Checking accounts are the most widely used financial product in the country. Yet poorly regulated bank overdraft practices continue to cause consumers to unknowingly incur multiple costly fees for a single transaction. Pew is promoting new rules to make overdraft programs safer and more transparent.

More than 39 million American adults incurred at least one fee for overdrawing their bank account or having insufficient funds in the past 12 months, according to an analysis of survey data by The Pew Charitable Trusts. Most of these consumers, known as overdrafters, view bank overdraft programs as a way to ensure that payments will go through if checking account balances are low. But almost a third—representing more than 12 million people—said doing so is a way to borrow when short on cash.

Each year banks make billions of dollars in overdraft fees, and more than three-quarters of this revenue is generated from just a small fraction of checking accounts, less than 10 percent. Survey research by The Pew Charitable Trusts shows that overdraft programs are not meeting the needs of most consumers for two key reasons. First, most of those who overdraw their accounts do not know that they can easily avoid these fees, and, second, many of the overdrafters use these programs for credit, even though regulators say they are not supposed to be used in this way.

Overdraft programs are often marketed as a service that banks provide to cover occasional budgeting errors, but in practice they are not well understood by consumers and often fail to meet their needs. The Consumer Financial Protection Bureau requires banks to receive affirmative consent (opt in) from customers before providing overdraft coverage for ATM withdrawals and one-time debit transactions, such as point-of-sale purchases.

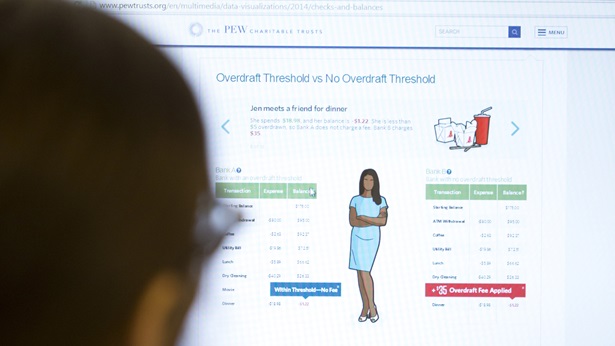

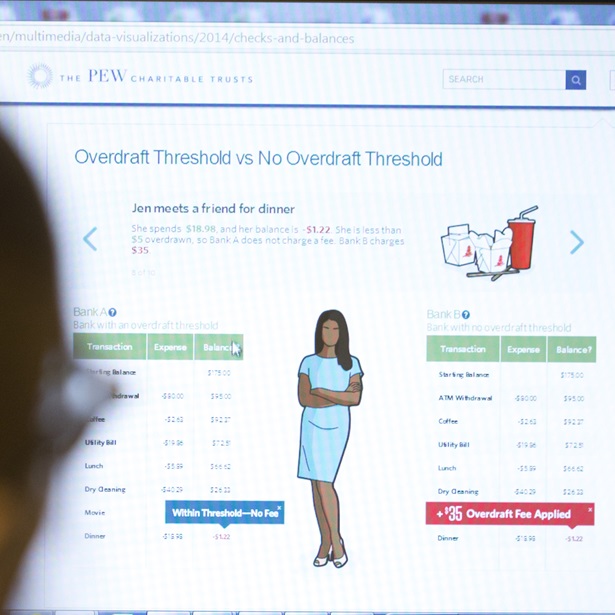

This interactive tool follows three typical people—Mike, Sarah, and Jen—as they go about their day. They are all responsible with money, but their budgets are a little tight. We will explore how, depending on where they bank, their experiences with overdraft fees can differ dramatically, and why it pays to know your institution's policies and practices. Click on a character to start.

Additional Resources

Sign Up

Receive our best conservation research bi-weekly—stunning photos, wins, and action alerts.

Sign Up

Exclusive state-policy research, infographics, and stats every two weeks.

This report finds that many consumers still express confusion and disapproval about bank overdraft practices and the rules surrounding them. Despite federal requirements that consumers must agree to debit card overdraft coverage before any fees are charged or services are provided, Pew’s survey finds that more than half of those who incurred a debit card overdraft penalty fee do not believe they ever opted in to the service. This report includes policy recommendations for the Consumer Financial Protection Bureau to make overdraft programs safer and more transparent.

How does broadband internet reach our homes, phones, and tablets? What kind of infrastructure connects us all together? What are the major barriers to broadband access for American communities?

Antibiotic-resistant bacteria, also known as “superbugs,” are a major threat to modern medicine. But how does resistance work, and what can we do to slow the spread? Read personal stories, expert accounts, and more for the answers to those questions in our four-week email series: Slowing Superbugs.