What Do Consumers Without Bank Accounts Think About Mobile Payments?

‘Unbanked’ customers cite concerns about loading funds, data security, and cellphone costs, survey finds

© Getty Images

© Getty ImagesOverview

Mobile payments technology allows customers to make online and point-of-sale purchases, pay bills, and send or receive money from their smartphones via Web browsers, apps, or text messages, and it has the potential to increase financial inclusion for consumers without bank accounts—the unbanked.1 To provide a better understanding of consumers’ views on the potential benefits and risks of mobile payments, particularly for this population, this chartbook presents findings from a nationally representative, Pew-commissioned telephone survey, focusing on consumers’ access to, usage of, and barriers to adoption of the technology, and compares responses of those with and without checking accounts. The key findings are:

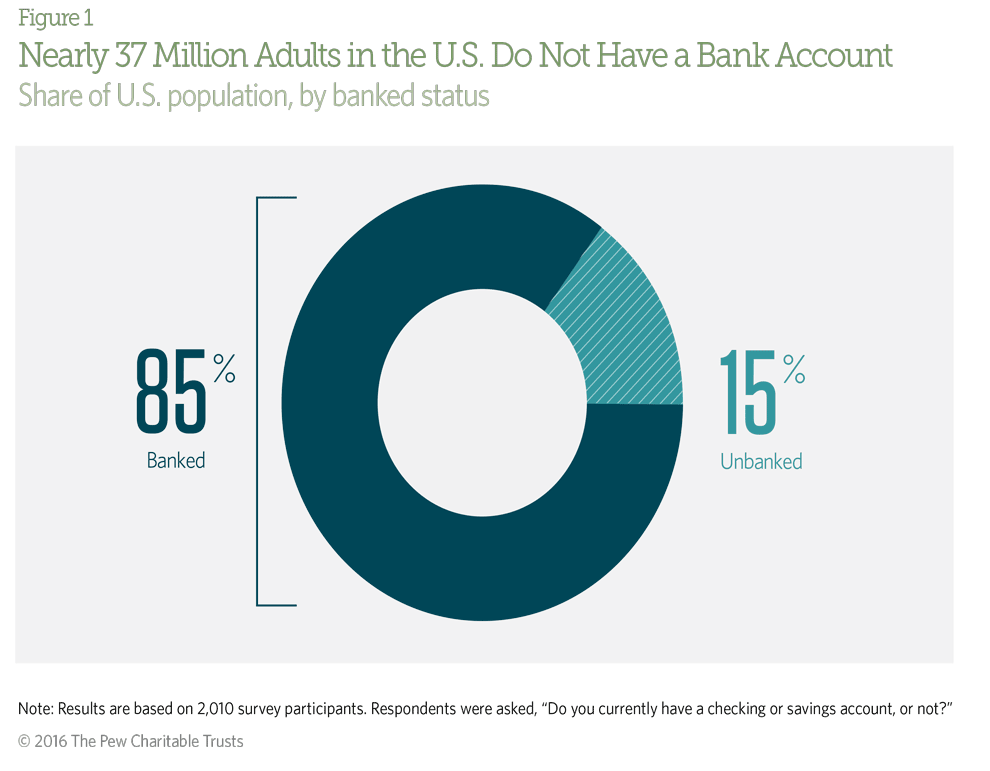

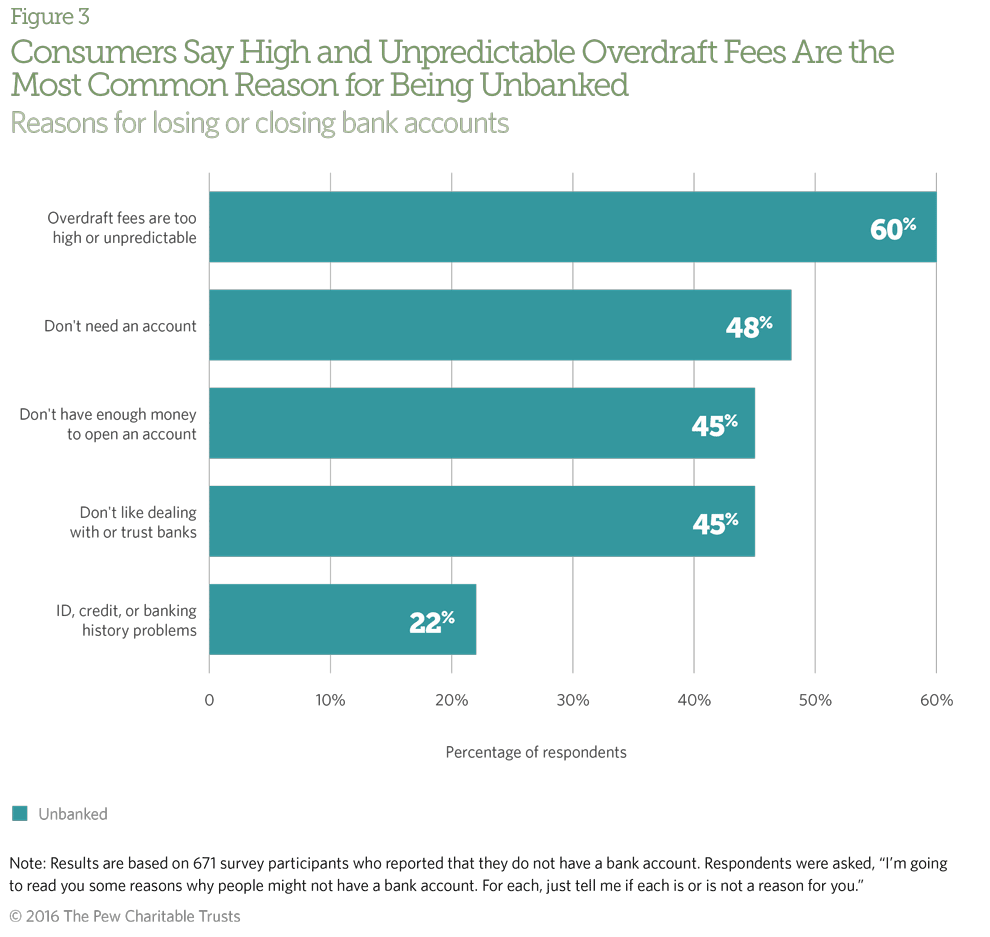

- About 15 percent of U.S. consumers—approximately 37 million adults— do not have a bank account; these consumers say overdraft fees are the most common reason they are unbanked.2

