Pew Unveils Model Disclosure Box for Prepaid Cards

Proposed Feature Highlights Fees, Terms, and Conditions in an Easy-to-Read Format

WASHINGTON—The Pew Charitable Trusts introduced a model disclosure box today for general purpose reloadable prepaid cards that provides information on terms and conditions in a concise and easy-to-read way to make it easier for consumers to compare the cards and avoid unexpected fees.

A general purpose reloadable prepaid card is a relatively new financial product that is growing in popularity: a card that functions like a debit card but is not attached to a traditional, individual checking account. The cards can be used at ATMs, retail cash registers, and online. Americans loaded more than $64 billion onto the cards in 2012, more than double the amount loaded in 2009.

“The disclosures for most prepaid cards are inconsistent and unclear,” said Susan Weinstock, director of Pew's safe checking research. “Terms should be plainly stated so that consumers can choose the product that best meets their needs. This disclosure box should be required by the Consumer Financial Protection Bureau for all general purpose reloadable prepaid cards.”

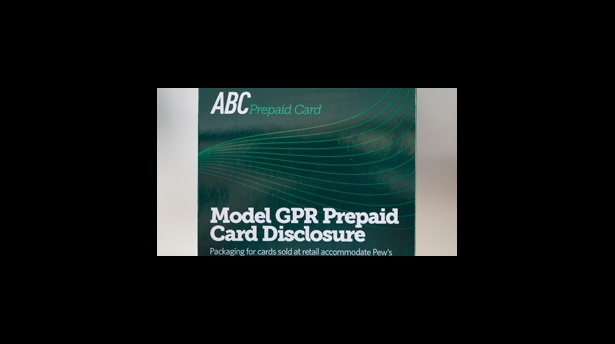

The model disclosure box is presented in a new Pew study, “The Need for Improved Disclosures for General Purpose Reloadable Prepaid Cards,” which details the lack of transparency in current card disclosures. Nearly every one of the 66 cards included in the study failed to disclose at least one type of fee, service, or consumer protection.

The disclosure box fits on existing prepaid card packaging so that it can be available before purchase at retail outlets as well as online. The format is based on Pew's disclosure box for checking accounts, which has been adopted by 26 banks and credit unions covering almost 50 percent of domestic deposit volume. Uniform, concise, and easy-to-read disclosures will help consumers compare the terms and conditions among prepaid products, as well as between those products and checking accounts, so that they can make fully informed decisions.

The rising popularity of prepaid cards has not been matched by increased protections for consumers, however. In its report, released this month, Pew provided the following policy recommendations to the Consumer Financial Protection Bureau to make the cards safer:

- Prepaid cards should not have overdraft or other automated or linked credit features.

- Prepaid cardholders should be protected against liability for unauthorized transactions that occur when a card is lost or stolen or a charge is incorrectly applied.

- Prepaid cardholders should have access to account information and transaction history.

- Prepaid cards should be required to provide information about terms, conditions, and fees in a uniform, concise, and easy-to-read format. This information should be included with the card packaging so that it can be reviewed before the card is purchased at retail outlets as well as online.

- Prepaid card funds should be federally insured against loss caused by the failure of an institution.

- Pre-dispute binding arbitration clauses in cardholder agreements, which prevent customers from challenging unfair and deceptive practices or other legal violations in court, should be prohibited.

The Pew Charitable Trusts is driven by the power of knowledge to solve today's most challenging problems. Pew applies a rigorous, analytical approach to improve public policy, inform the public, and stimulate civic life.

America’s Overdose Crisis

Sign up for our five-email course explaining the overdose crisis in America, the state of treatment access, and ways to improve care

Sign up

This video is hosted by YouTube. In order to view it, you must consent to the use of “Marketing Cookies” by updating your preferences in the Cookie Settings link below. View on YouTube

This video is hosted by YouTube. In order to view it, you must consent to the use of “Marketing Cookies” by updating your preferences in the Cookie Settings link below. View on YouTube

Who Reads 44 Pages of Disclosures?

The Need for a Disclosure Box

ADDITIONAL RESOURCES

Fact Sheet

Podcast