-

Chi-square tests of significance show significant differences in familiarity of retirement plan fees between men and women at p<0.001.

-

The Pew Charitable Trusts, “Who’s In, Who’s Out: A Look at Access to Employer-Based Retirement Plans and Participation in the States” (2016), http://www.pewtrusts.org/~/media/assets/2016/01/ retirement_savings_report_jan16.pdf.

-

Chi-square tests of significance show significant differences in familiarity of retirement plan fees by educational attainment at p<0.001.

-

Chi-square tests of significance show significant differences in familiarity of retirement plan fees between income categories at p<0.001.

-

Chi-square tests of significance show significant differences in familiarity of retirement plan fees between those who have and have not planned for retirement by trying to figure out how much to save for retirement at p<0.001.

-

Colleen Tokar Assad, “Financial Literacy and Financial Behavior: Assessing Knowledge and Confidence,” Financial Services Review 24, no. 2 (2015): 101–117, http://eds.b.ebscohost.com/eds/pdfviewer/pdfviewer?vid=0&sid=bd81cf54-32cc-4233-bd1c-055cb745ecf8@sessionmgr103; Mark Grinblatt and Matti Keloharju, “Sensation Seeking, Overconfidence and Trading Activity,” The Journal of Finance 64, no. 2 (2009): 549–578, http://www.nber.org/papers/w12223.pdf; Brad M. Barber and Terrance Odean, “Trading Is Hazardous to Your Wealth: The Common Stock Investment Performance of Individual Investors,” The Journal of Finance 55, no. 2 (2000): 773–806, http://dx.doi.org/10.2139/ssrn.219228.

-

Chi-square tests of significance show significant differences in familiarity of retirement plan fees by levels of confidence in “ability to make the right investment decisions” at p<0.001.

-

Chi-square tests of significance show significant differences in familiarity of retirement plan fees by risk tolerance at p<0.001.

America’s Overdose Crisis

Sign up for our five-email course explaining the overdose crisis in America, the state of treatment access, and ways to improve care

Sign up

ADDITIONAL RESOURCES

Fact Sheet

Article