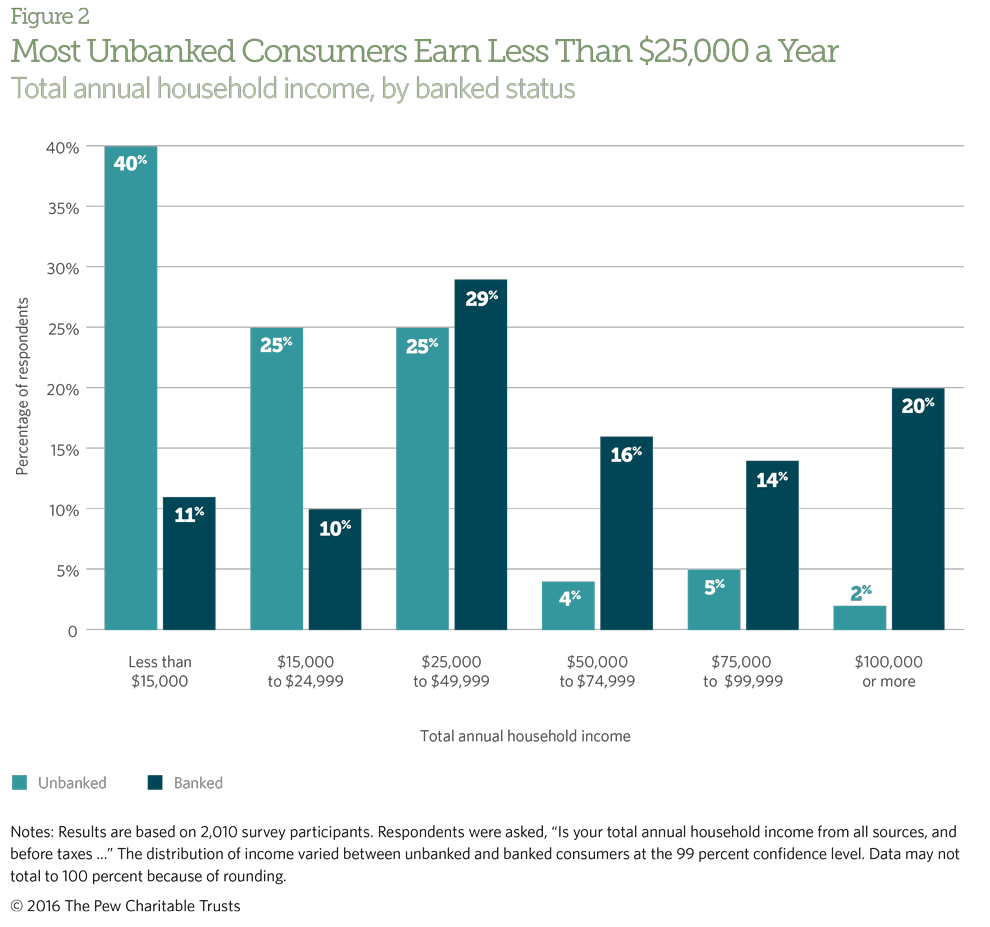

- The majority of unbanked consumers have household incomes under $25,000 annually.

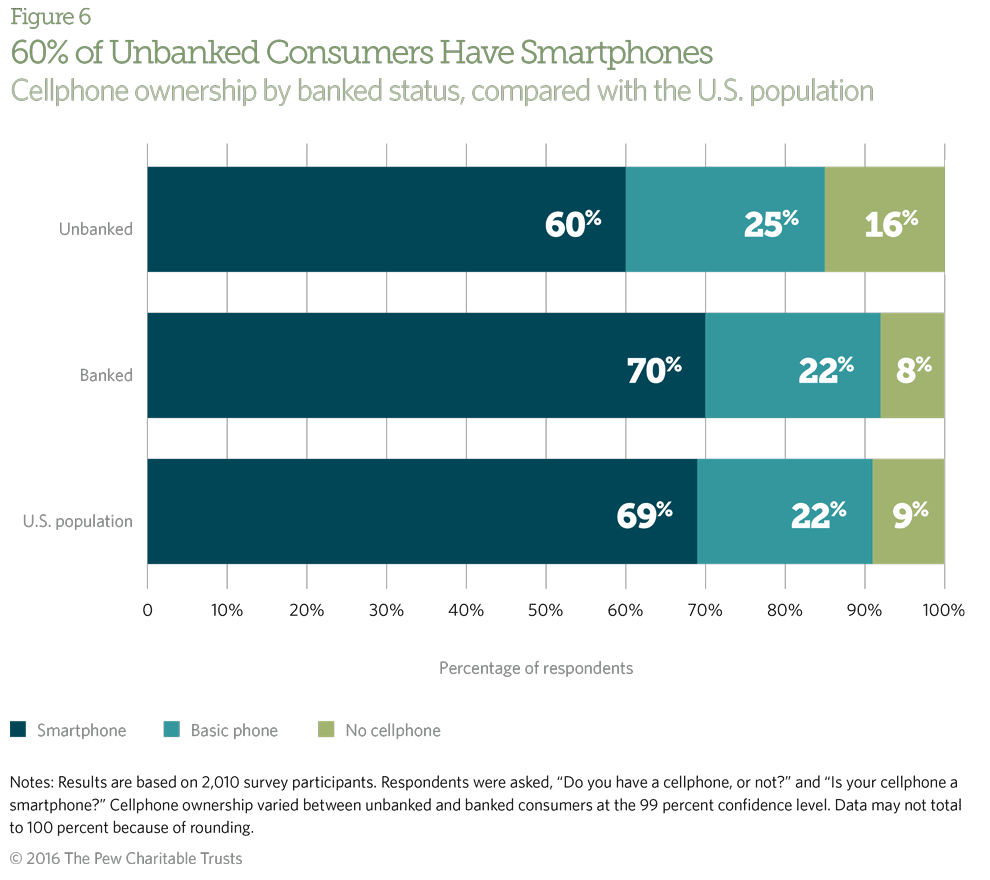

- About 6 in 10 unbanked consumers have a smartphone, but they are nearly twice as likely as banked consumers to suspend or cancel their cellphone plans because of the cost of maintaining coverage.

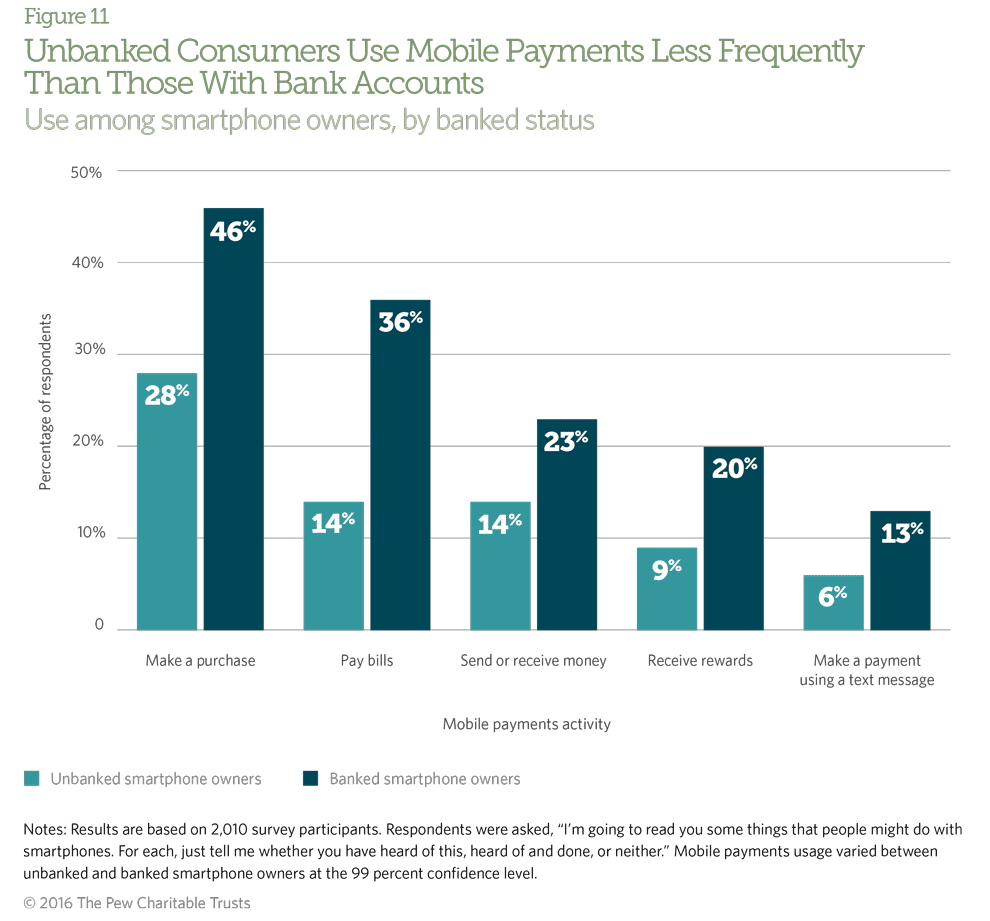

- Mobile payments use is significantly lower among the unbanked: About 39 percent of unbanked smartphone owners have ever made a purchase, paid bills, or sent or received funds using mobile payments technology compared with 64 percent of banked smartphone owners.

- Regardless of banking status, mobile payments users are more likely than nonusers to be millennials or Generation Xers.

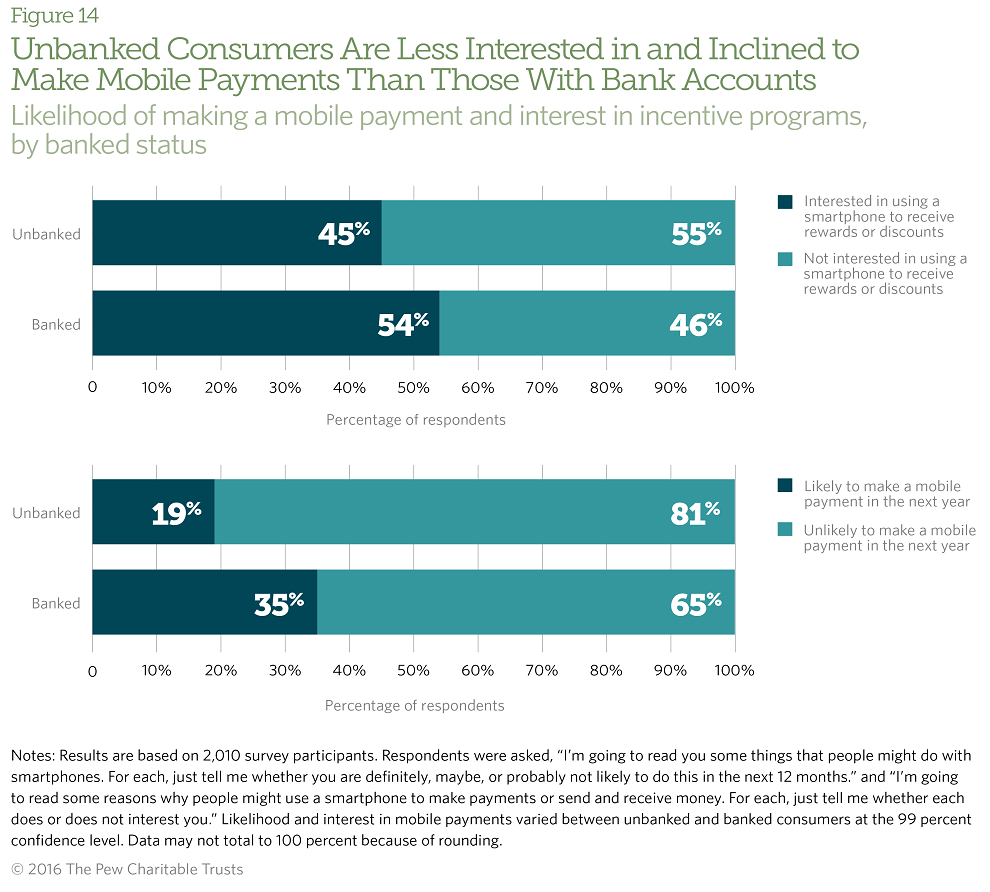

- Unbanked consumers are less likely than those with bank accounts to say that they will make a mobile payment in the next year and are less interested in using a smartphone to receive rewards and discounts.

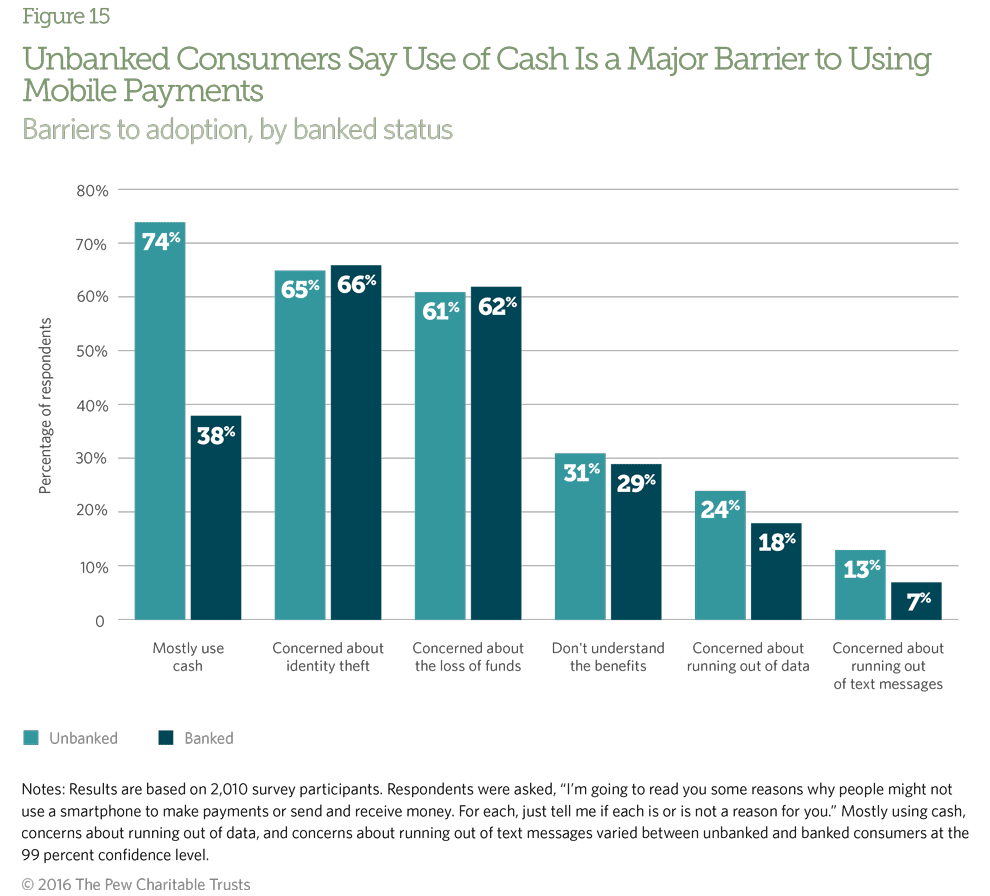

- The most significant barrier to mobile payments use for unbanked consumers is poor compatibility with paper checks, their most frequent form of income, and cash, which they use regularly for payments and purchases, even more than safety, which is the top concern of banked consumers.

The survey found that about 15 percent of U.S. consumers are unbanked, which translates to approximately 37 million adults and is consistent with the results of earlier research by the Federal Reserve Board.3 About 21 million of these people were previously banked, holding a median of two accounts. When asked whether they would like to have a checking or savings account in the future, 77 percent say no.

For a typical fee of $35, most U.S. banks allow consumers to overdraw their accounts when they don’t have sufficient funds to cover debit card point-of-sale and ATM transactions.4 The Consumer Financial Protection Bureau has shown that the median transaction amount of debit card purchases that incurred such a fee was just $24.5 On average, people who paid an overdraft penalty fee also incurred additional fees, for a total of $69 the last time their account was overdrawn.6 Overdraft fees are a major reason that many checking account holders exit the banking system, which reduces their access to lower-cost, mainstream financial services and puts them at greater risk of loss or theft of funds.7

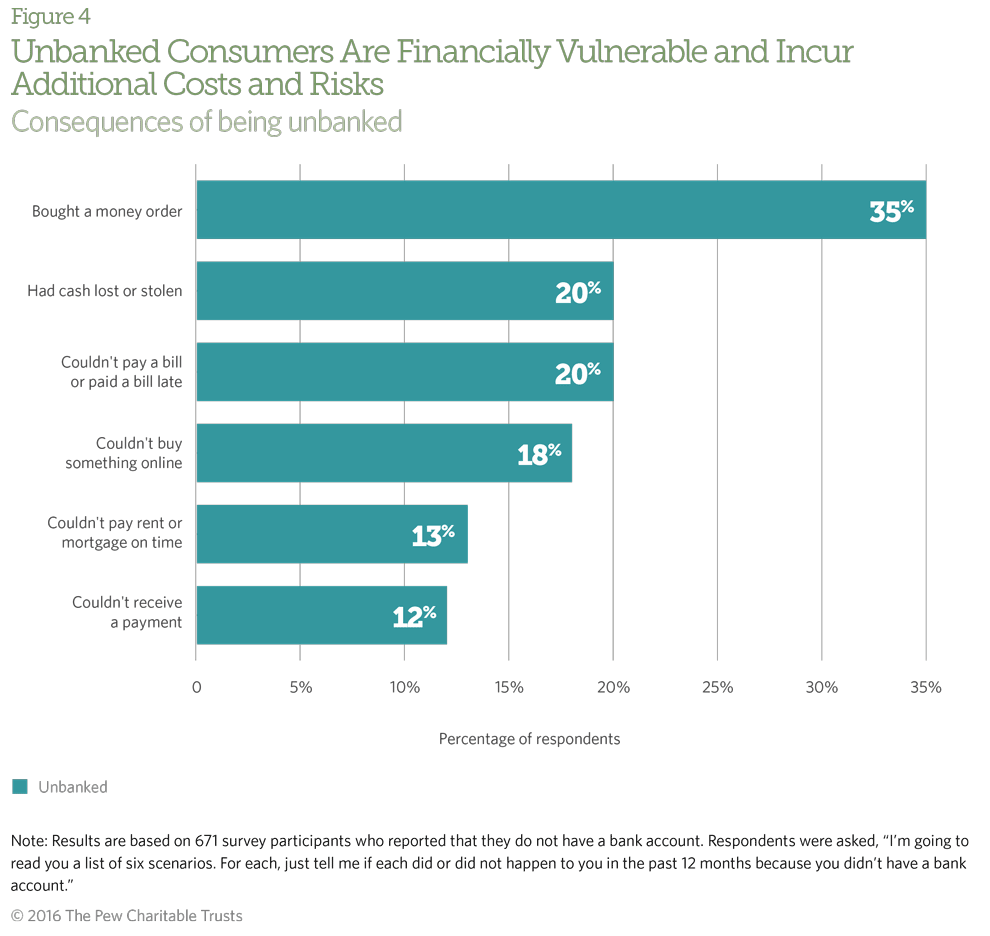

Sixty-five percent of the unbanked earn less than $25,000 a year, and these low-income consumers incur additional costs and risks because they lack access to mainstream banking services. For example, 20 percent of unbanked consumers reported having cash lost or stolen. A study of low-income Los Angeles area households, for example, found that the average unbanked consumer lost the equivalent of nearly two weeks of household expenses when cash was lost or stolen.8

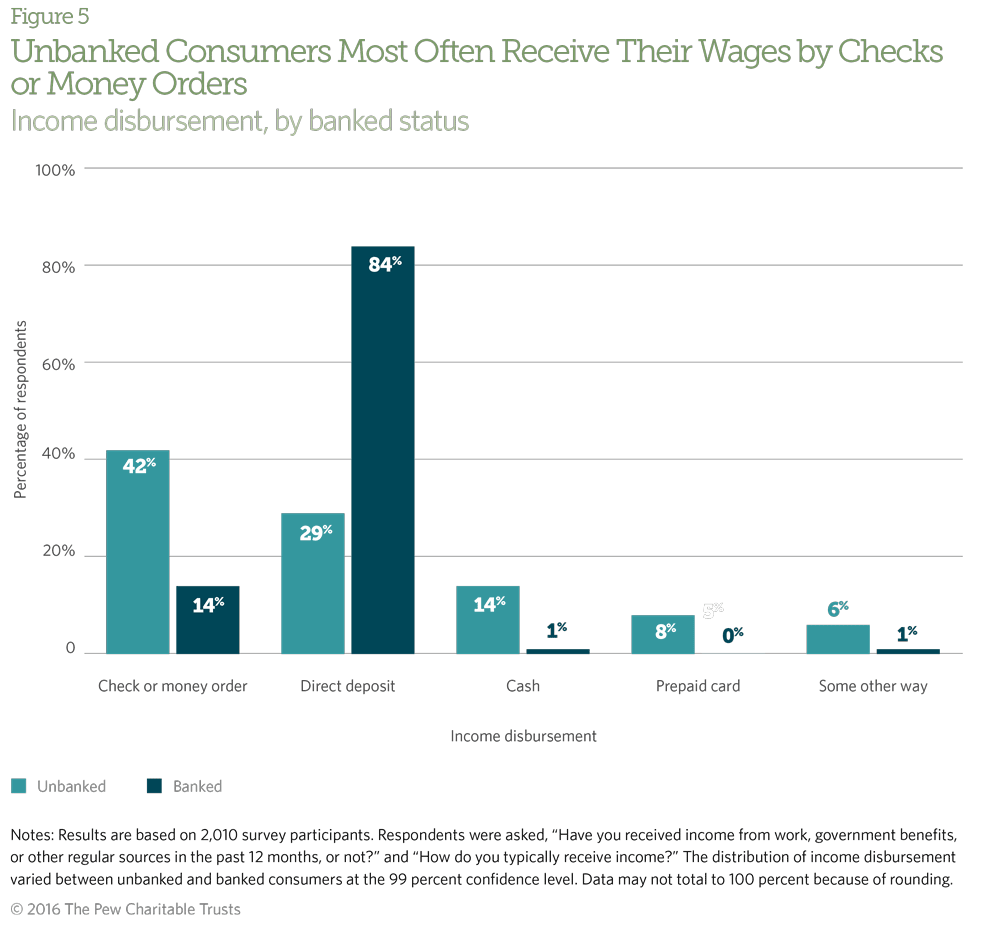

About 84 percent of banked consumers receive income through direct deposit, but the most common methods for unbanked consumers to receive income are checks or money orders. Prior Pew research shows that many unbanked consumers also receive income through direct deposit onto general purpose reloadable prepaid cards, which they use like checking accounts.9 In focus groups designed to gauge whether unbanked smartphone owners are interested in using their mobile devices as proxy bank accounts, unbanked consumers expressed interest in receiving direct deposit from an employer to a mobile payments app and in the ability to deposit checks using apps and phone cameras.10

Unbanked consumers are twice as likely as banked consumers to be without a cellphone, despite the fact that more than half of them have smartphones. Further, most unbanked consumers who own basic mobile phones don’t plan on buying a smartphone in the next year. Cellphones can be especially costly for lower-income consumers, such as most of the unbanked. Shared or family plans—which 68 percent of smartphone owners use—often cost between $100 and $200 a month.11

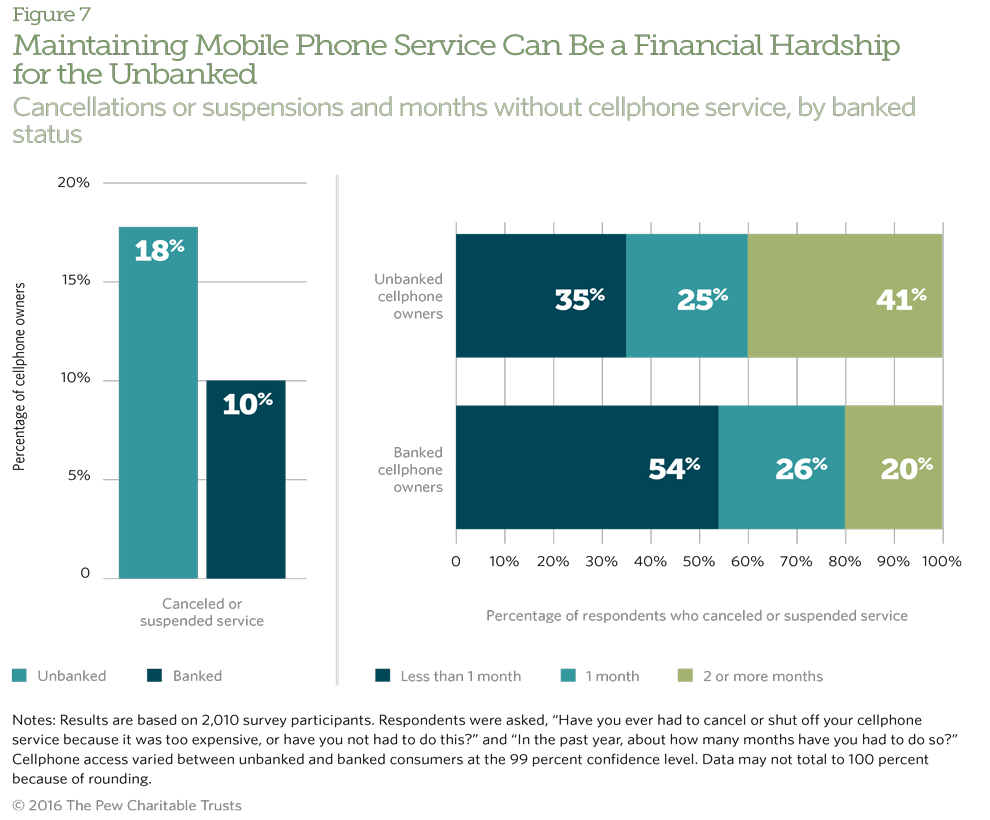

The unbanked are nearly twice as likely as banked consumers to have canceled their cellphone service in the past year because maintaining it was too expensive. Those who suspended service typically did so once and were without access for one month in the past year. From 2007 to 2014, the average annual cost of cellphone service rose from $608 to $963 a year.12 Most unbanked consumers gross less than $2,000 monthly, so maintaining cellphone service for a year could cost them nearly half a month’s pay.

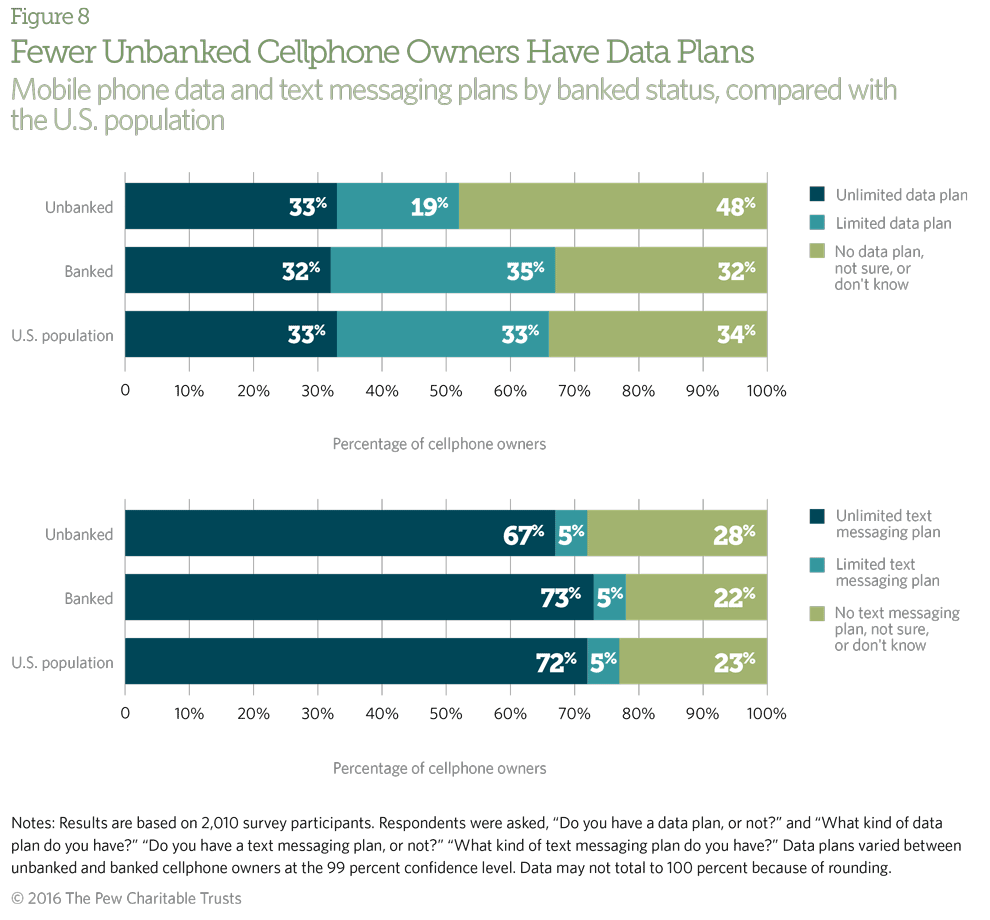

Text messaging is the most popular mobile phone activity regardless of age, gender, and income level.13 Text message and email are also the two most preferred ways that millennials would like to receive notifications from their financial institutions.14 In this survey, access to text messaging does not differ between unbanked and banked consumers, but access to data plans does.

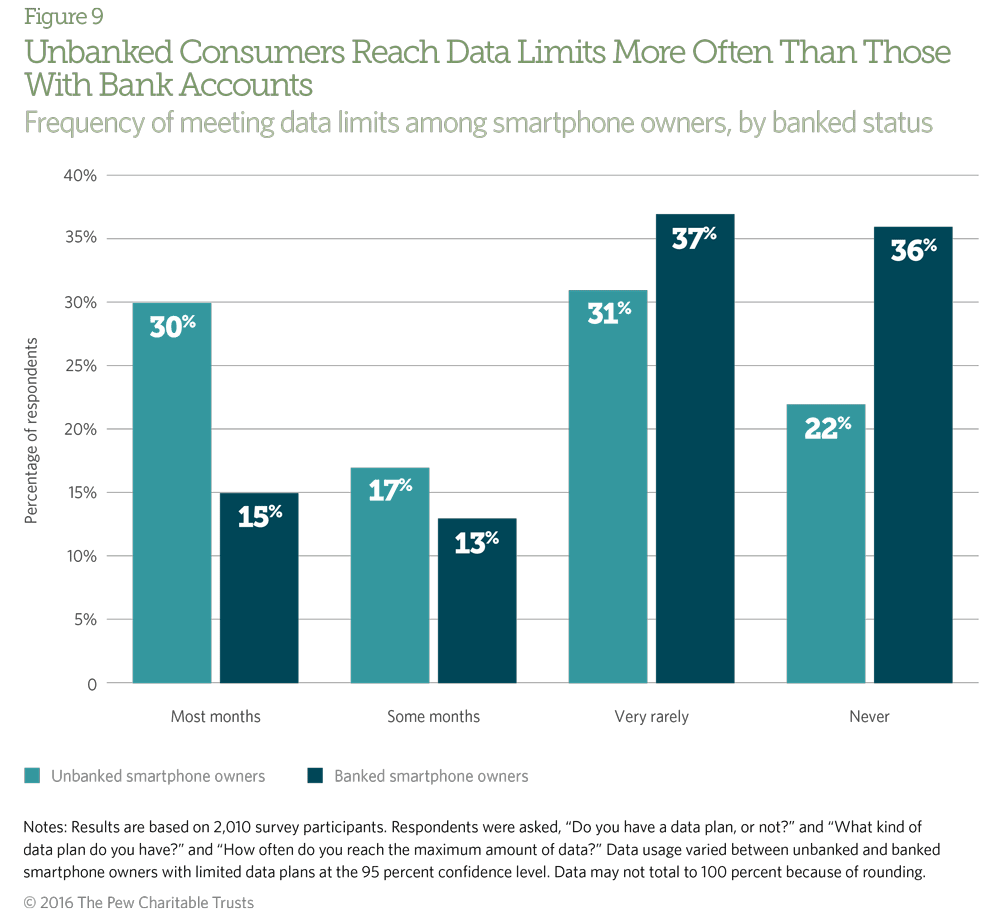

Among smartphone owners with limited data plans, nearly half of unbanked consumers reach their data limits most or some months, which indicates a high amount of use. About 7 percent of U.S. consumers rely exclusively on their smartphones for accessing the Internet (are smartphone-dependent).15 Households with incomes under $30,000 annually, which include about 60 percent of unbanked consumers, are almost twice as likely as the general population to be smartphone-dependent. Unless smartphone owners with limited data plans can access a Wi-Fi network or purchase additional data, they would be unable to use mobile payments technology regularly.

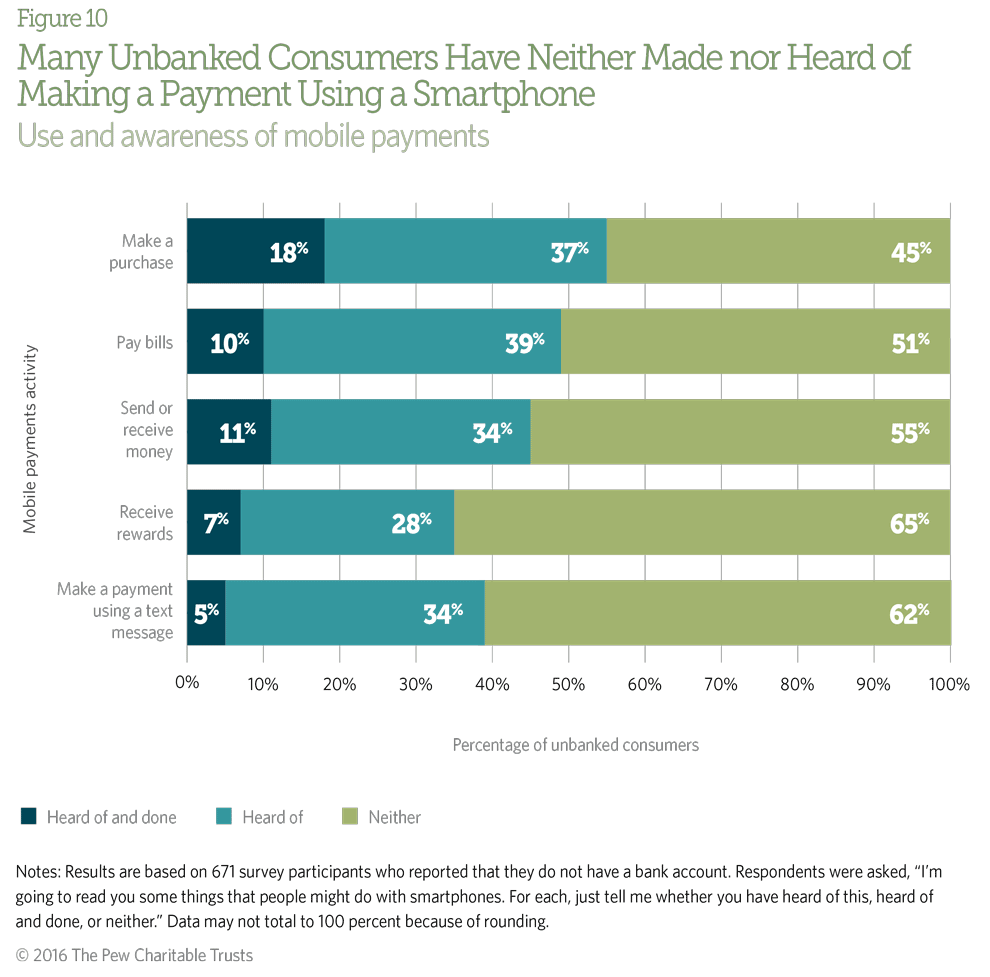

A significant number of unbanked consumers are unaware that it is possible to make payments via smartphone. Usage is also significantly lower among the unbanked: About 39 percent of unbanked smartphone owners have ever made a purchase, paid bills, or sent or received funds using mobile payments technology compared with 64 percent of banked smartphone owners.

Unbanked smartphone owners use mobile payments at significantly lower rates than banked smartphone owners across all types of activity. Across consumers and consistent with prior research, smartphone owners make mobile payments more frequently by accessing a website on their phones or using an app than by sending a text message.16

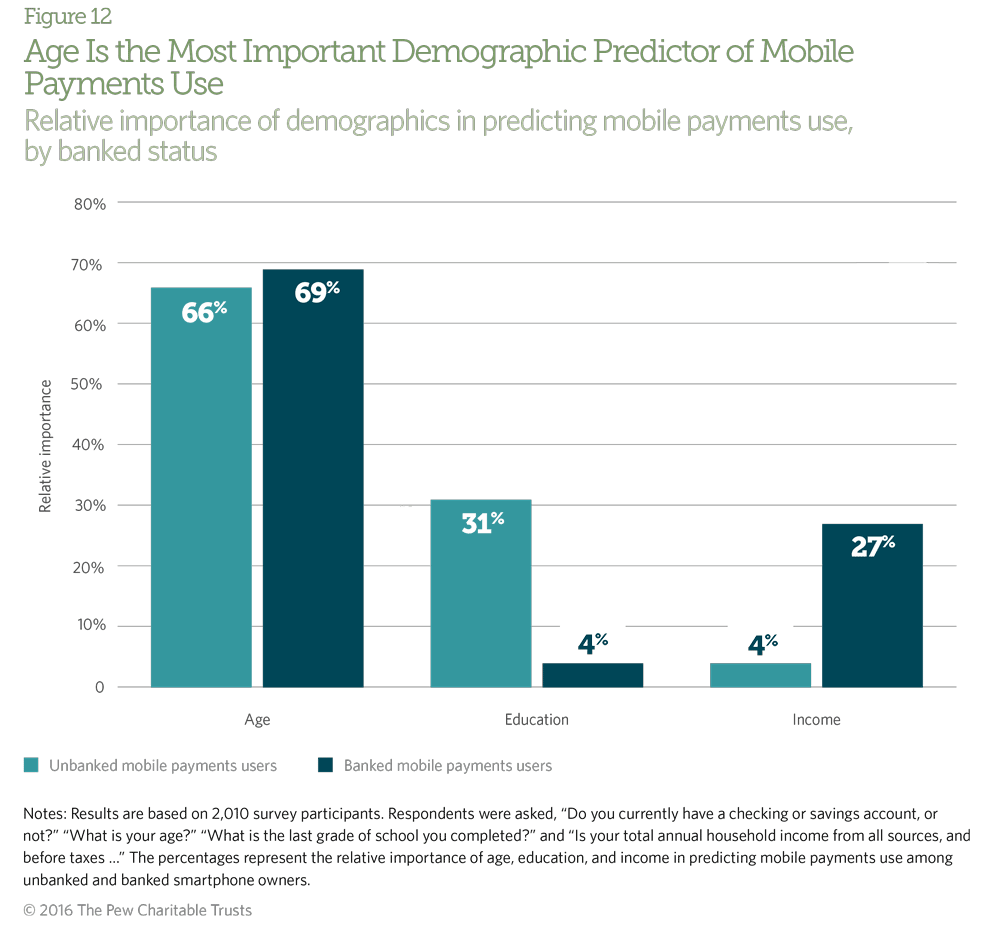

Mobile payments users, whether banked or unbanked, are more likely than nonusers to be millennials or Generation Xers. Among the three demographic factors examined, age is the most important in forecasting mobile payments use among smartphone owners; but the second-most important variable differs by banked status: education among the unbanked and income for those with bank accounts.

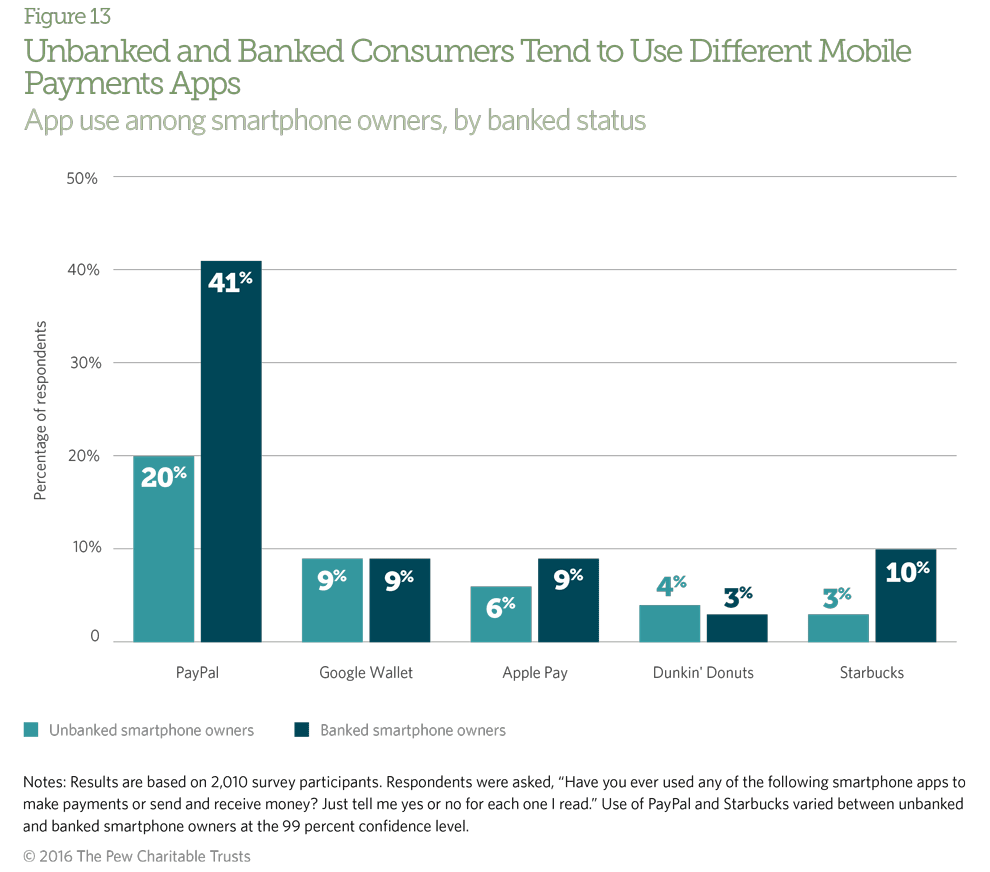

Unbanked smartphone owners are less likely than banked smartphone owners to have used the PayPal and Starbucks apps, but are equally likely to have used the Google Wallet and Dunkin’ Donuts apps. Differences in usage for Apple Pay were not statistically significant.

Compared with banked consumers, those without bank accounts are less likely to make mobile payments and less interested in the potential benefits overall, which may be explained by the barriers to use that many unbanked consumers perceive. For example, in focus groups, when asked whether they were interested in the idea of using their phone to deposit and spend money as they would with a checking account debit card, many unbanked consumers considered the concept convenient because they always carry their phones but also expressed concerns—that banked consumers did not—about the difficulty in loading cash onto an app.17

Unbanked and banked consumers cite a number of the same barriers to mobile payments use, including comparable rates of concern about safety, but unbanked consumers are much more likely to report that, because cash cannot be easily loaded onto a smartphone, frequent use of cash is an obstacle to adoption of mobile payments and somewhat more likely to raise concerns about running out of data and text messages. In addition, both groups reported equal understanding of the benefits of mobile payments.

Conclusion

Mobile payments could offer a more convenient and less expensive way for Americans to manage their money, especially the nearly 37 million U.S. adults who do not have bank accounts. This technology has given these consumers a wider array of options for tracking expenses, depositing funds, making payments, and saving for the future. Yet, this research shows that unbanked smartphone owners are less likely than smartphone owners who have bank accounts to make mobile payments—39 percent and 64 percent, respectively—and are generally less interested in using their smartphones for purchases.

About 60 percent of unbanked consumers have smartphones, but maintaining phone service is often a financial hardship for this population. The unbanked are nearly twice as likely as banked consumers to suspend or cancel their cellphone plans because they were too expensive. For the unbanked, the inability to easily load funds either via check—which is how they most often receive income—or cash onto a smartphone is the most significant barrier to use, even more than concerns about safety, which is the top concern among banked consumers.

Methodology

On behalf of The Pew Charitable Trusts, Social Science Research Solutions (SSRS) conducted a nationally representative random-digit-dialing telephone survey of 1,339 banked and 671 unbanked consumers from Oct. 2 through Nov. 3, 2015. The margin of sampling error, including the design effect, is plus or minus 2.6 percentage points. SSRS conducted 1,029 interviews via cellphone and 132 in Spanish.

Endnotes

- Mobile banking—defined as bill pay, funds transfers, and payments transacted on a smartphone via a bank’s website or app—is a widely used precursor to mobile payments; for more information, see The Pew Charitable Trusts, “Is This the Future of Banking? Focus Group Views on Mobile Payments” (January 2016), http://www.pewtrusts.org/~/media/assets/2016/01/ cb_futurebankingissuebrief.pdf; Susan Burhouse et al., Assessing the Economic Inclusion Potential of Mobile Financial Services, Federal Deposit Insurance Corp. (2014), 1, https://www.fdic.gov/consumers/community/mobile/ Mobile-Financial-Services.pdf.

- The survey found that 14.98 percent of U.S. adults do not have a bank account. The 2014 estimate of the U.S. population age 18 or older is 245,158,000, so approximately 36,724,668.40 (rounded to 37 million) adults are unbanked. Sandra L. Colby and Jennifer M. Ortman, “Projections of the Size and Composition of the U.S. Population: 2014 to 2060: Population Estimates and Projections,” U.S. Census Bureau (March 2015), 6, http://www.census.gov/content/dam/Census/library/publications/2015/demo/ p25-1143.pdf.

- Federal Reserve Board, Consumers and Mobile Financial Services 2015 (March 2015), 2, http://www.federalreserve.gov/econresdata/consumers-and-mobile-financial-services-report-201503.pdf.

- The Pew Charitable Trusts, Checks and Balances: 2015 Update (May 2015), 9, http://www.pewtrusts.org/~/media/Assets/2015/05/ Checks_and_Balances_Report_FINAL.pdf.

- Consumer Financial Protection Bureau, “Data Point: Checking Account Overdraft” (July 2014), 18, http://files.consumerfinance.gov/f/201407_cfpb_report_data-point_overdrafts.pdf.

- The Pew Charitable Trusts, “Overdrawn: Persistent Confusion and Concern About Bank Overdraft Practices” (June 2014), 7, http://www.pewtrusts.org/~/media/assets/2014/06/26/ safe_checking_overdraft_survey_report.pdf.

- Ibid., 14.

- The Pew Charitable Trusts, Slipping Behind: Low-Income Los Angeles Households Drift Further From the Financial Mainstream (October 2011), 15, http://www.pewtrusts.org/~/media/legacy/uploadedfiles/ wwwpewtrustsorg/reports/safe_banking_opportunities_project/ slipping20behindpdf.pdf.

- The Pew Charitable Trusts, Banking on Prepaid: Survey of Motivations and Views of Prepaid Card Users (June 2015), 4, http://www.pewtrusts. org/~/media/assets/2015/06/bankingonprepaidreport.pdf.

- The Pew Charitable Trusts, “Is This the Future of Banking?” 11.

- Pew Research Center, “U.S. Smartphone Use in 2015” (April 2015), 14, http://www.pewinternet.org/2015/04/01/us-smartphone-use-in-2015/.

- Brett Creech, “Expenditures on Cellular Phone Services Have Increased Significantly Since 2007,” Beyond the Numbers: Prices & Spending 5, no. 1, U.S. Bureau of Labor Statistics (February 2016), http://www.bls.gov/opub/btn/volume-5/expenditures-on-celluar-phone-services-have-increased-significantly-since-2007.htm.

- Pew Research Center, “U.S. Smartphone Use in 2015,” 8.

- Fair Isaac Corp., “Millennial Banking Insights and Opportunities” (2014), 8, http://www.fico.com/millennial-quiz/pdf/fico-millennial-insight-report.pdf.

- Pew Research Center, “U.S. Smartphone Use in 2015,” 3.

- Federal Reserve Board, Consumers and Mobile Financial Services 2015, 17.

- The Pew Charitable Trusts, “Is This the Future of Banking?” 11.

America’s Overdose Crisis

Sign up for our five-email course explaining the overdose crisis in America, the state of treatment access, and ways to improve care

Sign up

This video is hosted by YouTube. In order to view it, you must consent to the use of “Marketing Cookies” by updating your preferences in the Cookie Settings link below. View on YouTube

This video is hosted by YouTube. In order to view it, you must consent to the use of “Marketing Cookies” by updating your preferences in the Cookie Settings link below. View on YouTube

Who Uses Mobile Payments?

Mobile payments use has become widespread: Forty-six percent of U.S. consumers report having made a mobile payment, which translates to approximately 114 million adults.

Is This the Future of Banking?

Focus group views on mobile payments

ADDITIONAL RESOURCES

Fact Sheet

Podcast